The Finnish Bottleneck Plays

Four overlooked names sitting on the same chokepoints the rest of the market is already paying up for.

The market is going a little insane around any and every name connected to AI, semiconductors, and photonics. Plenty of stocks have risen several hundred percent in a very short window as analysts have mapped the wave of AI spending to specific bottlenecks in the supply chain, and worked out what each one means for the companies sitting in that part of the value chain.

This post is about those companies, and specifically the hidden ones found in Finland.

Unlike their counterparts elsewhere in the world, these names have traded flat for the past few years, some of them down. But they sit on the same bottlenecks. And if the buildout plays out the way the rest of the sector is already pricing in, they have the same potential to see large gains as the spending works its way down the chain.

A note before we start: this is a survey of a cluster I find interesting, not a set of price targets. Some of the international names these get compared to have run well ahead of their fundamentals, and I’ll flag where the Finnish ones have real warts too. The point isn’t that these are guaranteed to follow. It’s that the attention has rotated through the US, Sweden, and Germany and largely skipped Finland, despite the same structural setup.

Canatu: the pick-and-shovel inside the lithography machine

Start with the one I’ve done the most work on. Canatu is a Vantaa-based deep-tech company that’s been quietly building since 2004. That long, boring history is the whole reason nobody owns it: it spent most of its life in the lab, and it’s only now hitting the point where the science turns into revenue. The market hasn’t repriced it because, until recently, there was nothing to reprice.

The first-principles case is simple. Making advanced chips runs through one chokepoint: EUV lithography machines, built only by ASML. Inside each machine sits a consumable part that protects the most expensive component, and as the machines get more powerful, the old version of that part stops working. Canatu makes the technology for the new version. So without getting into the chemistry, the position is this: the AI buildout needs chips, the chips need these machines, the machines need this part, and the current materials are hitting a wall. Canatu sits exactly on that wall.

What makes it a business rather than just a clever product is the model. Canatu doesn’t manufacture and ship the part itself. It sells a reactor to a partner, sells the proprietary inputs that only it can supply, and then collects a royalty on every single unit the partner produces. One sale turns into three revenue streams, and the best one, the royalty, recurs forever with almost no cost or manufacturing risk attached. They carry none of the capital burden of building factories around the world; the partner does. Canatu just owns the IP and clips a fee off everything that comes out. That’s the kind of capital-light, high-margin, recurring structure that, if volumes scale, becomes very valuable very fast.

It’s not theoretical anymore. The model went live in October 2025 when a Korean partner, FST, took a commercial license. The interesting wrinkle: Samsung owns a stake in FST. So Canatu is effectively plugged into Samsung’s supply chain without ever appearing as a direct supplier, which is about as good as it gets for a company this size.

Now the honest part, because the bull case usually overstates it. Canatu is not the only player here. Mitsui, the established incumbent, is developing a competing version of the same part with its own backing. So the right way to think about Canatu is not “irreplaceable monopoly.” It’s the other door. The entire chip supply chain relying on one supplier for a critical consumable is exactly what makes the big fabs nervous, nobody wants a single point of failure on something that gates their most expensive equipment. Canatu is the credible independent alternative, and the only one offering partners a way to make this in-house under license rather than buying from a competitor. In a market this strategic, being the trusted second source isn’t a consolation prize. It’s a structurally excellent place to sit, and the licensing model means even winning a modest share compounds into real money over time.

A few things to keep honest. The payoff got pushed from 2027 to 2030, so this is a multi-year hold, not a quick flip. The company still loses money (2024 revenue was €22M, up 62%, but it ran a €5M net loss) because it’s spending to build capacity, which is normal at this stage but demands patience. And the share count is the detail most holders miss: thanks to how the company came public, more shares get issued as the price rises, so the realistic fully-diluted figure is closer to 44-46 million than the ~34 million your broker shows. If you’re doing the math, use the bigger number.

