ServiceNow Deep Dive $NOW

The Company Harness That Outlives Its Employees

For the last eight years or so I have had this itch for one simple idea. A company harness.

Probably the biggest problem any company faces is knowledge loss and value retention in its employees. Companies can suffer massive losses from a few key people retiring or being poached by competitors. Key strategies get lost, or worse, acted on blindly by the next person taking over. Over time the constant churn of employees makes companies rot. This is especially true in larger companies, where complexity compounds. Why are things done the way they are? Who is in charge of this? Where is that decision documented? Nobody knows, because the person who knew left in 2019.

The solution to this problem is pretty straightforward in theory but hard to offer as a service. You need a layer that sits above the employees themselves. A persistent operational substrate that captures how the company actually works; the approvals, the rules, the routing, the exceptions; and keeps it intact regardless of who comes and goes. A harness for the company.

There is one publicly traded business that has been quietly building exactly this for over twenty years. It is so well positioned to own this layer for the next several decades that I believe it will eventually become one of the most valuable companies on earth. That company is ServiceNow.

In this deep dive I will walk through every aspect of the thesis in detail; what they actually sell, why the harness framing matters, how the agentic transition accelerates rather than threatens the moat, where the real risks lie, and why I believe the market is currently mispricing the entire setup.

What ServiceNow Actually Does, and How They Make Money

Before getting to the thesis, it is worth slowing down and explaining what this company actually sells. ServiceNow has a branding problem; not in the sense that the brand is weak, but in the sense that the brand is so generic that almost nobody outside of large enterprise IT has any clear picture of what the product is. So let me strip away the marketing language and explain it plainly.

ServiceNow sells a workflow engine. That is the simplest possible description and it is more or less the whole truth. Every large company runs on thousands of recurring sequences of decisions; an employee asks for access to a system, a server fails and someone needs to fix it, a customer files a complaint, a new hire joins, a vendor gets onboarded, a security alert fires. Each of these is a workflow. In most companies, these workflows live in a chaotic mess of emails, spreadsheets, Slack threads, and tribal knowledge. ServiceNow gives the company one place to encode all of them, with proper approval chains, audit trails, integrations to every other system, and a single interface for the people involved.

The platform underneath all of this is called Now Platform. It includes a configurable database that models everything in the company; every employee, every laptop, every server, every contract; plus a no-code workflow builder that lets the customer encode “when X happens, do A, then route to B for approval, then trigger C in SAP, then log the result.” On top of this platform, ServiceNow has built five major product lines that they sell as separate modules.

The original and still largest module is IT Service Management, usually shortened to ITSM. This is the system the IT helpdesk runs on. When your laptop breaks at a Fortune 500 company and you submit a ticket, that ticket almost certainly lives in ServiceNow. ITSM handles the full lifecycle of IT support; incident management when something breaks, change management when production systems are being updated, problem management when something keeps breaking, and request fulfillment when employees need access to new systems. This is where ServiceNow started in 2004 and it remains the foundation of most customer relationships. People pay for ITSM because the alternative is running IT support out of email and shared mailboxes, which works for a startup and falls apart at scale.

The second module is IT Operations Management, or ITOM. If ITSM is about the human-facing tickets, ITOM is about understanding the actual technology underneath. ITOM discovers every server, database, and application running in the company, maps how they depend on each other, and monitors their health. The data structure that holds all of this is called the CMDB, the Configuration Management Database. When the company’s trading platform goes down at 3am, ITOM tells the engineers which underlying server failed and which downstream systems are affected. People pay for ITOM because in a company with twenty thousand servers across three clouds and a hundred internal applications, nobody can actually keep that map in their head.

The third module is Customer Service Management, or CSM. This is the same workflow engine pointed outward at customers instead of inward at employees. When a customer of a telco files a complaint, or a corporate customer of a software vendor opens a support case, CSM routes it, tracks it, escalates it, and connects it to the underlying systems needed to resolve it. This is ServiceNow’s direct attack on Salesforce Service Cloud and Zendesk, and it is strategically important because it is where the company expands beyond its IT origins into the broader enterprise.

The fourth module is HR Service Delivery, sometimes called HRSD or just HR. Same workflow engine, applied to HR. When employees ask “what is my parental leave policy,” “I need to update my emergency contact,” “I am referring a candidate,” HRSD handles the case management, knowledge base, and routing. Note that this is not a replacement for Workday; Workday is the database of employees and payroll, HRSD is the service and workflow layer that sits next to it. People pay for HRSD because the HR team is otherwise drowning in email asking the same fifty questions over and over.

The fifth module is Security Operations, or SecOps. Workflow engine pointed at the security team. When the company’s security tools flag a potential intrusion, SecOps automates the response; pull the threat intelligence, check if the affected machines are critical, route to the right analyst, trigger containment actions, log everything for the post-mortem. People pay for SecOps because security teams cannot scale linearly with the threat surface, and orchestration is the only way to keep up.

Across these five modules there is a horizontal layer worth understanding called App Engine. This is the low-code part of the platform that ServiceNow sells to customers who want to build their own custom workflow applications, beyond the prepackaged modules. Large enterprises end up with hundreds of custom apps built on Now Platform; for managing legal contracts, tracking facilities maintenance, running internal R&D processes, whatever the customer needs. App Engine competes head-on with Microsoft Power Platform and Salesforce Platform.

Sitting on top of all of this for the last two years is the AI layer, branded as Now Assist and increasingly as Otto following the Knowledge 2026 conference. This generates incident summaries, drafts responses, accelerates the workflow builder, and increasingly executes work autonomously through AI agents. ServiceNow has also introduced AI Control Tower to govern AI agents across the enterprise and Action Fabric to let external agents (Claude, Copilot, custom-built ones) trigger ServiceNow workflows through a Model Context Protocol server. This AI layer is sold as separate SKUs on top of the base modules, which matters enormously for the financial story because it is the primary vehicle for ARPU expansion in the next five years.

