Similarweb Earnings Recap: AI and NRR Hope

Similarweb Earnings Recap: AI and NRR Hope

Today SMWB released earnings and the results look promising. The stock traded first up and then down on low volume. It seems like there aren’t very many eyes left on the name. Here are the key things that happened. I will dive into the key webcast items and thoughts on the earnings after.

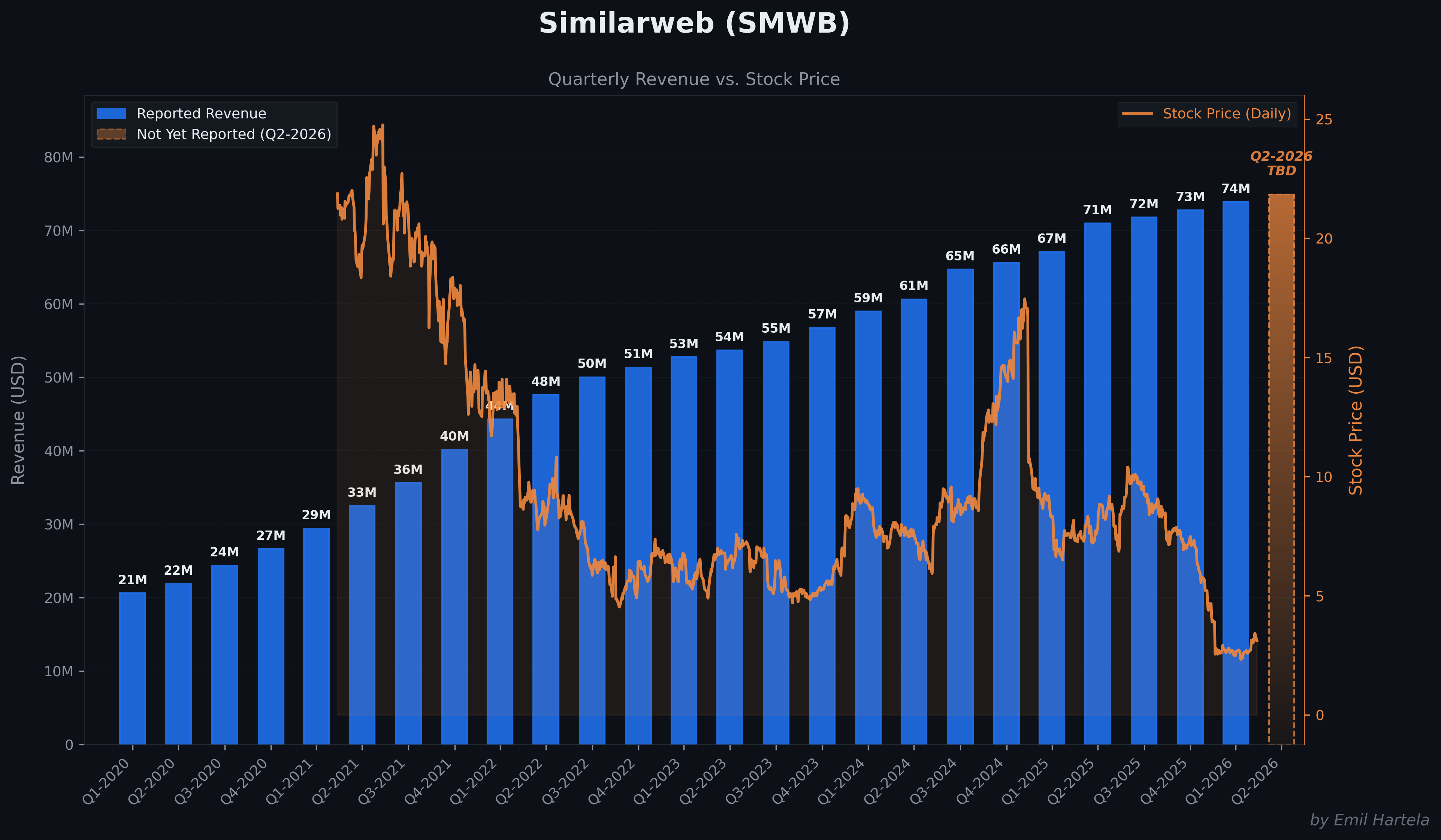

The headline numbers

Revenue $73,9M, up 10% YoY, at the top end of guidance. Non-GAAP operating profit $2,4M (3% margin) vs a $1,3M loss in Q1’25, also at the top end. Normalized FCF $6,6M, the 10th consecutive positive quarter. Non-GAAP diluted EPS $0,01 vs -$0,03 last year.

