Superyachts for the Rest of Us

How to own a slice of the world's most exclusive industry without owning the boat

I have spent pretty much every single summer of my life in the Mediterranean, boating somewhere between Mallorca and Venice. That has given me constant exposure to mega yachts and the entire ecosystem that surrounds these boats.

To understand the significance of what I have been seeing in the post pandemic years, I will start by taking you back to how things looked roughly ten years ago in places like Capri and Porto Cervo.

Back then, the yachts you saw sat in the 30 to 40 meter range, and very rarely more than that. Spotting something larger happened maybe once a week. I still remember seeing Paul Allen’s Octopus at roughly 126 meters somewhere near Capri. At the time, that boat ranked among the ten largest yachts in the world.

When you hopped off your boat and took a stroll into one of the luxury marinas, things were also very different. There was clearly more moderation. Stuff did not have to sport a strong brand or be well known. Social media was still in its infancy, so the shape of luxury in many of these places was completely different. I will return to social media soon, because it plays a bigger role in this story than one might think.

Now to the present. I just returned from the Mediterranean once again, and it suddenly hit me that the change between now and ten years ago is massive. The first thing you notice is that those 30 to 40 meter yachts, which represented a sort of ceiling back in the day, are now closer to 100 meters. Instead of seeing one very long yacht like Octopus once a week, you now see several 100 meter boats daily. The 100 meter boat is essentially the new 40 meter boat. At first this might sound insane, but I will do my best to explain what is going on.

The same shift shows up across the marinas and the wider luxury ecosystem. Where you previously had a marina filled with nice but unknown restaurants and brands, you now have pretty much the opposite. The towns are filled with all the usual suspects like Stefano Ricci, Kiton, Brunello and Loro Piana. There are very few unknown names left. By unknown, I mean brands that do not already have a store in every major city around the world. Restaurants follow the same pattern. Many are now well known luxury chains. It feels like there is a Zuma or a Cipriani in pretty much every place now.

The thing I want you to keep in mind from this intro is that there has been a massive change over the last ten years, and few have had time to register its magnitude. Many simply hold the wrong perception of reality when it comes to the post pandemic world. This new reality is stark enough to raise an obvious question. What kind of investments will benefit from it? So I decided to map several winners in the field that I believe have the potential to do well. But before that, I will explain the underlying trends driving the stark difference we can now see.

Why the Boats Got Bigger

As I mentioned earlier, the last ten years have brought a massive change in the luxury yachting scene. I will now explain my take on why the difference is so stark.

The first culprit is social media, and especially Instagram. It was not long ago that Instagram did not exist, let alone the subcultures that I believe are driving a lot of the change we are seeing. Both old money and the wealth and hustle crowd are thriving on Instagram, and this magnifies the whole yachting sector. It is now far easier to see that your boat is not as big as someone else’s. Your wife and children would rather go to Zuma for the pictures. Yachting already represents the top of luxury, and when you couple it with social media, the result is exactly what we see today. Bigger yachts, more exuberance, and importantly, less durable spending. I believe social media is a large part of the puzzle, but not all of it. There are two other factors that are equally important.

The second tailwind is tech, the wealth created from tech, and what it does to the buyer demographic. In the past, yachts could really only be afforded by 70 year olds. Now you have tech billionaires and millionaires who are under 40. The effect is fairly self explanatory. These younger people have more of a need to show off, since they grew up with social media. Many of them sit on more wealth than they know what to do with, and most importantly, they are young. Yachting is not always the most comfortable form of luxury for an older person, but for a 40 year old there is nothing better. On top of that, the fact that under 40 tech billionaires now own yachts and post about them online adds even more pressure on everyone else to get a taste of the lifestyle. That brings us to the third reason yachts are booming like never before.

The third reason ties back to the picture social media paints. If yachting looks common, and not partaking makes you an outsider, then the only solution for someone with less money is to charter. And charter they have. Chartering has grown explosively over the past ten years. A person earning 500k a year obviously cannot afford to buy a 50 meter yacht, but what they can do is gather ten friends, put in 30k each, and split a week on the water. Sustainable or not, it is happening. More and more people are willing to spend an outsized portion of their income and wealth on chartering bigger and bigger boats.

These three forces combined are what, in my opinion, has created this massive influx of money chasing a sector that ten years ago was far smaller. Now let us jump into some of the stocks that enable and profit from this changed reality.