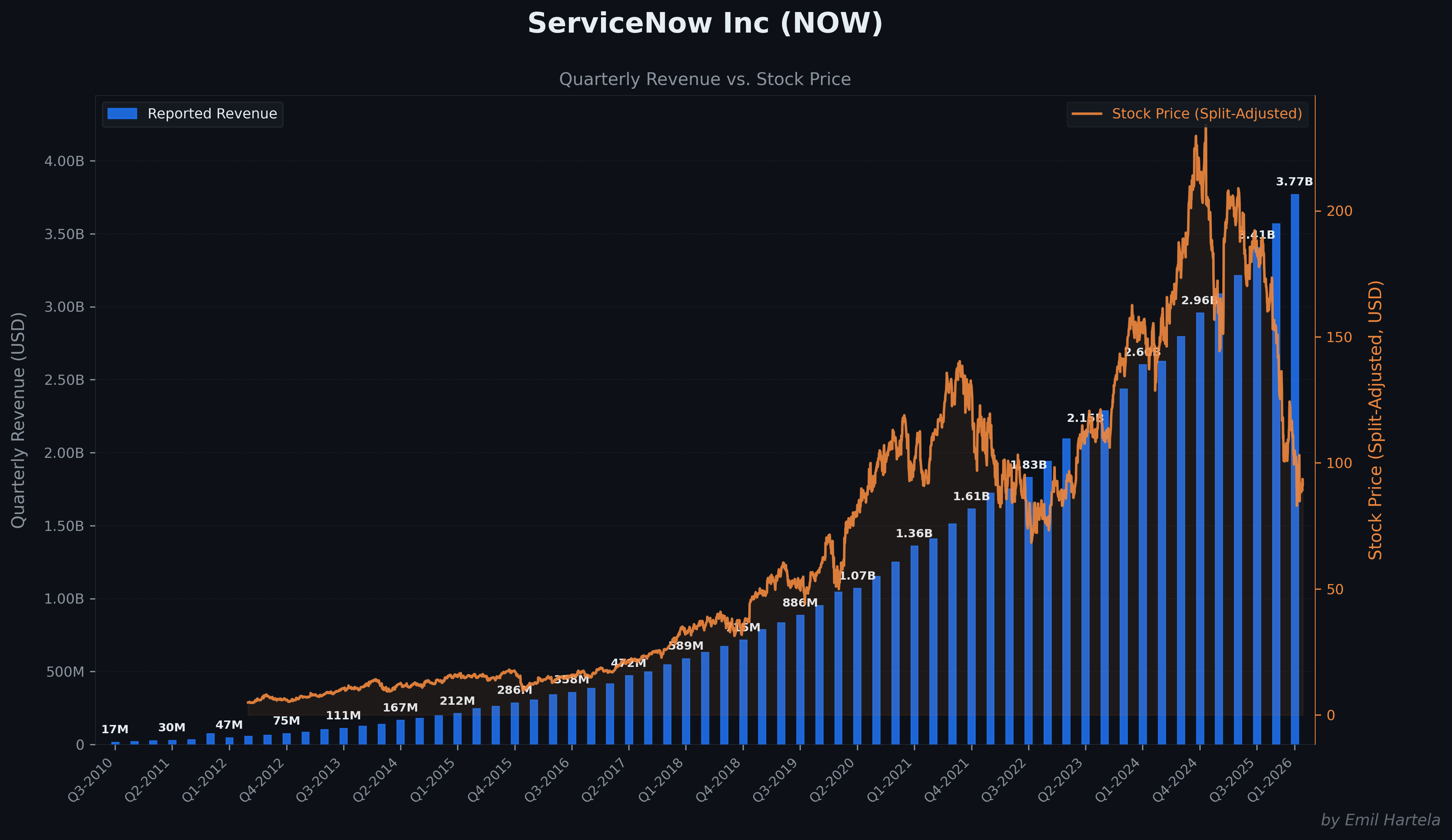

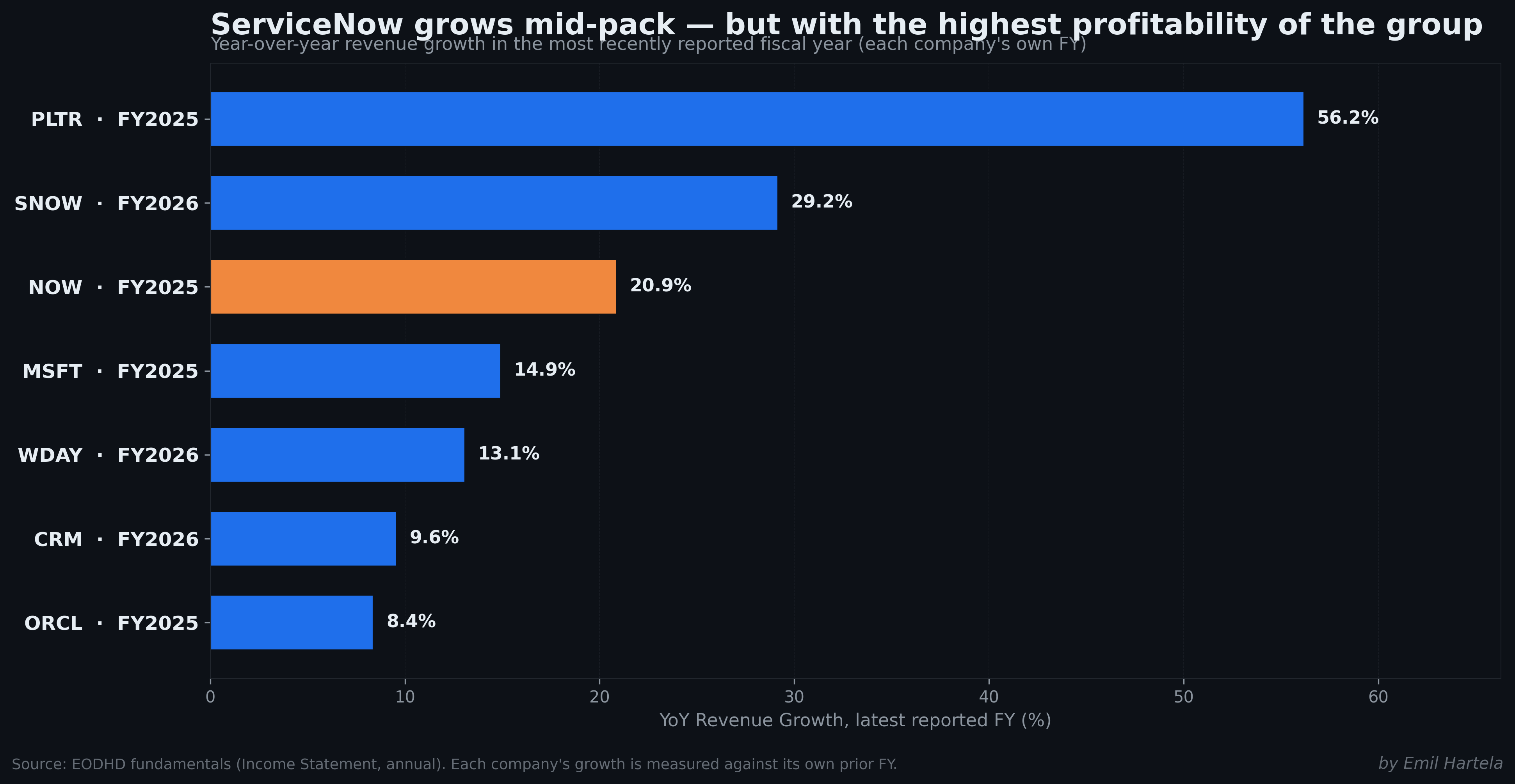

Now to how the money actually flows. ServiceNow is a subscription business. Customers pay annual contracts, typically priced per-user-per-month, with separate SKUs for each module they activate. A typical large customer starts with ITSM for a few thousand users, then over time adds ITOM, then HRSD, then CSM, then SecOps, then layers in Now Assist on top of all of it. Total contract values for the largest customers run into the tens of millions of dollars per year. The company reported trailing twelve month revenue of roughly fourteen billion dollars and they have been growing in the high twenties annually, which for a business of this scale is genuinely remarkable.

But the number that matters most is not revenue or growth. It is net revenue retention, which measures how much existing customers expand their spend year over year. ServiceNow consistently reports this above 125%, and at the top end of the customer base it is meaningfully higher. Said plainly, every existing customer spends roughly a quarter more next year than this year, before any new customer wins. That metric is the entire business in one number. It tells you that the typical customer experience is not “we bought ServiceNow and that was that,” it is “we bought ServiceNow for IT and now we keep finding new things to put on it.”