The most recent signal is the one I’d weight most. In May, Dr. Maximilian Slawinski took over as CEO, coming from Soitec, a company whose entire competence is taking advanced semiconductor materials from “we can make a little” to “we can make a lot.” That is exactly the problem Canatu has to solve next. Moving from one-off deliveries into real commercial volume is a different skill than inventing the technology, and they just hired someone who has done precisely that. For a company at this specific inflection, it’s the right hire at the right time.

Aspocomp: the tiny re-shoring bet

Aspocomp is a different kind of idea, smaller, scrappier, and riskier, but it sits in front of a real tailwind that the big banks have started naming out loud.

The first-principles case starts one layer away from the chips themselves. Everything in an AI server has to sit on something, and that something is a printed circuit board. As the boards get denser and more complex to handle AI workloads, they’ve quietly become a constraint of their own. Goldman’s spring 2026 supply-chain work flagged PCBs and the laminates underneath them as one of the genuine bottlenecks in the buildout, with prices climbing 30%-plus a year and shortages they don’t expect to clear before 2027. So this isn’t a Finnish curiosity. It’s a global chokepoint that a major bank has put in writing, and Aspocomp is one of the few European names that plays in it.

Here the interesting part isn’t really the company, it’s the geography. Almost all of this production sits in Asia. Europe has been trying, through the Chips Act and now its successor, to drag critical supply chains back onshore so the continent isn’t fully dependent on imports for the things that matter most, defense electronics, semiconductors, aerospace. A PCB maker with an actual European plant and defense and semiconductor qualifications is exactly the kind of supplier that policy is designed to favor. That’s the core of the bet: not that Aspocomp out-competes the Asian giants on cost, but that Europe increasingly needs a domestic option and is willing to support one.

And there’s early evidence the demand is real. In its most recent quarter the company posted a record order book, with the bulk of new orders coming from the semiconductor and defense segments and part of the backlog stretching into late 2027, unusually long visibility for a company this size.

Now the warts, and they’re real. This is a genuinely tiny company, a market cap around €30 million, with a single plant. Recent results have been bumpy: even as orders hit records, sales actually dipped and margins compressed hard, dragged down by low-margin contracts signed earlier and a literal equipment breakdown that hurt output. That’s the risk in one picture, the order book says one thing, the income statement says another, and the gap between them is execution. Scaling a small single-site manufacturer into a hundred-million-euro revenue company, which is their stated long-term ambition, is hard, capital-hungry, and exactly the kind of thing small caps stumble on. None of that is hidden; it’s why the stock is where it is.

So I’d frame Aspocomp honestly: not a chokehold story like Canatu, and not a clean compounder. It’s a “right place as Europe re-shores, in a category the banks are now flagging” bet, in a name small enough that almost nobody is looking. Worth watching, not pounding the table.