Guidance raised on the low end

Full year 2026 revenue guided to $307M–$315M (was $305M–$315M). Non-GAAP operating profit raised to $17M–$19M (was $16M–$19M). Q2 guided to $74,5M–$76,5M, implying around 8% YoY at the midpoint, with the H2 ramp doing the heavy lifting.

Multi-year contracts now 64% of ARR

Up from 52% in Q1’25 and 42% in Q1’24. Enterprises are locking SMWB in as infrastructure, not a discretionary tool.

RPO at $298M, up 18% YoY

Growing nearly 2x revenue growth. 70% expected to recognize within 12 months. The gap between bookings and recognized revenue mechanically forces revenue acceleration as bookings convert.

NRR stabilized; underlying point-in-time metrics already improving

Reported NRR 98% all customers, 103% for $100K+ ARR customers. Both flat for two quarters. Management explicitly disclosed that the trailing four-quarter average is masking improvement that has already happened in the underlying quarterly numbers. GRR hit a two-year peak in Q1.

$100K+ ARR customers grew to 461; average account value a new high at $383K

Both count and intensity expanded simultaneously. Customer base is moving up-market.

One of the two deferred LLM contracts closed in Q1

The second is still in the pipeline alongside multiple other large deals. Dedicated LLM/OEM sales team is the structural change.

MCP integration launched with ChatGPT

Same architecture as the Claude MCP connector announced last quarter. SMWB is now embedded directly into the two largest LLM platforms. Manus partnership also expanded with bidirectional MCP.

ChatGPT ads measurement product launching this quarter

Management claims SMWB is the first company in the world to bring LLM ad measurement data to market. New revenue line, no direct competitor.

Retail Intelligence and Ad Intelligence launched in March

Retail Intelligence covers 650+ retailers. Ad Intelligence covers paid media across search, social, display, with LLM ads being added now.

CEO Ofer announced he is stepping down by mid-2027

His 20-year milestone. External search starting now with a top executive search firm. He stays through the transition. No change to strategy, operations, or financial outlook.

Customer count metric is being retired

Total logo count (6,038, down 1% QoQ) is being replaced by $25K+ ARR cohort disclosure (1,840 customers, +2% YoY, $132K average account value, +9% YoY). The new cohort is 86% of ARR.

Buyback floated but no decision

$65M cash, no debt, accelerating FCF. Management said capital allocation is on the table once FCF strengthens further.

Now to the webcast details and what they actually mean.

AI and the LLM training pipeline

It really seems like SMWB is doing well on the AI data licensing side. One deferred LLM contract closed in Q1, a seven-digit deal with an existing big tech customer. The second large contract is still being worked, with multiple other large deals in the pipeline alongside it. A dedicated LLM and OEM sales team is now running point on this category. Or Offer on the call: “We started the year with a dedicated team only focusing on this large language model and original equipment manufacturer opportunities and they really executing very well.”

Worth remembering that part of why Semrush was bought at such a premium was the data itself. The data is the asset, not the dashboard. SMWB closing LLM training contracts is the cleanest possible validation that this data has structural commercial value to the AI buildout. If the data was generic or substitutable, LLM labs would not be writing seven-figure checks for it. The fact that they are, and that the pipeline keeps growing, points directly at the same thesis that justified the Semrush price tag.

Pricing model: consumption is working

CBO Maoz Lakovski clarified that SMWB does not price by seats and has not for a while; pricing is data access plus consumption layered on top. The shift is working. Or Offer addressed margins directly: “I think the margin are similar or even better in this consumption model because there’s no UI. So every time historically when customers used to buy data from us or API first they become more sticky and retention was better. But also they’re much more profitable because it’s more integrated into the workflow. So you need less customer success people to support those customers and they’re more sticky and there’s no UI on top of that.”

So consumption pricing means less platform overhead, fewer CS headcount, deeper workflow integration, and better stickiness. For an AI agent economy where agents do not buy seats but do consume data, SMWB’s monetization model is already structurally aligned with what’s coming. This is the kind of architectural advantage that does not show up in a single quarter but compounds for years.