Which brings us to the stickiness. This is the part most analysts understate. ServiceNow is not sticky because it is good software, although it is. ServiceNow is sticky because of what the customer encodes into it over time. The first year a bank rolls out ServiceNow, they configure ITSM to match their support process. The second year they add HR workflows for onboarding. The third year they integrate it with their compliance system. The fourth year they build twenty custom apps on App Engine for their trading desk. The fifth year they encode their entire change management policy with seventeen approval gates that match their regulatory requirements. By year seven, the company runs on ServiceNow in a way that is impossible to replace without ripping out and rebuilding the operational logic of half the company.

This is why gross retention rates at ServiceNow run above 98%. Customers do not leave. They cannot leave. The platform is not just storing their data; it is storing the encoded shape of how they actually work. Replacing it would mean rewriting the company’s operating procedures from scratch, retraining tens of thousands of employees, and rebuilding integrations to every other system in the stack. No CIO has the budget, the political capital, or the appetite to do that voluntarily. The few cases where companies have tried have generally failed and ended with the company quietly returning to ServiceNow.

This combination, broad cross-sell across five modules, an AI layer that creates a new monetization vector on top, net revenue retention above 125%, and gross retention above 98%, is what produces ServiceNow’s financial profile. It is a business that is mathematically very hard to break once it is installed, and that compounds organically through expansion even before the company wins a single new logo. The harness, in other words, is also a very good business model.

Next I will walk through the bull thesis, and after that risks and deeper due diligence. But before that, a quick note.

I am an independent stock researcher. I publish deep dives on a small handful of companies and track them alongside my own portfolio. I specialize in research that is borderline obsessive, and I run a highly concentrated book; the kind where every name has to earn its slot against the others. If that style of work is what you are looking for, subscribe to the Substack for ongoing updates on $NOW and for new ideas outside of this name as they come.

Now to the bull thesis.

The Bull Thesis

Imagine a future where every large company on earth has not just thousands of human employees doing their daily work, but also millions of AI agents running alongside them, each handling their respective tasks end to end. This is not a hypothetical. It is already happening. More and more teams are getting more and more done with agents that complete real work, not just suggest it.

The main problem this creates is not capability. It is coordination. Auditing what was done and by whom. Tracking how different parts of the organization interact with each other. Understanding which agent is operating under which permissions, with which context, and answering to which human. Thousands of employees and millions of agents running in parallel creates a coordination problem that no large enterprise has the infrastructure to solve today.

This is where ServiceNow comes in. What they are building, piece by piece, is exactly that infrastructure. A harness for the agentic enterprise. The same way you currently need a small harness to run a few AI agents inside a single team or function, ServiceNow is building it at the scale of the entire organization. The substrate that holds everything together as the moving parts multiply.

There are four structural trends pushing every large organization toward needing this kind of harness, and each of them is independently durable. Together they form the strongest version of the bull case.

The first trend is rising organizational complexity. As network effects and stronger moats have concentrated capital and revenue in fewer and fewer companies, the number of sub-tasks, processes, integrations, and dependencies inside those companies has grown almost exponentially. The more moving pieces a system has, and the more rapidly it evolves, the more demand there is for a layer that holds the substrate together. This is not a trend that is going to reverse. Complex systems walk toward entropy by default; the only way to keep them functional is to add coordination infrastructure on top. The demand ServiceNow has captured over the past two decades came from the complexity introduced by computers, the internet, and the proliferation of SaaS tools each speaking their own language. The next leg of demand comes from AI and agents being integrated into organizations at a scale that makes the previous wave of complexity look small.

The second trend is the maturity of big tech and the broader push for efficiency. The companies that built and scaled aggressively over the past twenty years are now in a different phase. Investors are demanding more efficiency, higher returns on invested capital, and tighter operating leverage. Management teams are responding by automating tasks and reducing headcount where possible. We are already seeing this play out across multiple sectors. The end state of this efficiency push is not “fewer people doing the same work.” It is “the same work being done by a mix of humans and agents, with the harness deciding which one runs which task.” That harness has to come from somewhere. ServiceNow is the most obvious candidate.

The third trend is the aging workforce and the institutional knowledge cliff. This one is less talked about but in some ways the most important. As more and more senior employees approach retirement at large enterprises, those companies face a knowledge loss problem at a scale they have never had to manage before. Processes that have been run for thirty years by the same person, with all the context and exception handling living inside that person’s head, need to survive the transition to the next generation. Spending the last productive years of a senior employee’s career explaining to their replacement how every process works is slow, wasteful, and lossy; a meaningful percentage of the knowledge does not survive the handoff. By encoding those processes into a system that intelligently tracks each task and maps how it interacts with the rest of the organization, companies can compress that transition time and preserve the operational logic. The harness becomes the institutional memory.

The fourth and most important trend is that agents themselves require a harness to work properly. For an AI to operate effectively inside a large organization, it needs context. We are already at the stage where agents can perform long-running tasks and contribute meaningfully to real work. But a major unresolved problem is ownership. If an agent sits under a single person, isolated from the wider organizational context, you are not getting the full value of the agent. To get the full value, the agent needs the freedom to operate the way a competent employee operates; talking to other employees, talking to other agents, accessing the systems it needs, escalating when it should. The risk in that freedom is that without a proper harness, auditability and accountability become impossible. Companies need to know how much each agent is spending, what it is doing, what assumptions it is operating under, and on whose authority. No CIO is going to deploy autonomous agents at scale without that infrastructure in place. The harness is not a nice-to-have for the agentic enterprise. It is the precondition for it.

To summarize the bull thesis, what we are looking at is a future where the demand for a company harness that allows for seamless AI integration alongside human employees will be vital and rapidly growing. The four trends driving this demand, complexity, the efficiency push, the knowledge cliff, and agent governance, are each large on their own. Stacked together, they form one of the most durable demand tailwinds in enterprise software for the next decade. There is essentially no plausible scenario in which a large organization decides not to implement this kind of layer. The only open questions are who builds it and how much they get to charge for it.

ServiceNow is the incumbent answer to both questions. Whether they can hold that position is what we will look at next, when we move to competition and risks.

Competition

With a massive opportunity comes strong competition. In a technical sense, ServiceNow likely has hundreds of companies competing with them across different parts of the business. However, for the bull thesis, meaning the question of which company will become the dominant harness inside large enterprises, only a handful of companies are actually relevant. These companies have the size, existing moats, and customer relationships that are hard to replace and that give them a real edge in the race. All of them are credible competitors, and I will now try to cover each of them in an unbiased way; first by laying out why they could pose a real threat, then by explaining why I believe ServiceNow is still favorably positioned to win.

Microsoft

Microsoft is the most credible threat by a wide margin. Their attack on the harness layer is built on three stacked pieces. Power Platform is the workflow engine. Copilot Studio is the agent builder. Microsoft 365 plus Azure is the distribution moat. The pitch to the customer is direct and powerful; if your employees already live in Teams, Outlook, and SharePoint, and your developers already live in Azure, why pay for a separate harness when Microsoft can fold the whole thing into the existing bundle.