Sanlorenzo S.p.A. (SL.MI, Euronext Milan)

Of all the stocks I have looked at so far, Sanlorenzo is the one that strikes me as the safest and most reasonable bet. It trades at roughly 11 times earnings, which sits well below its own ten year average, and the business underneath that multiple looks genuinely healthy rather than cheap for a reason.

The story starts in 1958 in Ameglia, on the Ligurian coast. For most of its life Sanlorenzo was a small, almost artisanal builder. The modern chapter began when Massimo Perotti, still chairman and CEO today, took control in 2005 and slowly turned it into the reference name at the top of the market. It listed in Milan in 2019, and since the IPO it has hit every financial target it set, growing revenue, margins and order intake across very different market conditions.

What makes Sanlorenzo interesting for this thesis is how pure the bet is. The company holds its leadership in the 30 to 40 meter segment, which is exactly the part of the market that has migrated upward over the last decade, and through its Superyacht division it builds well beyond that. There is no mass-market boat dragging down the brand. The structure is clean: Bluegame for smaller utility yachts, the core Yacht division, and the Superyacht division at the top. Compare this to many peers who either stretch their range down into far smaller boats to chase volume, or sit buried inside a wider industrial group, or remain private and uninvestable. Sanlorenzo gives you close to a pure play on exactly the kind of large, expensive yacht that now fills Porto Cervo.

The thing they are genuinely good at is scarcity. Management talks openly about choosing value over volume and elegance over extravagance, and they mean it as a financial strategy, not just marketing. They deliberately keep waiting lists long rather than flooding the market, which protects pricing and resale value. Waiting lists currently extend as far out as 2029. That discipline shows up in the margins. EBITDA margin has climbed from 14.5% in 2019 to 18.8% in 2025, and net profit went from about 27 million euros in 2019 to 107 million in 2025.

The buyer base is worth dwelling on, because it ties directly into the trends I laid out earlier. Sanlorenzo sells to a sophisticated, repeat ultra high net worth clientele, and a meaningful share of growth is coming from exactly where you would expect given the demographic shift: the Americas and the Middle East. In Q1 2026, revenue from the Americas rose almost 19% and the Middle East and Africa rose 24%. These are younger, newer money buyers entering a market that used to belong to an older European crowd.

The backlog is the part that makes the whole thing feel solid rather than speculative. As of the end of March 2026 the order backlog stood at roughly 1.23 billion euros, with 90% already sold to final clients rather than to dealers. That backlog covers around 72% of 2026 revenue guidance, and order intake has now grown for seven consecutive quarters, with Q1 2026 up over 25% year on year. In a cyclical industry, that kind of forward visibility is rare and it is what lets you underwrite the earnings with some confidence.

None of this means it is risk free. The broader superyacht market actually normalized in 2025, with total sales down around 8% versus 2024, and Sanlorenzo outperformed rather than escaped that. The business is still cyclical, and a prolonged downturn in new builds would eventually pressure intake. But the combination of a clean balance sheet sitting in net cash, a long backlog, a disciplined scarcity model and a low double digit multiple is exactly why I see this as the anchor position of the basket rather than the lottery ticket.

Ferretti S.p.A. (YACHT.MI, Euronext Milan)

If Sanlorenzo is the anchor, Ferretti is the close second, and arguably even slightly cheaper. It trades at a similar low double digit multiple while carrying something Sanlorenzo does not have: a stable of the most recognizable names in the entire industry.

That portfolio is the whole reason to own it. Ferretti owns and markets seven brands, including Ferretti Yachts, Riva, Pershing, Itama, CRN, Custom Line and Wally, distributed through roughly 60 dealers across more than 70 countries. Riva alone is arguably the most iconic name in yachting, the brand of the classic wooden runabout that has meant glamour on the water since the 1950s. And for me personally the jewel is Wally, my favorite brand of the lot, the maker of those radical, almost spaceship-like sailing and motor yachts that look like nothing else on the water. Owning Ferretti means owning the heritage and the design language that a large part of the buyer base is actually chasing.

Strategically Ferretti is broader than Sanlorenzo. Where Sanlorenzo deliberately stays narrow and scarce, Ferretti spans everything from serial production boats up through full custom superyachts built at CRN, covering far more of the market. The group runs both a serial market and a superyacht segment, giving it a transversal presence across most segments of yachting. That breadth is a double edged sword. It gives diversification and scale, but it also means the brand isn’t quite the pure top-end play that Sanlorenzo is. You are buying a portfolio rather than a single rifle shot at the largest boats.