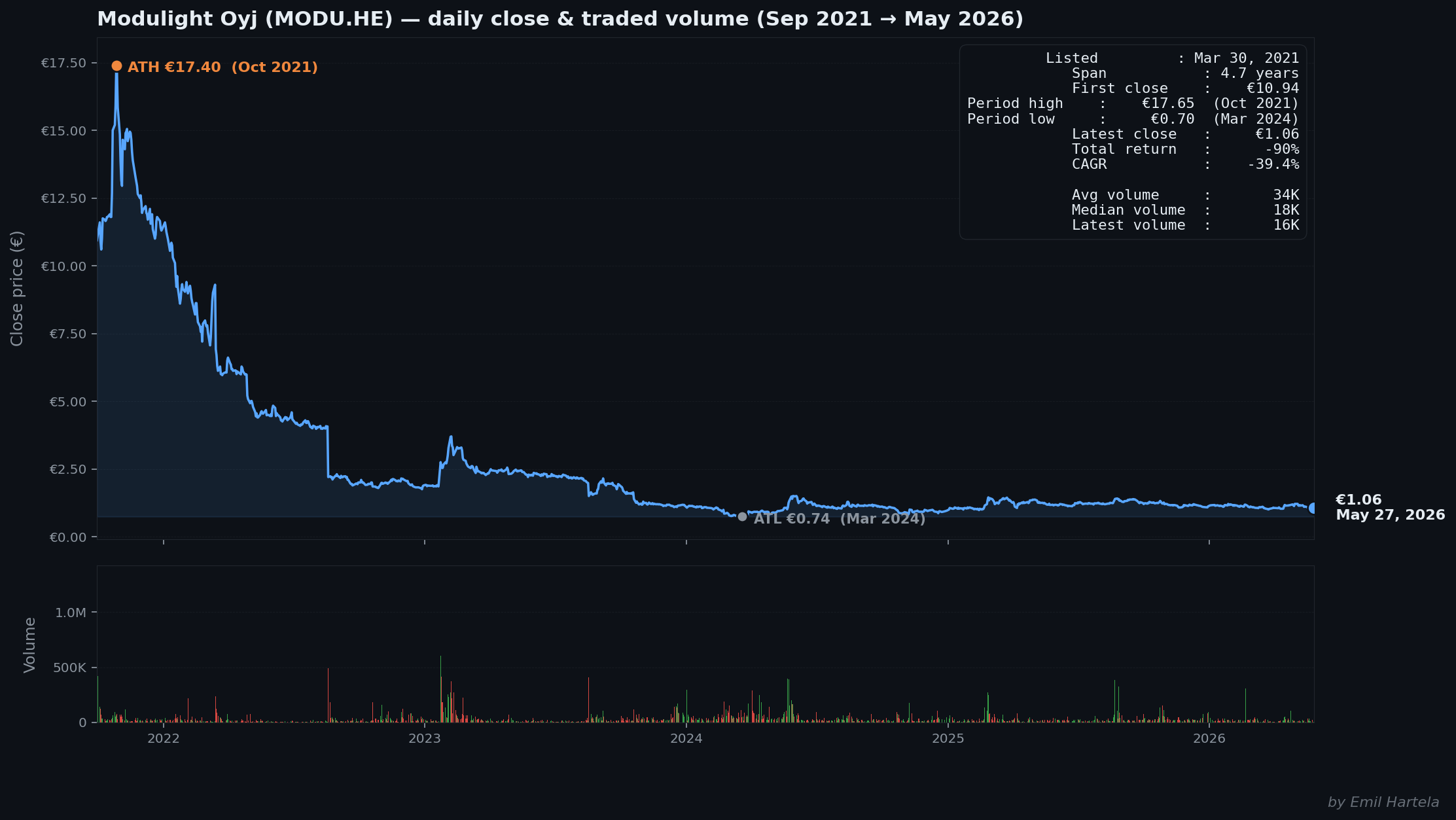

Modulight: the photonics wildcard

The third name is more of a wildcard, and I’ll keep it shorter because I’m earlier in my own work here. Modulight is a Tampere laser company that’s been around since 2000. The core business today is medical lasers, mostly for cancer treatment and eye conditions, a real, revenue-generating business, not a story stock. But the part that’s interesting in this context is that it runs its own vertically integrated facility in Finland, doing semiconductor fabrication, laser assembly, and optical calibration all under one roof. That’s an unusual amount of capability for a company this small, and it gives it a genuine foothold in photonics, with early exposure to defense optics, quantum, and semiconductor applications.

The first-principles appeal is the same shape as the others: a small European company with real manufacturing capability in an area where the world is increasingly worried about depending on Asia. And there are two things I like about how it’s built. First, the balance sheet is genuinely strong, mostly equity, a net cash position, and enough runway to fund itself toward profitability without being forced to raise money and dilute holders, which is rare for a company at this stage. Second, it’s quietly shifting toward a recurring “pay-per-treatment” model, where it earns a fee every time one of its hospital systems runs a procedure, rather than just selling a machine once. That’s the kind of model that compounds if it scales.