The case for Microsoft as the eventual winner is real. They have 400 million paid Microsoft 365 seats, which is structural distribution that nobody else in this race can match. They have been steadily expanding Power Platform into territory that overlaps directly with ServiceNow, including process mining, agent orchestration, and prebuilt agents for HR, IT, and customer service workflows. Their bundling power means they can effectively give workflow capabilities away alongside M365 and Azure renewals, which makes the cost comparison favorable on paper. For mid-market customers and newer enterprises that never built a deep ServiceNow installation, Microsoft has a genuine shot.

The case for why ServiceNow still wins comes down to the depth of encoded enterprise workflow at the largest, most complex, most regulated customers. Power Platform is excellent for relatively simple, departmental, often Microsoft-centric automations. It is significantly weaker at the deeply governed, regulator-grade, cross-system, decades-encoded workflow logic that runs at a global bank or a Fortune 100 manufacturer. Twenty-two years of accumulated complexity at a Tier 1 bank cannot be casually rebuilt in Power Platform; the workflows span SAP, Workday, Oracle, custom systems, and ServiceNow’s own modules, with compliance audit trails and approval chains tied to specific regulatory frameworks. Microsoft can theoretically rebuild this. They have not, and the customers that have tried have generally ended up either supplementing Power Platform with ServiceNow or building so much custom code that the cost advantage evaporates.

There is also a useful structural tell. Microsoft Copilot Studio ships with deep connectors into ServiceNow. The Employee Self-Service Agent ships with prebuilt ServiceNow integrations. Microsoft is implicitly acknowledging that they cannot displace ServiceNow from the workflow execution layer in the short term. Their actual play is to own the conversational and productivity layer and gradually pull execution back into Power Automate over time. That works in some accounts and not in others, and it does not threaten the harness position in the largest, most complex enterprises in the world; which is precisely where the harness is most valuable.

The honest summary on Microsoft. They will win the productivity agent battle. They will win at mid-market and at customers where Microsoft is already the dominant stack. They will not, in the next five to seven years, displace ServiceNow at the harness layer of large regulated enterprises, and that is exactly the customer base where the harness thesis pays off.

Salesforce

Salesforce is the second credible threat, narrower than Microsoft but more directly competitive in the modules they overlap on. Their attack is concentrated in Customer Service Management, where Service Cloud has long been the incumbent, and where Salesforce has now layered Agentforce as the agentic AI offering. Marc Benioff has been openly aggressive about positioning Agentforce as the platform for autonomous customer service agents, and Salesforce has the largest installed base in customer-facing service software.

The case for Salesforce as a real threat is straightforward. They own the customer-facing workflow incumbency. They have a massive sales-led customer base. They are extending inward toward employee-facing workflows in the same way ServiceNow is extending outward toward customer-facing service. The two companies are running mirrored expansion strategies and they meet most directly in CSM, which is one of ServiceNow’s fastest growing modules.

The case for why ServiceNow still wins this race is more nuanced than the Microsoft argument. Salesforce is not building a harness; they are building a stronger CRM stack with agents on top. That distinction matters because customer service tickets in many large enterprises ultimately depend on resolving an underlying technical or operational issue. When a corporate customer calls because their banking platform is down, the ticket may start in Service Cloud, but the resolution requires touching the incident, the change management record, the affected systems, and the field service dispatch; all of which sit in ServiceNow at most large enterprises. ServiceNow’s pitch is that you should run the entire loop on the harness rather than handing off between two platforms. Increasingly, that pitch is winning at the largest, most operationally complex customers.

The honest summary on Salesforce. They will continue to be a real headwind on ServiceNow’s CSM growth rate, particularly in pure customer-facing service deployments where the operational complexity is low. They are not building a harness, and the harness thesis does not turn on the CSM module specifically. ServiceNow loses some CSM deals and the bull thesis still works.

Workday

Workday is the smallest of the three threats today but worth flagging because the trajectory is right. They are the system of record for HR and finance at most large enterprises, and they have been steadily extending into HR service delivery and financial workflow automation. That puts them in direct competition with ServiceNow’s HRSD module and increasingly with their finance workflow ambitions.

The case for Workday is rooted in data ownership. They argue, with some logic, that if they already hold the employee data and the financial data of record, they should be the natural place to run workflows on top of that data. For customers where Workday is deeply entrenched, this argument resonates and ServiceNow has lost some HRSD deals as a result.

The case for why ServiceNow still wins is structural. Workflow logic is fundamentally different from data of record, and the same workflow engine should run across HR, IT, finance, customer service, security, and custom domains. You cannot solve the harness problem if you only own one vertical’s data. Workday’s architecture and DNA are oriented around being a system of record, not a system of action; that is what they are good at and what they will continue to be good at. The two companies are largely complementary at the scale of large enterprises, and most customers buy both.

The honest summary on Workday. They are a real but contained threat in the HRSD module specifically. They are not building a harness, and they are not architecturally positioned to do so. ServiceNow loses some HRSD deals at Workday-heavy accounts and the bull thesis still works.

Smaller players and Palantir

A note on the second tier of competitors. Atlassian Jira Service Management, BMC Helix, Ivanti, and Freshservice all compete with ServiceNow in IT service management at the lower end of the market. They take some helpdesk share at mid-market and smaller enterprises. None of them are remotely positioned to become the harness for a large enterprise; their architectures, customer bases, and product depth are not in the same league.

Palantir deserves a separate note because investors familiar with both names will inevitably ask. Palantir is not a competitor to ServiceNow in any meaningful sense. They are solving a different problem at a different layer of the enterprise. Palantir’s Foundry and AIP are decision support and intelligence layers that fuse data and let humans or agents reason over it for hard, high-stakes problems; defense, supply chain optimization, clinical trial monitoring, and similar. ServiceNow is the operational substrate that runs the recurring, governed, auditable execution of work across the entire organization. The cleanest framing is that Palantir is the brain and ServiceNow is the spine. The largest enterprises in the world increasingly run both, and the products complement each other far more than they compete. Anyone framing this as a Palantir-versus-ServiceNow trade is misreading the architecture.

The race overall

This is a real, ongoing race, and the heat will only increase over the next several years as the agentic enterprise becomes the default architecture. Microsoft, Salesforce, and Workday are each formidable in their own zones. Each has a credible angle of attack on some part of ServiceNow’s surface area.

But ServiceNow has the strongest head start and the clearest vision of what the harness actually needs to be. Twenty-two years of encoded workflow at the largest enterprises in the world. The deepest cross-functional module footprint of any platform in this space. The most credible AI control tower and agent governance story. And, crucially, the only architecture in this race where workflow is the entire product rather than a feature bolted onto something else.

The competitive landscape does not invalidate the harness thesis. It sharpens it. The race is real, and ServiceNow is leading it.

Next up we will take a look at the team and leadership to determine skin in the game and important connections.

Leadership and Skin in the Game

For ServiceNow to get to the next stage, strong leadership and skin in the game are vital. In this section I will go over the key figures in the company, insider ownership patterns, and the key signals that either support or weaken the bull thesis.

Fred Luddy, the founder and Chairman

ServiceNow was founded in 2003 by Fred Luddy, working alone out of his home in San Diego. Luddy had previously been the Chief Technology Officer of Peregrine Systems, an enterprise IT software company that had collapsed a year earlier. Rather than retire, Luddy started ServiceNow at the age of 49, famously telling colleagues he could not wait until 50 because he had decided 50 was too old to start a company.