The superyacht end, which is the part this thesis cares about most, is in good shape. Production capacity in the superyacht segment is virtually fully utilised out to 2029, which tells you the demand for the genuinely large, expensive boats is still there even as the cheaper end wobbles.

Now the honesty section, because Ferretti has more hair on it than Sanlorenzo. The first quarter of 2026 was clearly softer. New yacht turnover fell about 8% year on year, but the bigger worry was order intake, which dropped almost 34% to roughly 180 million euros, driven largely by geopolitical tension in the Middle East delaying orders and deliveries. The net order backlog slipped to 722 million euros from 829 million at the end of 2025. Margins held up, which is the saving grace. Adjusted EBITDA came in at 48.7 million euros versus 52.5 million a year earlier, so profitability proved resilient even as the top line softened.

The second issue is governance, and it is messier. China’s Weichai Group won a shareholder vote that ended the twelve year tenure of long-time CEO Alberto Galassi, while Czech investor KKCG appealed the validity of that decision, leaving the governance situation unresolved. Italy has also been weighing KKCG’s request for golden power scrutiny, partly because Ferretti owns a small non-core patrol boat division. A new global CEO, Stassi Anastassov, is now in place, but the ownership picture is genuinely in flux, and that is the single biggest reason this sits a notch below Sanlorenzo on the risk scale rather than at the same level.

So the trade-off is clean. Ferretti gives you the better brands, a broader footprint, and a slightly cheaper entry, in exchange for a softer recent quarter and real governance uncertainty. For a basket built around this theme, it earns its place precisely because of Riva, Wally and CRN, names that the post pandemic buyer actually wants, even if you size it a little smaller than the anchor to account for the noise.

MarineMax, Inc. (HZO, NYSE)