NRR turnaround

This is the most important mechanical signal in the print. Reported NRR is a trailing four-quarter average. Or Offer: “The NRR we reporting to the street is the four-quarter average of NRR and we’re already seeing an improvement with our NRR and GRR in the past two quarters. That is not fully seen yet in the average. So we already know that the NRR is going to be better going forward.” And on GRR specifically: “the GRR that we saw in Q1 was the strongest in the last two years and we also, we didn’t of course share Q2 yet but we also seen the strength of the GRR continuing to be very strong in Q2.”

The 103% NRR for $100K+ customers is mathematically at or near the trough. The next 1–2 prints should show the average catching up to the underlying point-in-time improvement. If this plays out, Q1 marks the turnaround quarter for the business. That is the kind of inflection that does not get priced in until it is already in the reported number.

The Manus deepening

Manus deepened its partnership with SMWB today, expanding the data available to Manus AI agents (keywords, search traffic, incoming and outgoing referrals, landing pages, popular pages) and adding MCP server access for joint customers. The new data is available to all Manus Pro subscribers without additional setup. The fact that an AI agent platform chose to deepen rather than diversify, less than 5 months after the initial integration, is a strong signal that the data is genuinely valuable inside agent workflows. Mike Sadler, SVP of AI and Data Partnerships at SMWB: “In January, we gave Manus’s AI agent the ability to see who’s winning online. With this expansion, businesses can put AI agents to work obtaining deeper insights into the signals that turn a traffic snapshot into a strategy.”

If the integration was not generating real usage, Manus would not be widening the data surface. They are. That is a small but real second proof point that SMWB data is becoming infrastructure in the agent economy, not a side feature.

Buyback

Lucas from Needham asked about a buyback. Or Offer’s response: “We did discussed it. We don’t have a specific decision yet and it’s a good stuff to think about going and seeing how the year is progress but it’s definitely something that can be on the table.” He followed up: “Generating normalized free cash flow is a top priority. So we focus on that once we see also this trend picking up, as as mentioned earlier, we will consider all available options of capital allocation.”

My personal take is that the cash is more likely to be used for M&A and product investment than for buybacks. Management has been explicit about a disciplined M&A strategy focused on bolt-ons that strengthen the data asset or accelerate scale. With $65M in cash, no debt, and accelerating normalized FCF, capital priorities point toward consolidation moves. That said, a modest buyback is not off the table, especially if the stock stays cheap into H2. Worth noting the PMI hire as well; bringing in someone to drive Post-Merger Integration discipline points at a company that is preparing to deploy capital into acquisitions, not return it.

CEO stepping aside

Or Offer announced he will step down by mid-2027 at his 20-year service milestone. The framing was personal and durable: “My promise to myself and to my wife was always that When I reached 20 years of service, I realign my priorities and spend more time with my family.” This is not a forced exit; it is a founder hitting a life milestone he set for himself 20 years ago. He is staying through the transition and repeated three times that strategy, operations, and financial outlook are unchanged.

The question now is who replaces him. The search has been confirmed as external: “It will be external search and now that we announced to the street we can probably start the search. We’re ready. And top executive search firm is starting work today.” That is a meaningful variable. An enterprise SaaS veteran with strong commercial chops could accelerate the AI re-rating; a finance-oriented operator could slow it. Until the successor is named, this is an overhang on the multiple but not on the underlying business.

Retail Intelligence is the understated addition

Retail Intelligence covers 650+ retailers, combining Amazon IQ with Cross-Retail IQ across product mix, availability, pricing, competitive positioning, and emerging trends in a single intelligence layer. E-commerce is getting brutally competitive; brands and retailers are hungry for unified data that cuts through the fragmentation of marketplaces. This is the kind of product that quietly compounds over multiple quarters as customers discover they need it. It also fits naturally into the multi-product expansion narrative driving the NRR recovery.

I think this is going to be a sleeper hit. The combination of cross-retail coverage plus the existing customer base plus the AI Studio interface means SMWB can sell this into existing accounts with minimal friction. Expect this to show up meaningfully in the upsell motion over 2026.