The original vision was characteristically unfashionable. Luddy was not trying to build a category-defining IT product. He was trying to build a generalizable workflow platform in the cloud, which essentially nobody understood at the time. To get the platform adopted, he layered an IT service desk product on top of it because that was a pain point customers could feel and pay for. The IT service desk became ITSM, ITSM put ServiceNow on the map, and the underlying platform became the substrate everything else has been built on for the past two decades. The harness, in other words, was Luddy’s actual original vision, and the IT module was just the wedge to get it sold.

Luddy served as CEO from 2004 to 2011, then stepped aside voluntarily when the company needed an operator to scale the sales motion. He moved into product development, then into an advisory role in 2016, and became Chairman of the Board in 2018. He still holds a meaningful family-trust stake in the company and remains the cultural anchor; Bill McDermott routinely references Luddy as the source of the “humble, customer-first” culture that runs through ServiceNow’s 27 000 employees.

What is worth flagging here is that ServiceNow is one of the very few enterprise software companies where the founder handoff actually worked. Most founders either cling on too long and become a drag, or hand off and the culture rots. Luddy did neither. He stepped back at the right time, kept his identity tied to the company through governance and equity rather than through running it, and let a series of best-in-class operators take the company through each scaling phase. That is a rare pattern and it is itself a signal of organizational health.

The CEO succession nobody talks about

Before getting to the current CEO, the succession history at ServiceNow is worth pausing on because it is unusually clean and tells you something about the quality of the underlying business.

Luddy was followed by Frank Slootman, who ran the company from 2011 to 2017 and took it public in 2012. Slootman is now the CEO of Snowflake and is widely considered one of the most ruthlessly effective enterprise software operators alive. He was followed by John Donahoe, the former CEO of eBay, who ran ServiceNow from 2017 to 2019 and is now CEO of Nike. Donahoe was followed by Bill McDermott, the former CEO of SAP.

Stop and notice the pattern. Every CEO of ServiceNow has been a top-tier operator who went on to lead another major public company afterward. ServiceNow has effectively become a CEO factory. That does not happen at average businesses. It happens at businesses that attract elite talent because the underlying platform is doing something genuinely important, and where the bench and the board are deep enough to keep the succession working. The leadership pipeline itself is a piece of evidence for the bull thesis.

Bill McDermott, the current CEO

Bill McDermott took over as CEO in late 2019 and added the Chairman title in October 2022. He is American, born in New York in 1961, and his career trajectory through enterprise software is among the most impressive of any operator in the industry.

He spent the early part of his career at Xerox, where he climbed into senior sales and management positions. From there he moved to Gartner as President, then to Siebel Systems as Executive Vice President during the period when CRM was being defined as a category. He then joined SAP America, where his performance got him appointed the first American co-CEO of SAP in 2010 and then sole CEO. During his tenure at SAP, the market capitalization went from roughly 39 billion to 163 billion dollars. He led SAP’s transition to the cloud, which is exactly the kind of platform-shift execution that ServiceNow now needs to pull off with the agentic transition.

McDermott left SAP in 2019 with a specific mandate at ServiceNow; take the company from 3,5 billion in annual revenue to 10 billion. He hit that mark and kept going. Annual revenue under his tenure has gone from 3,5 billion in 2019 to roughly 13,3 billion in 2025, with the company on track to exceed 15 billion this year. The company has more than tripled in revenue under his leadership while also entering the Fortune 500 and consistently winning best-place-to-work and most-trusted-business rankings. Whatever you think of the stock, the operating execution has been exceptional.

McDermott’s personal style is worth understanding because it shows up in how the company is positioning for the agentic era. He is a relentlessly customer-focused, narrative-driven CEO who is willing to make bold strategic claims publicly and then drive the company to deliver on them. His Knowledge 2026 framing of ServiceNow as the “AI control tower for business reinvention” is exactly the kind of high-conviction, slightly-ahead-of-the-product positioning that built SAP’s cloud transition. He is also notably aggressive about defending the company in public; in May 2026 he gave a Fortune interview pushing back hard on the “SaaSpocalypse” narrative that has driven the stock down, calling the bear case nonsense and arguing ServiceNow is on a path to a trillion dollar market cap.

The honest assessment of McDermott is that he is exactly the right CEO for this phase of ServiceNow’s life. He is not a founder. He does not pretend to be. He is the operator hired to take a great platform and turn it into a defining enterprise software company, and his track record at SAP says he is one of perhaps three or four people on the planet qualified to do this job at this scale.

Gina Mastantuono, the CFO

It is worth flagging the CFO because in a business with this much expansion and so many capital allocation decisions, the CFO matters more than usual. Gina Mastantuono joined ServiceNow as CFO in January 2020, brought in by McDermott shortly after he started. She has been the financial architect of the revenue tripling, the margin expansion, and the recent aggressive share buyback program. She is widely respected in the enterprise software CFO community and represents continuity in the financial discipline the company has been known for.

The skin-in-the-game signal

This is where the leadership story gets most interesting and where you want to pay attention as an investor.

McDermott is a hired-gun CEO, not a founder, and his direct equity stake reflects that. He owns a meaningful amount of stock in absolute dollar terms, but it is not founder-level ownership and would not be the strongest skin-in-the-game story on its own. If this is where the analysis ended, you would have to call leadership ownership a moderate signal and move on.

What changes the picture is what happened in early 2026. As ServiceNow’s stock came under heavy pressure on growth deceleration concerns and “SaaSpocalypse” fears, several things happened in quick succession. McDermott bought roughly 3 million dollars of stock on the open market in late February. At the same time, he, the CFO Mastantuono, the Chief People and AI Enablement Officer Canney, and the Special Counsel Elmer all cancelled their previously planned 10b5-1 stock sale arrangements. McDermott has also publicly stated that more than 90 percent of ServiceNow employees are buyers of the company’s stock.

This pattern is what you actually want to see. A hired-gun CEO who has already made his fortune does not need to put 3 million dollars of personal capital into the open market unless he genuinely believes the stock is mispriced. Cancelling pre-arranged sale plans is not a costless action; it is a public commitment to hold through whatever the market is doing. The simultaneous behavior across the senior team suggests this is not one person’s gut call but a coordinated read on where the business is headed versus where the stock is priced.

For the bull thesis, this is the strongest single piece of leadership evidence. The team running the company is not behaving like a team that thinks the harness thesis is broken. They are behaving like a team that thinks the market is wrong and is willing to put their own money behind that view at exactly the moment most investors are running the other direction.

Summary of the leadership story

The leadership story for ServiceNow has three layers. The founder, Fred Luddy, built the right thing for the right reasons and handed it off cleanly while keeping the cultural and governance anchor in place. The succession of operator CEOs, Slootman to Donahoe to McDermott, has consistently attracted the best enterprise software talent in the world, and each handoff has been clean. The current CEO, McDermott, is the rare operator with both the track record and the mandate to take the company through its next defining phase, and he is putting his own capital behind that mandate at exactly the moment doubters are loudest.

For a thesis that depends on a fifteen-year compounding horizon, the leadership question is essentially whether you trust these people to allocate capital intelligently and execute through the agentic transition without losing the cultural and architectural discipline that built the company. On the evidence available, the answer is yes.