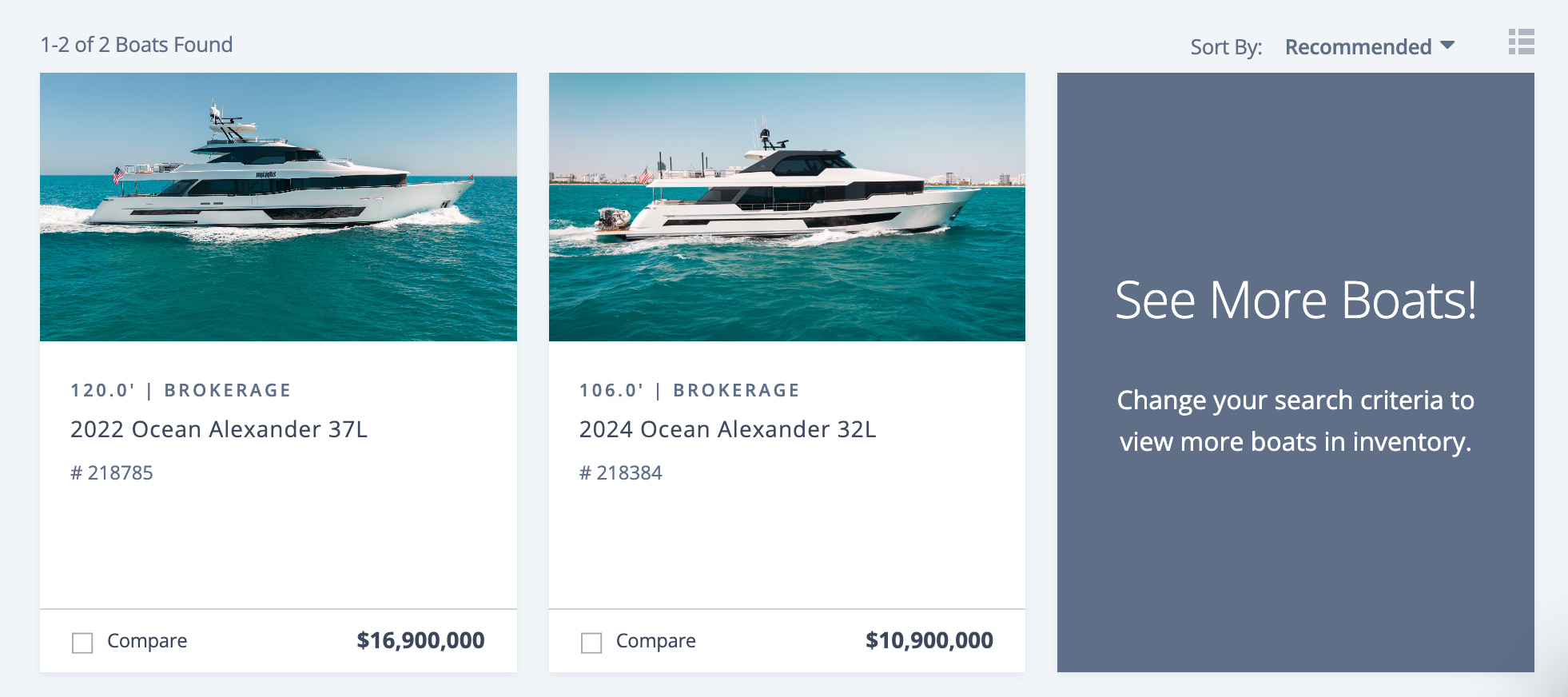

MarineMax is the stock that gives you a completely different way to play this theme, and that is exactly what makes it interesting. The two Italian names are builders. MarineMax is everything around the boat. It bills itself as the world’s largest recreational boat and yacht retailer, marina operator and superyacht services company, with over 120 locations worldwide, including more than 70 dealerships and over 65 marina and storage facilities. If the Italians sell you the boat, MarineMax wants to dock it, broker it, finance it, insure it and service it.