Here’s the honest framing, though, and it’s why I’d hold this one at arm’s length for now. Modulight sits a step further from the current AI and semiconductor boom than Canatu or Aspocomp. Its revenue today is medical. The photonics, defense, quantum, and semiconductor angles, the parts that would tie it directly into the trade everyone’s chasing, are early-stage optionality, not the core of the business yet. So the bull case is more diffuse: you’re backing a well-run, profitable niche company that happens to hold several call options on hot themes, rather than a pure-play sitting squarely on a named bottleneck.

That cuts both ways. It makes Modulight less obviously a rotation beneficiary than the other two. But it also means that if attention swings toward European photonics and defense optics under the same re-shoring logic, a small, profitable, vertically integrated laser maker in a NATO country is exactly the kind of name that could catch outsized interest in a hurry. Worth watching, and worth a proper deep dive, which I’ll do before I say anything stronger.

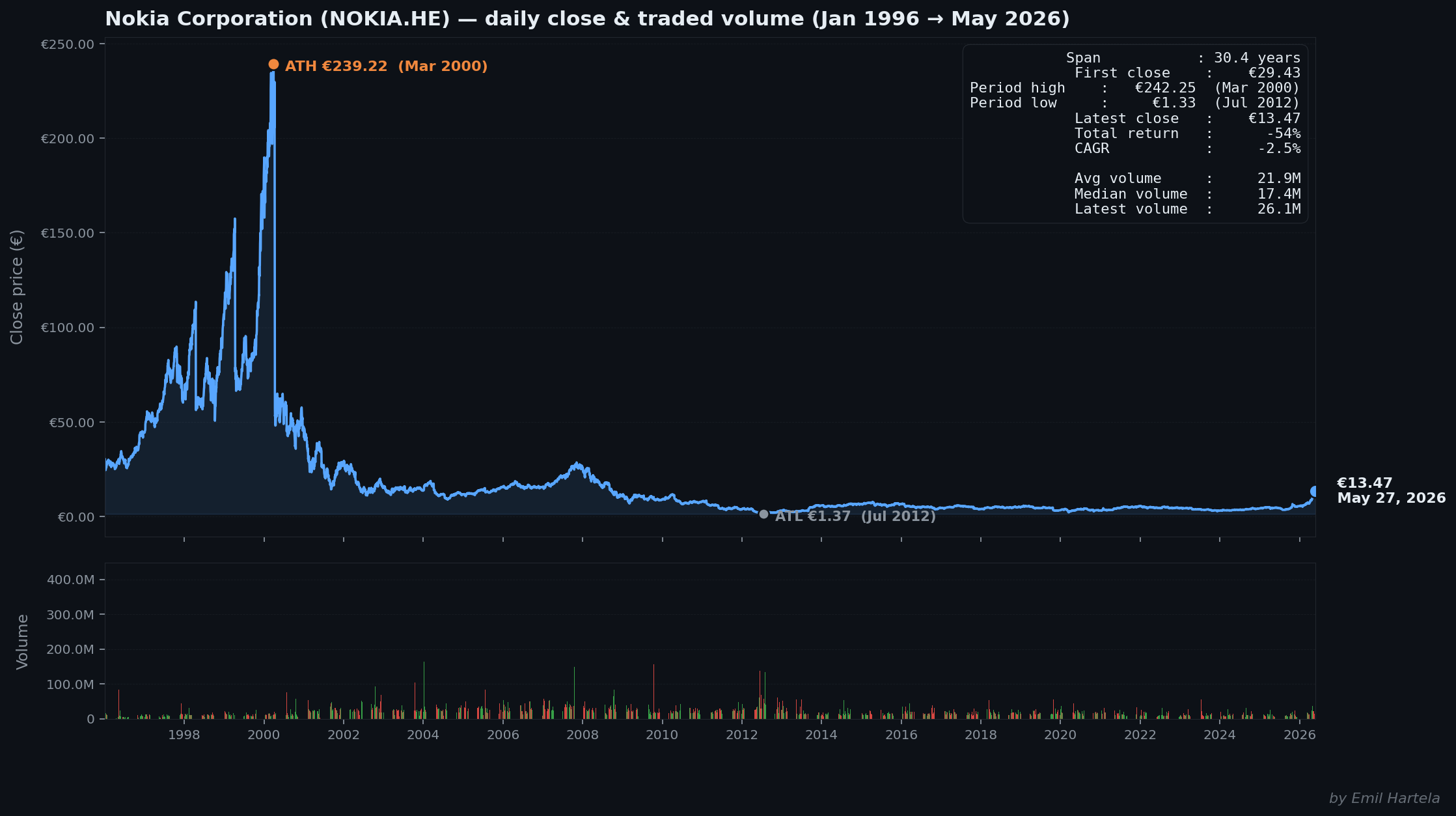

Nokia: proof the rotation is real

I’ll end with the one everybody already knows, because it’s the proof of concept for everything above. Nokia spent a decade as a byword for a Finnish tech champion that lost its way, the phone company that missed the smartphone, then a telecom-equipment also-ran trading sideways for years. The kind of name nobody on FinTwit wanted to touch.

And then it re-rated, hard. Not on the old telecom story, but because the market reframed it as an AI-infrastructure play. The acquisition of Infinera plugged Nokia directly into optical networking, the systems that move data between and inside the data centers AI runs on, and suddenly its order book and guidance started reading like a different company. The stock has roughly doubled off its lows as investors repriced it from a legacy equipment vendor into something exposed to the same buildout that’s lifting everything else in the supply chain.

The point isn’t to pitch Nokia here, it’s already been found, and a doubled stock is a different risk-reward than an undiscovered one. The point is what it demonstrates. A large, sleepy, unloved Finnish tech name sat flat for years while the AI trade raged everywhere else, until the market finally connected it to a bottleneck it was actually exposed to. Then it moved fast.