Next we will look at the financial profile and the valuation question; specifically whether the market is currently pricing the harness thesis or just the workflow business.

Valuation and Financials

The price action and the SaaSpocalypse

To understand where ServiceNow’s valuation sits today, you have to understand why the stock has done what it has done. Shares of ServiceNow are down 39 percent this year and off more than 55 percent from their 52 week high. Despite the company beating guidance every quarter, raising forward outlook, growing free cash flow at over 30 percent annually, and announcing a doubling of revenue targets to 30 billion by 2030, the stock has gone almost straight down. This is one of the most extreme dislocations between operating performance and stock price in large cap enterprise software in recent memory.

The reason is a market wide narrative that has come to be called the SaaSpocalypse. The argument runs like this. The last twenty years of SaaS valuations were built on per seat subscription pricing, where every additional employee was an additional license. Generative AI threatens that model at the root. If agents replace seats, ARPU collapses. If customers can build internal AI tools that replicate SaaS functionality at marginal cost, switching costs evaporate. The entire seat based subscription economy, in this view, is heading toward a structural reset. Investors have been pricing in that reset across the SaaS complex, and ServiceNow, as one of the largest and most expensive seat based SaaS businesses, has taken some of the heaviest punishment.

Here is the part of the SaaSpocalypse argument that is correct. SaaS businesses that do not see meaningful upside from AI, particularly the ones whose primary value proposition is being a static system of record or a forms based productivity tool, are genuinely going to get crushed. AI either eats their use case or commoditizes it. Many mid cap SaaS names trading at ten or fifteen times revenue with unclear AI angles deserve significant multiple compression. The narrative is not entirely wrong.

Where the narrative gets ServiceNow specifically wrong is that ServiceNow is not a static SaaS business. ServiceNow benefits more from AI, not less. The harness thesis explains why. As enterprises deploy more AI agents, they need more workflow infrastructure to govern, audit, and orchestrate those agents. Every additional agent in the enterprise is a new node that needs a harness underneath it. ServiceNow does not get smaller as agents proliferate; ServiceNow gets bigger, because the surface area of work that needs governance expands rather than contracts. The market has been pricing ServiceNow as if it were the same as a CRM tool that may get replaced by a Copilot agent. It is not the same thing. The dislocation between the narrative and the underlying business is exactly where the opportunity lives.

Where the multiples actually sit

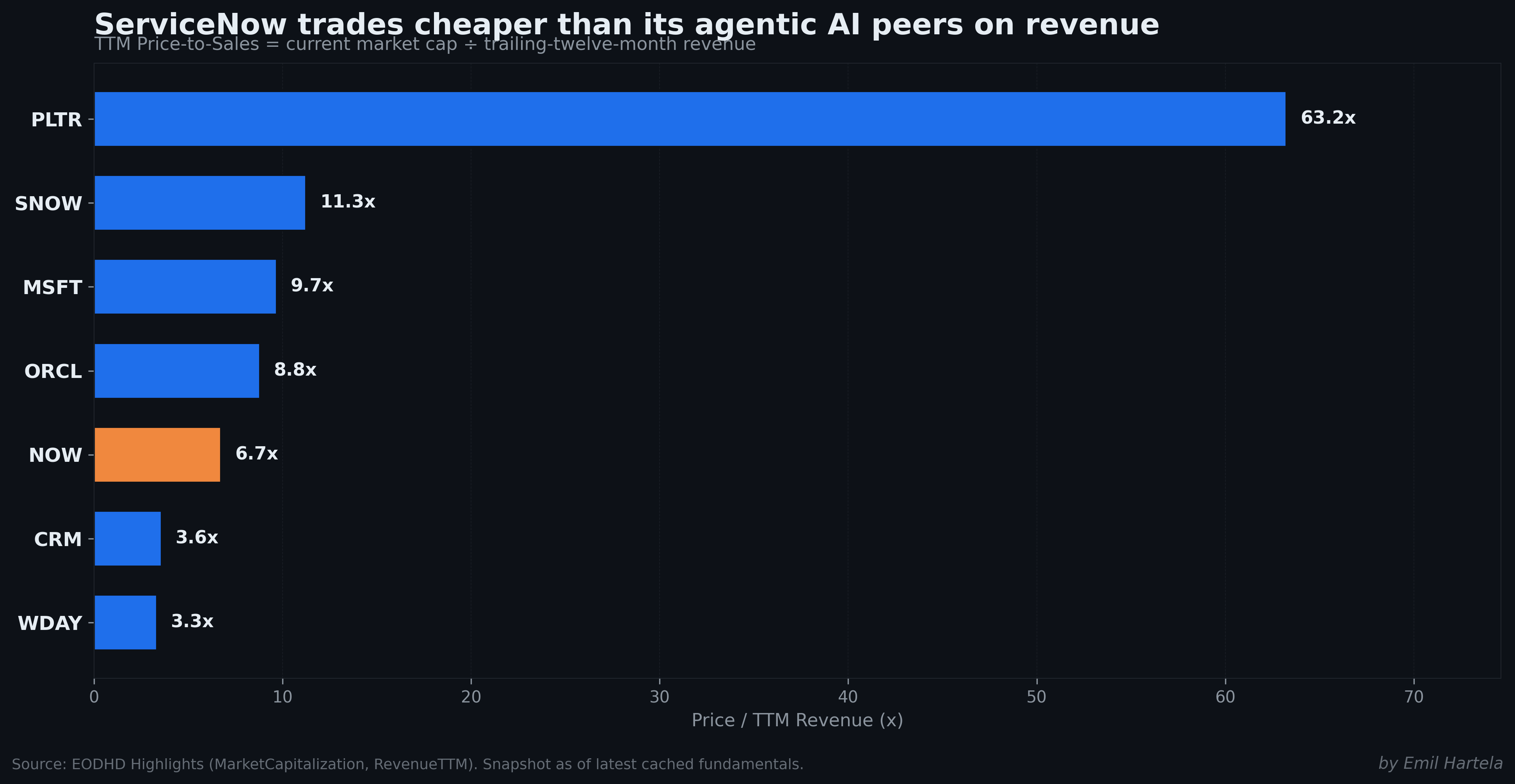

ServiceNow is not cheap on a price to sales basis. The current TTM P/S sits at 6,74 with EV/Revenue at 6,54. For context, the average S&P 500 company trades at roughly 2,8 times sales, and most established large cap software businesses sit somewhere between 5 and 10. So this is squarely in the premium software bucket but nowhere near the extreme end. Palantir, by comparison, trades at a market cap above 320 billion on roughly 4,5 billion in revenue, putting its P/S in the 70s. ServiceNow trades at less than one tenth of Palantir’s revenue multiple while generating roughly three times the revenue and growing at over 20 percent.

The earnings multiple is where the picture gets more nuanced and where investors need to be careful. On a GAAP basis, ServiceNow earned roughly 1,76 billion in net income on TTM revenue of 13,96 billion. Against a market cap of 94 billion, that is a trailing GAAP P/E of 54,3. That is rich by any standard. The forward non GAAP P/E, which strips out stock based compensation and acquisition related amortization, sits at 21,7. That is the figure most sell side analysts and management point to, and it is reasonable for the growth profile, but it papers over the real economic cost of SBC. The honest investor should hold both numbers in mind. The gap between 21,7 and 54,3 is essentially the SBC issue, which we will examine in detail in a moment.