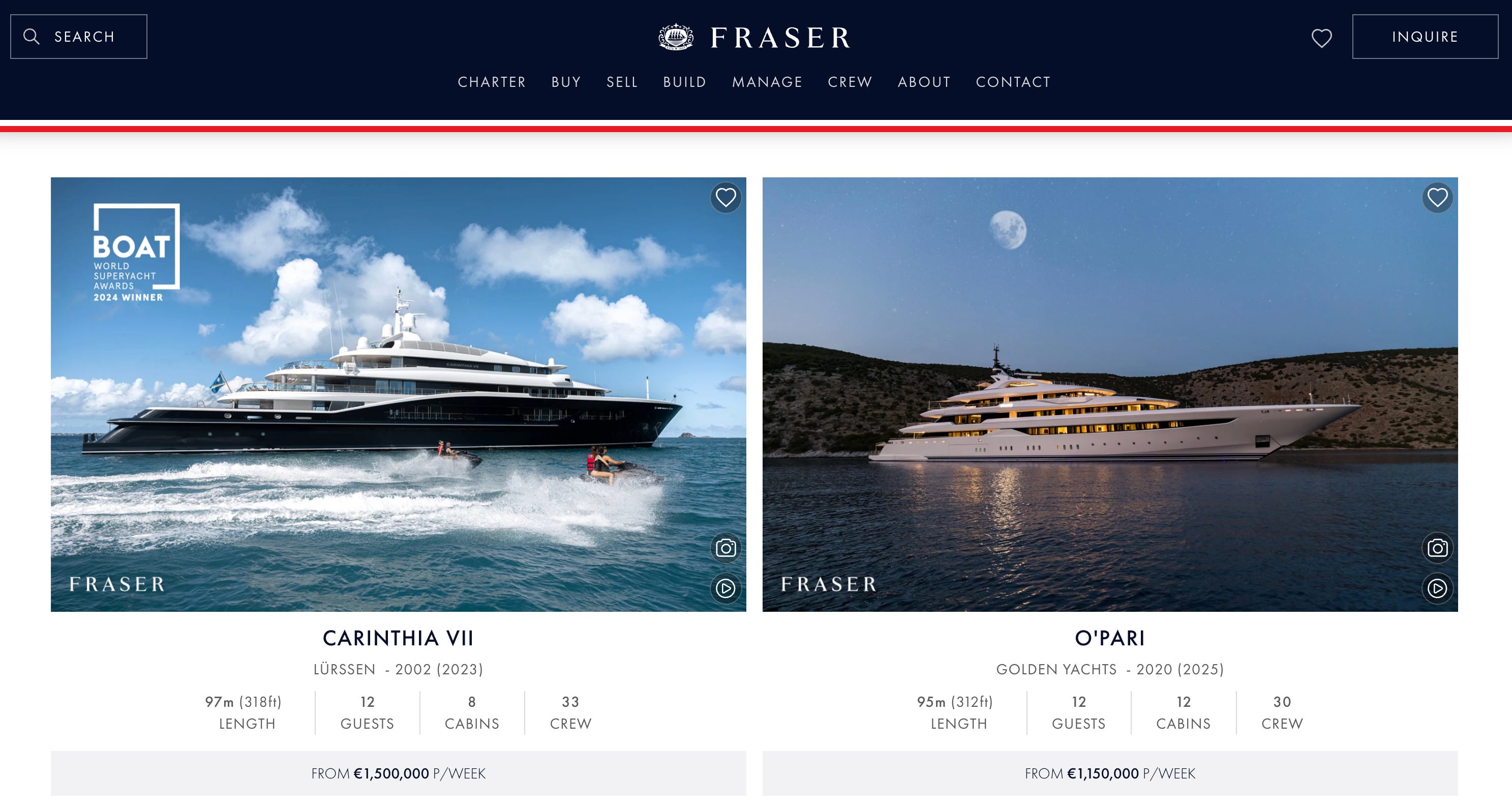

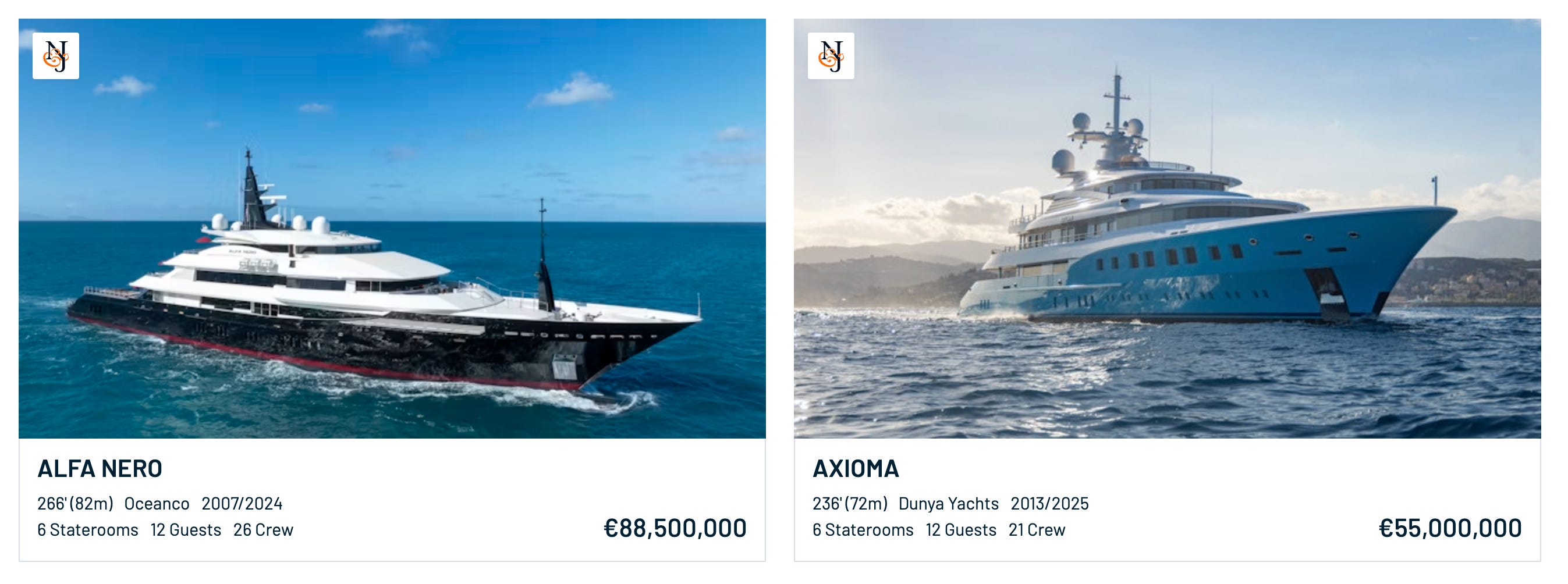

The pieces that matter for this thesis are the ones at the top of the chain. Its superyacht services run through Fraser Yachts Group and Northrop & Johnson, two of the best known names in superyacht brokerage, both acquired over the past decade as part of a deliberate move upmarket. On the infrastructure side, its IGY Marinas operate luxury facilities across the Caribbean, the Mediterranean and major US yachting destinations. This is the part I find most attractive. Marinas and brokerage are the toll booths of the yachting world. As boats get bigger and more numerous, somebody has to berth them and somebody has to handle the sale, and MarineMax owns both functions. It is a way to bet on the activity around the boom rather than on any single hull selling.