That’s the whole thesis of this post in one example. The attention rotates. It went through the US hyperscalers, then the picks-and-shovels names, then Sweden and Germany, and at each step it eventually reached the companies sitting on a real bottleneck, regardless of how boring or overlooked they’d been. Nokia is the Finnish name where that has already happened. Canatu, Aspocomp, and Modulight are names where, on the same logic, it largely hasn’t yet.

I’m not promising it will. Plenty of these setups never get their moment, and I’ve tried to be honest above about where each of these has real warts, execution, dilution, timing, size. But the structural pattern is hard to ignore: the same bottleneck themes that have repriced names across the US, Sweden, and Germany are sitting, mostly undiscussed, on a handful of Finnish balance sheets. Nokia shows what it looks like when the market finally notices. The rest of the cluster is still waiting.

That’s the bet. Not that any single one of these is a sure thing, but that the gap between “same bottleneck, same tailwind” and “a fraction of the attention” is exactly the kind of inefficiency worth being early to.

Disclaimer

This post is for informational and educational purposes only. It is not financial advice, an investment recommendation, or an offer or solicitation to buy or sell any security. I am not a licensed financial advisor, and nothing here is tailored to your individual circumstances, risk tolerance, or objectives.

I hold positions in some of the companies discussed, so I am not impartial. The names covered here are small-cap and micro-cap stocks listed on Nordic exchanges, which carry elevated risk: low liquidity, high volatility, wide spreads, limited analyst coverage, and real potential for permanent loss of capital. Several are not yet profitable and may need to raise capital, diluting existing shareholders.

Some figures and claims in this post draw on company filings, third-party analyses, and external market data that I have not independently verified in every case, and which may contain errors or become outdated. Forward-looking statements and any scenario or valuation figures are inherently uncertain and should not be relied upon as predictions.

Do your own research. Verify everything independently, and consider consulting a qualified financial professional before making any investment decision. You alone are responsible for your investment choices.

DYOR. NFA.