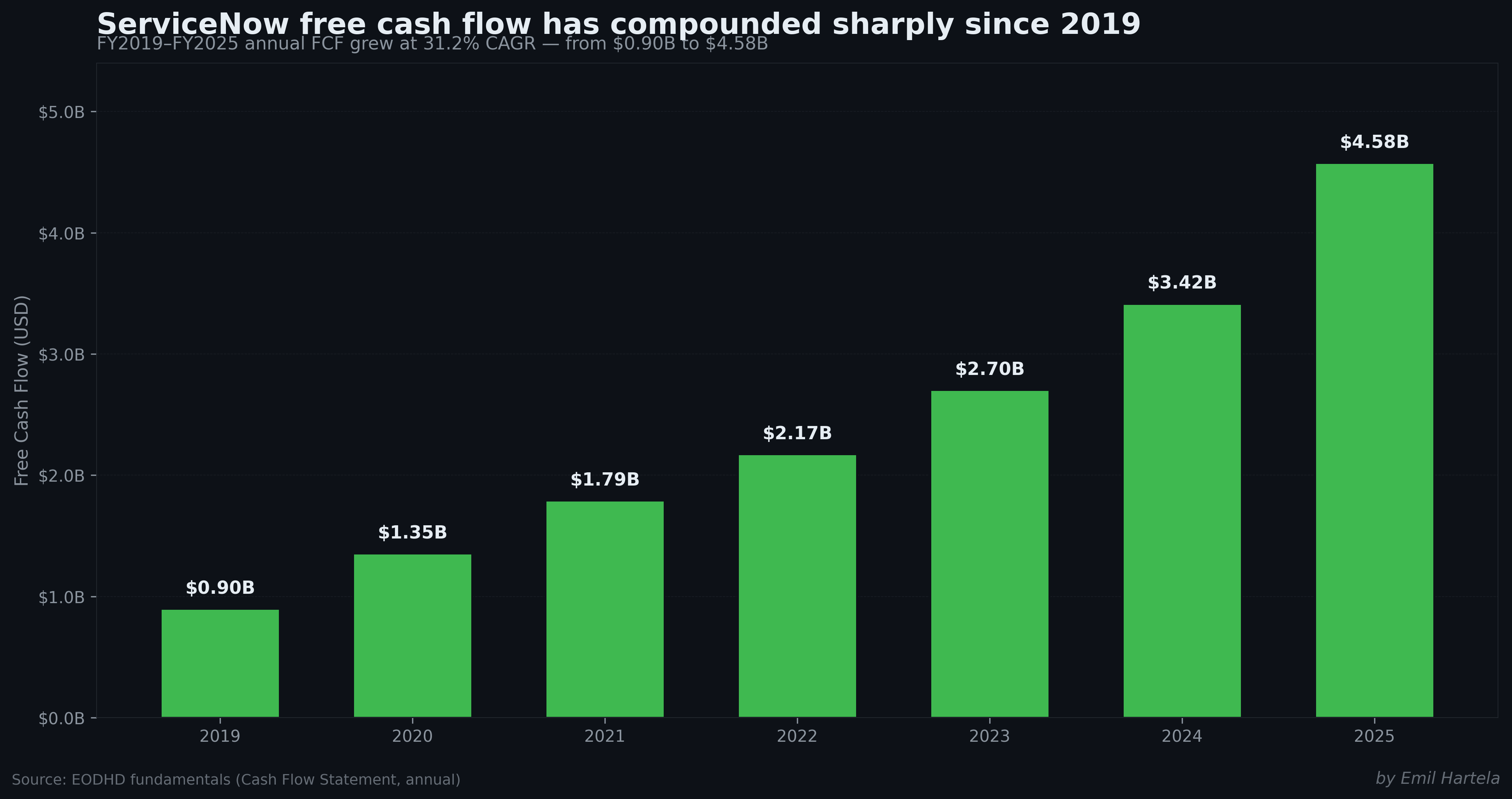

The cleanest valuation lens is on free cash flow. ServiceNow generated 4,58 billion in free cash flow in 2025, growing 34 percent year over year, and is now running at a TTM rate of 4,63 billion. Against a 94 billion market cap, that is a free cash flow yield of 4,9 percent. For a business growing free cash flow at over 30 percent annually, with a customer base that essentially does not churn and a net cash balance sheet, that yield is genuinely attractive. Most quality compounders trade at FCF yields closer to 3 percent. ServiceNow is being priced as if it were a much lower quality business than it actually is.

It is worth flagging that the GAAP operating margin of 13,7 percent is low for a software business of this scale and quality. Microsoft runs at over 45 percent. Oracle is north of 30 percent. Adobe is at 35 percent plus. The gap is almost entirely the SBC line. ServiceNow does not yet show up as a high margin business on a GAAP basis, which is part of why traditional value investors have stayed away. The bull case requires accepting that the cash flow is real and the SBC, while expensive, is a known and decreasing drag rather than a structural problem.

Growth has been remarkably consistent

The financial profile that makes the current dislocation so striking is the consistency of growth. Under McDermott, ServiceNow has grown subscription revenue from 3,5 billion in 2019 to 13,3 billion in 2025, with revenue compounding at roughly 24 percent annually over that stretch. The Q1 2026 print showed subscription revenue growing 22 percent year over year, accelerating from 19,5 percent the prior quarter. Guidance for full year 2026 sits at 15,74 to 15,78 billion, implying continued growth in the low 20s.

What anchors this growth is net revenue retention, which has consistently sat above 125 percent across multiple years. The reason is the encoded workflow stickiness discussed earlier; every workflow a customer builds increases switching costs, and every additional module adopted increases ARPU. The other side of that retention story is what the company calls its renewal rate, which has been disclosed at 98 percent for each of the past three years in the 10-K. Customers do not leave. They cannot leave. The business is not just growing; it is growing in the most defensible way possible, by deepening relationships with customers who have nowhere else to go.

The other forward looking growth anchor is the remaining performance obligation. Total RPO of 27,7 billion as of Q1 2026 grew 25 percent year over year, with current remaining performance obligations of 12,64 billion representing revenue expected in the next 12 months. Total RPO sitting at roughly twice annual revenue is a powerful lock on near term forecasts. Revenue is essentially already booked; the question is execution and renewal, not demand.