Here is where my reservation comes in, and it is a real one. The financials are messy and the headline numbers are going the wrong way. Second quarter fiscal 2026 revenue came in at 527 million dollars, down more than 15% from a record 631 million a year earlier, with same-store sales down 15% against an 11% increase in the prior-year period. The company swung to a net loss of 2.6 million dollars, versus net income of 3.3 million the year before. Used boat sales were the weakest line, falling 44% year over year. This is not a clean compounder. It is a cyclical retailer having a tough stretch as the broader boat market normalizes.

The counterargument, and the reason it still earns a place, is the mix shift underneath the decline. The higher-margin businesses are exactly the ones tied to this thesis, and they are growing while retail shrinks. The superyacht services, marina, finance, insurance and parts operations grew both as a share of revenue and in absolute dollars year over year, even as boat revenue fell around them. That shift shows up in profitability. Gross margin actually expanded to 34.4% from 30% a year earlier, driven by the increasing contribution from those higher-margin businesses. In other words, the part of MarineMax that this whole article is about is the part that is working. The drag is the commodity retail boat business, which is the part you care about least.

There is also an outside chance of a corporate catalyst. The company received an unsolicited, non-binding indication of interest from The Donerail Group to acquire all outstanding shares for 35 dollars per share in cash, and that approach drew further reported interest from large private equity names. Whether anything comes of it is unknowable, but it puts a degree of attention on the valuation that a sleepier name would not have.

So my honest framing is this. MarineMax is not the pure play, and the income statement makes that obvious. You are buying a diversified marine conglomerate with a cyclical retail anchor dragging on a genuinely attractive luxury services and marina core. But it is one of the only listed ways to own the toll booths rather than the hulls, and in a field this thin on options, that uniqueness is worth something. I would treat it as the more speculative, mix-shift bet of the basket rather than a name you underwrite on current earnings.

The Italian Sea Group S.p.A. (TISG.MI, Euronext Milan)

I want to be completely upfront here. The Italian Sea Group belongs in this article on paper, because it owns some of the most storied names in the business, but the company is currently in the middle of a serious crisis that I do not yet understand well enough to underwrite. I am including it for completeness and transparency, not as a recommendation, and I would rather tell you plainly what I do and do not know than pretend I have it figured out.

The brand portfolio is the reason anyone looks at it in the first place. TISG’s brands include Admiral, Tecnomar, Perini Navi, Picchiotti, NCA Refit and Celi 1920. Perini Navi in particular is a legendary name in large sailing yachts, which ties directly into that trend I mentioned earlier about big sailing yachts being the ultimate flex. In a normal world, this would be a pure-play builder at the very top of the market.

But this is not a normal situation, and the timeline of the last few months is alarming. In early 2026 the company launched an independent forensic investigation into unauthorised overspending, two weeks after taking a 25 million euro shareholder loan to shore up its cash position. Workers staged a two-hour strike in February after wages were delayed by eight days due to liquidity problems, and the board acknowledged the company had incurred significant extra-budget costs in executing orders. The chair and vice chair resigned, with founder and CEO Giovanni Costantino taking over as chair.

It got worse from there. The Italian Stock Exchange ordered the company’s exclusion from STAR status, a complaint was filed against former executives, and the company initiated a negotiated settlement procedure under Italian insolvency law. Then the real shock. In May 2026 the company announced that losses had reduced its share capital below the legal minimum, a material event under Article 2447 of the Italian Civil Code, and the shares fell more than 37% in a single day. The exact amount of the losses is still being determined, pending ongoing accounting reviews, and the forensic due diligence by KPMG has experienced delays. The stock, which traded above 8 euros at its 52-week high, has collapsed to roughly 1.2 euros.

There is also a darker backdrop that I am still trying to make sense of. TISG was the builder of the superyacht Bayesian, which sank off Italy in August 2024. There is now litigation swirling around that event, with the company reportedly pursuing legal action while a UK investigation raises unresolved questions about the yacht’s design and stability. How much of the financial crisis is connected to that, versus separate accounting and order-management problems, is exactly the kind of dynamic I have not yet untangled.

So my honest position is this. I do not currently hold it and I am not telling you to. The brands are real and the underlying market is the same booming market the rest of this article describes, which is precisely why a distressed, restructuring situation like this can become interesting to a certain kind of investor once the facts are clearer. But right now it is a forensic-investigation, capital-below-minimum, court-supervised-restructuring story, and anyone who tells you they know how it resolves is guessing. I am flagging it so you have it on your radar, and I will only form a real view once KPMG’s review is complete and the true scale of the losses is known. Treat this section as a transparent placeholder rather than a thesis.