Sales and marketing efficiency

S&M expense fell to 39% of revenue in Q1’26 from 44% in Q1’25, while revenue grew 10%. Lower spend, better productivity, more output. Or Offer was clear on the call that sales productivity has improved for the third consecutive quarter, with two separate commercial teams (new sales and expansion) both performing well. This ties directly into the GTM rebuild that has been underway for over a year; the team is now showing through in the numbers. Stronger productivity at lower S&M intensity is exactly what you want to see in a business approaching scaled profitability.

Other relevant

G2’s Spring 2026 report awarded SMWB 90 badges, with leadership recognition in 7 key categories including AEO, competitive intelligence, content analytics, SEO tools, digital advertising intelligence, market intelligence, and paid search intelligence. Independent validation of product leadership across the categories that matter most for the AI data thesis.

Deferred revenue grew to $117M from $112M sequentially. Cash and equivalents at $65M down from $72M at year-end, mainly due to a $6,5M payment for business combinations. Operating cash flow was thin at $0,2M but the normalization adjustment for that same $6,9M business combination payment is what brings normalized FCF up to $6,6M. Worth understanding that the FCF number is doing some work via add-backs this quarter.

Net take

The thesis got stronger, not weaker. AI data licensing is closing real deals. Consumption pricing is working and the margin structure is improving under it. NRR is mechanically set up to inflect over the next 1–2 prints. Manus deepening, ChatGPT MCP, and the ChatGPT ads measurement product all point to SMWB data becoming foundational to AI workflows. Retail Intelligence is a sleeper. Sales productivity is normalizing on lower spend. The new risk is the CEO transition, which is a real overhang but not a thesis-breaker.

Q2 print is the next catalyst window. Reported NRR should tick up, the second LLM deal may close, the CEO shortlist may emerge, and Q3 guidance will tell you whether the H2 ramp is real. There is value in the data; the market just hasn’t priced it yet.

Thoughts going forward

If one believes in the fact that SMWB data will be more valuable in the AI landscape, not less, this was a great quarter. At the current EV/S the stock is genuinely cheap. There are multiple ways where things could go right; either they just continue executing on the AI pivot and larger customers and re-price once the AI thesis is understood, or they get bought at a nice premium in the near term. I am pretty sure there are multiple companies that would love the data and the edge they can get in the AI race.

The setup is asymmetric. On the upside, you have a business with locked-in revenue acceleration through RPO conversion, a mechanical NRR inflection that is already happening in the underlying numbers, a consumption pricing model structurally aligned with the agent economy, dual MCP integration across Claude and ChatGPT, and a first-mover position in LLM ad measurement. Each of these alone is worth something; together they describe a company whose data is becoming infrastructure for the next wave of computing.

On the downside, the floor is meaningfully higher than the multiple suggests. Ten consecutive quarters of positive normalized FCF, 80% gross margins, $65M in cash with no debt, 64% of ARR locked in multi-year contracts, and a customer base moving up-market. The business does not need a heroic outcome to compound from here. It just needs to keep doing what it is already doing.

The acquisition optionality is real. Strategic buyers who would benefit from owning the data layer include large data and analytics platforms looking to defend their relevance in an AI-native world, advertising and media measurement companies that need digital intelligence to stay competitive, large enterprise software vendors that want to embed market intelligence into their workflows, and the LLM labs themselves who already pay seven-figure sums for the training data. A private equity buyer with a roll-up thesis around digital data and AI measurement would also see the math work, especially given the FCF profile and the multi-year contract base providing predictable cash flow.

The CEO transition actually slightly increases acquisition probability. Founder-led companies are harder to buy; a founder who has just announced his departure window is a different dynamic. Whether intentional or not, the next 12–18 months are a structurally easier period for a strategic buyer to make a move.

The path I am underwriting is the organic one. Continued execution on the AI pivot, the second LLM deal closing, NRR inflecting in the reported number over the next 1–2 prints, Retail Intelligence quietly compounding, and the market eventually catching up to what the leading indicators have been saying for two quarters. The acquisition outcome is a free option on top.

Either way, the data has value. At this multiple, you are not paying for it.

Disclaimer

Not financial advice. I own SMWB and am clearly biased. Do your own work, form your own thesis, size your own positions. I am not your fiduciary and this post is not a recommendation to buy, sell, or hold any security. Markets can stay irrational longer than any thesis can stay intact; the bull case I laid out can be wrong, and the risks I flagged can be larger than I think. If you act on anything written here without doing your own independent work, that is on you.