Grand Harbour Marina p.l.c. (GHM, Malta Stock Exchange)

The last name on the list is more of an honorable mention than a core idea, but it is worth including because it is about as pure a play as you can find anywhere in this space. Where MarineMax bundles marinas inside a sprawling retail conglomerate, Grand Harbour Marina is essentially just the marina, full stop.

The business is simple to understand, which is part of the appeal. The company owns and operates marina facilities providing berthing and ancillary services for yachts and superyachts, running through two segments: the Grand Harbour Marina in Malta and a stake in the IC Cesme Marina in Turkey. The Malta asset sits in the historic Grand Harbour next to Valletta, and it is built for exactly the kind of boat this whole article is about. The marina offers over 250 berths and 26 superyacht berths able to take vessels up to 135 metres. It is owned and managed in association with Camper & Nicholsons Marinas, a recognized name in the luxury berthing world.

This is the toll-booth idea in its purest form. As the trend pushes the Mediterranean toward more and bigger boats, the constraint that does not move is space in good harbours. Prime superyacht berths in desirable locations are genuinely scarce, the supply cannot be conjured up quickly, and the operator collects on occupancy and berth sales regardless of which shipyard built the hull. Malta has actively leaned into this, with the government pursuing a long-standing policy to make the island a superyacht-friendly destination. So in theory you are buying a slice of the dock itself, the chokepoint that every one of those 100 metre boats eventually needs.

Now the caveats, and they are significant. This is a micro cap in the truest sense. As of May 2026 the stock traded around 1.19 and the entire market capitalization was roughly 24 million dollars, on trailing twelve-month revenue of about 9.4 million. That tininess brings everything you would expect: the stock is thinly traded, listed on the Malta Stock Exchange rather than a deep liquid market, and any position is hard to build or exit without moving the price. The financial performance also partly depends on the timing and number of berth sales, which makes results lumpy from year to year. One offsetting positive worth noting is the income. The shares have carried a high dividend yield, recently in the double digits, though with a micro cap you always have to ask how durable a payout like that really is.

So I would not build a thesis around it, and I am not pretending it belongs in the same tier as the Italian builders. But if what you want is the single most direct, undiluted exposure to the act of parking a superyacht somewhere expensive in the Mediterranean, this is close to the only listed way to get it. Treat it as a curiosity and an honorable mention: a tiny, illiquid, pure-play bet on the scarcity of the dock, suitable only for someone who understands exactly what a micro cap entails and sizes it accordingly.

Misc.

Beyond those names, I also looked into all of these:

Close Brothers Group plc (CBG.L, London Stock Exchange)

Garmin Ltd. (GRMN, NASDAQ)

Chugoku Marine Paints, Ltd. (4617.T, Tokyo Stock Exchange)

AkzoNobel (AKZA.AS, or OTC: AKZOY, Euronext Amsterdam)

PPG Industries (PPG, NYSE)

Gurit Holding AG (GURN.SW, SIX Swiss Exchange)

Hexcel Corporation (HXL, NYSE)

Toray Industries (TRYIY, or 3402.T, Tokyo)

Rolls-Royce Holdings (RR.L, London Stock Exchange)

OneWater Marine (ONEW, NASDAQ)

Catana Group (CATG.PA, Euronext Paris)

Fountaine Pajot (ALPAJ.PA, Euronext Paris)

Grand Banks Yachts (G50.SI, Singapore Exchange)

They are all related to the trend in some way, but most of them either fall outside the large yacht end of the market or are not pure play enough to earn a full write up. I am leaving them here in case anyone wants to go through them themselves. Think of them as an extension of the same thesis rather than the heart of it.

The connecting logic is worth spelling out, because it is really the second half of the story. The trend does not stop at billionaires buying mega yachts. It cascades downward. As social media makes the water look like the place everyone is supposed to be, the middle class and upper middle class start spending outsized chunks of their income to get a taste too. That is where most of these names come in. Instead of a 100 metre custom build, it is a financed boat, a chartered catamaran, a fractional share, a week split between friends. The money is smaller per head but the population is vastly larger.

You can see how each of these slots into that wider funnel. Catana and Fountaine Pajot build the cruising catamarans that increasingly fill the charter fleets, which is exactly the rental democratization I described earlier. OneWater Marine is another US boat retailer in the same vein as MarineMax, riding the broader ownership wave. Close Brothers touches marine lending and finance, the plumbing that lets people buy boats they could not pay for outright. Garmin sells the marine electronics that go on almost everything that floats. Rolls-Royce, through its MTU engines, sits in the propulsion of large yachts among many other things. Grand Banks builds at the more traditional motor yacht end.

Then there is a whole cluster tied to one specific input: advanced materials and marine coatings. Chugoku Marine Paints, AkzoNobel and PPG all supply the paints and coatings that every hull needs. Gurit, Hexcel and Toray supply the composites and carbon fibre that make large, light, structurally demanding builds possible, and this is the same carbon fibre story behind those big sailing yachts I mentioned earlier, where the structural engineering is the whole flex. These are the picks-and-shovels names, the trouble being that for almost all of them, marine is only a sliver of a much larger and unrelated business, which is precisely why they did not make the main list.

So treat this section as a research starting point rather than a set of recommendations. The pure-play, large-yacht-exposed names are the four I covered in depth. Everything here is a wider, more diluted way to bet that the entire pyramid, from the billionaire at the top to the upper-middle-class family chartering a catamaran at the bottom, keeps growing.

The Thesis

So now the real question. What actually makes this opportunity interesting? Stating that the number of mega yachts and the amount of luxury on the water has increased over the past ten years does not, on its own, warrant a thesis. It is what happens from here that matters.

Right now the prevailing narrative in the field goes roughly like this. Things are going well, but we already saw the cyclical peak. Much of the recent spending gets attributed to covid and the liquidity that came with it. And the Iran crisis is read as a material dent in demand. Several of these points are true. But none of them actually weaken the real tailwinds driving the structural increase in demand.

Start with social media. Instagram is not going anywhere. If anything, as more and more younger, Instagram-native people start inheriting and earning serious money, the amount of capital flowing toward yachts increases rather than fades. Then layer on the demographic point from earlier. The number of tech-related millionaires and billionaires is still rising. And here is the part most people miss: essentially every yacht bought so far has been bought by pre-AI-boom wealth. The people getting rich off AI, or off something like SpaceX, have not even had time to start looking at yachts yet. That cohort is coming. Finally, as the industry matures, chartering becomes easier and more accessible than ever, pulling in an entirely new layer of demand from below.

Now look beyond the current tailwinds to what AI and robotics are likely to do to the global economy. I think two things are very probable. First, physical goods like yachts get cheaper to produce. If you have humanoids working around the clock on production lines, output stops being constrained by human labour capacity and becomes constrained mainly by energy. Second, and just as important for the long run, wealth keeps polarizing. As network effects and data moats compound across an AI-driven economy, a slice of society gets richer and richer. I am personally not very optimistic about the middle class in relative terms. So focusing on the very top of the pyramid, the mega yacht end, feels like the smarter approach rather than betting on the broad base.

To summarize what I think makes this opportunity real, there are two things happening at once. Most investors believe the sector is just seeing a short cyclical boom, fuelled by covid, that will fade. I think that read is wrong. The mechanism, as I see it, runs more like this: the more pictures and cultural relevance yachting accumulates, the more people are willing to overspend and pour their excess wealth into it. Yes, there may well be a local cyclical top. But I am having a genuinely hard time seeing how all this recent AI-driven wealth does not, at some point, find its way to mega yachts.

End Note

My personal view is that this sector is likely to prove very durable over the long term. Demand should continue climbing higher and higher. But at the same time, it is vital to stay focused on brand, because without a strong brand the margins are impossible to defend. On that front the current valuations look compelling.

The one thing to keep in mind is that the wealth driving this demand is highly sensitive to broader market moves. So while I believe this sector is a great place to park money over the long run, these stocks are also likely to take a beating in any serious market downturn. The two things are not in conflict. You can love the structural story and still expect a brutal drawdown if equities roll over, because the marginal yacht buyer feels the stock market in his bones.

If you liked this writeup, please share it. It helps surprisingly much. And if you have any questions, just ask.

NFA. This writeup is for informational and entertainment purposes only and reflects my personal opinions, not investment advice. I am not a licensed financial advisor. Everything here may contain errors, and nothing should be taken as a recommendation to buy or sell any security. The companies mentioned are ones I find interesting, and I may hold positions in some of them. Always do your own research and consult a qualified professional before making any investment decision. You alone are responsible for your money.