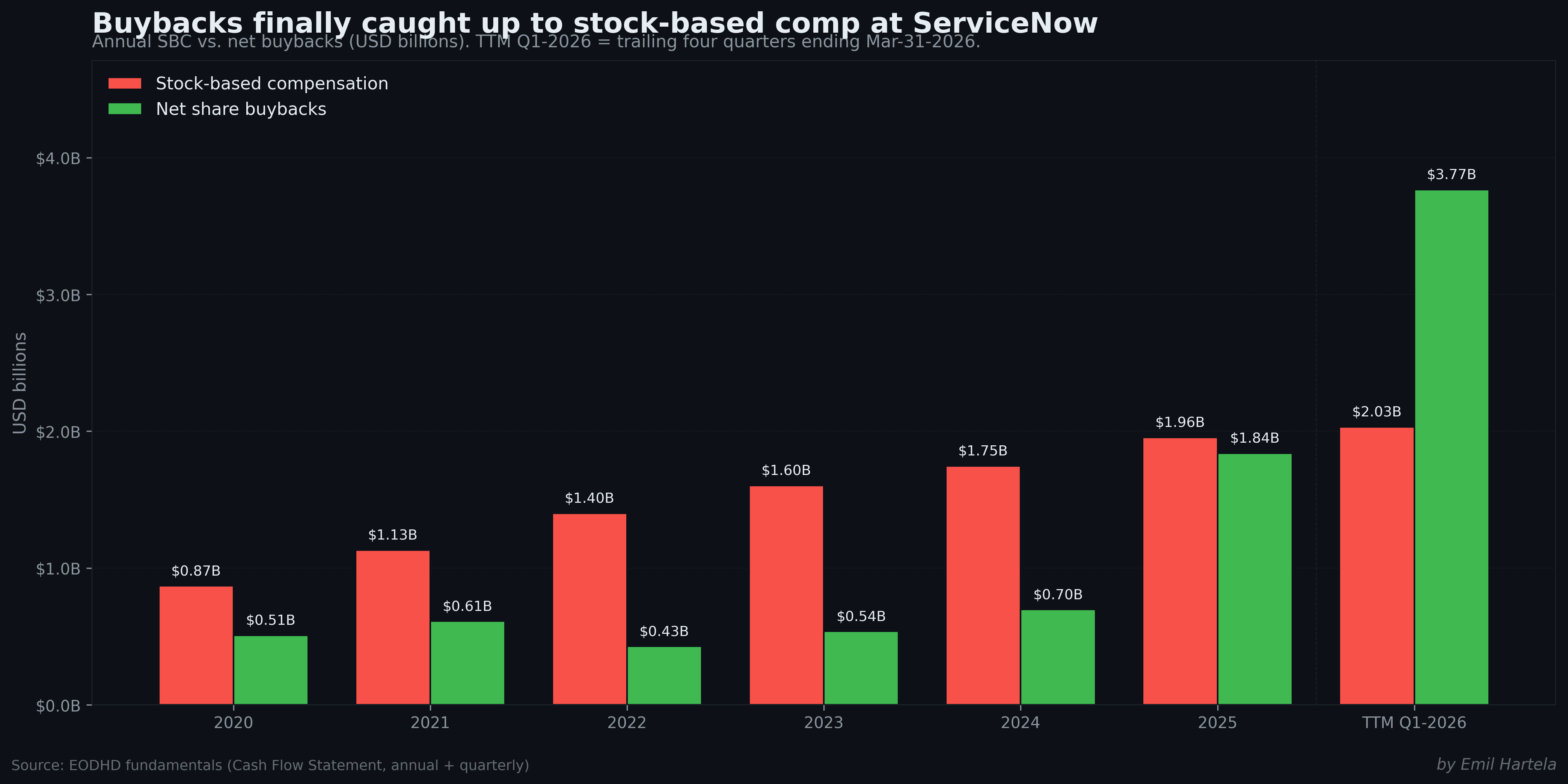

Stock based compensation and the buyback offset

This is where the bull case has to be honest. SBC ran at 1,96 billion in 2025 and is on a TTM run rate of about 2,03 billion as of Q1 2026. That is roughly 14,7 percent of revenue in 2025 and trending to about 14,5 percent on the latest TTM numbers. Five years ago, in 2020 and 2021, SBC was 19,2 percent of revenue. The 5 year average is 17,4 percent.

Two things matter in that history. First, the absolute level. SBC at 14 to 15 percent of revenue is high by mature large cap standards. Microsoft and Oracle run SBC at 4 to 6 percent. Salesforce runs at 9 to 11 percent. Snowflake runs above 40 percent. Workday runs at 16 to 19 percent. ServiceNow sits in the middle of the high growth enterprise software peer group. Second, the trend. SBC as a percentage of revenue has been declining steadily for four years, from 19,2 percent in 2020 to 14,7 percent in 2025. That trajectory matters more than the absolute level, because it tells you the dilution drag is structurally improving over time as the company scales, even though absolute dollar SBC continues to grow.

The offset is the share buyback program, which has accelerated dramatically. ServiceNow spent 0,70 billion on buybacks in 2024, then 1,84 billion in 2025. In Q1 2026 alone the company repurchased 2,23 billion of stock, more than the entire 2025 program. On a trailing twelve month basis, buybacks now total 3,77 billion against SBC of 2,03 billion. That is no longer managing dilution. That is meaningful net share count reduction. The Board has authorized an additional 5 billion under the share repurchase program in January 2026, bringing total available headroom to 9,5 billion, and the company announced a 2 billion accelerated share repurchase shortly after.

The honest framing is that the buyback program has moved through three phases. From 2020 to 2023, buybacks were modest and barely covered SBC. In 2024 and the first half of 2025, the company stepped into actively managing dilution. From late 2025 onward, the company has been aggressively buying back shares at a rate that materially exceeds SBC, which is the right behavior for a CEO who believes the stock is mispriced relative to the long term thesis. For a long horizon shareholder, this is the trajectory you want to see.

The balance sheet

ServiceNow runs a clean, conservative balance sheet. Cash and short term investments sit at 5,18 billion as of the most recent quarter. Long term debt sits at roughly 1,49 billion plus around 0,91 billion in capital lease obligations, but cash and short term investments comfortably exceed total debt, leaving the company in a net cash position of roughly 0,5 billion. There is no leverage risk, no refinancing risk, and no near term liquidity concern. For a business of this size and growth profile, the balance sheet is a strength rather than a constraint.

How they think about M&A

ServiceNow has become genuinely acquisitive over the past few years, and the pattern is worth understanding because acquisitive software companies have a habit of destroying value when they get the philosophy wrong. ServiceNow has so far gotten it mostly right, and the M&A history tells you something about how management thinks.

The pattern is consistent. ServiceNow does not buy companies for their revenue. They buy companies for capabilities that extend the harness. The acquisition logic is almost always about plugging a specific gap in the platform that would otherwise take two or three years to build internally. The acquired company’s revenue is essentially incidental. Some recent examples make the pattern clear.

Moveworks, acquired in late 2025 for roughly 2,85 billion, brought a conversational AI front-end and an enterprise search capability that ServiceNow now positions as the AI-native employee experience layer. The strategic logic was that as AI agents proliferate, the conversational entry point to the enterprise becomes valuable real estate, and Moveworks had built a real product there with real customers.

Armis, acquired in early 2026 for roughly 7,75 billion, added cybersecurity asset visibility, particularly for IoT and operational technology environments. This extends the SecOps module and the CMDB into a part of the enterprise that ServiceNow’s traditional discovery tools could not reach. Armis is also creating most of the near-term margin headwind being discussed on earnings calls; roughly 75 basis points of operating margin and 200 basis points of FCF margin in 2026, normalizing by 2027.

Veza, acquired in 2025, brought identity and access governance capabilities. The strategic logic ties directly into the AI Control Tower story; if you are going to govern AI agents at the enterprise level, you need to know who has permission to do what, and Veza’s product gave ServiceNow that capability natively.

Element AI earlier in the cycle, plus a series of smaller AI tooling acquisitions, brought AI engineering talent and specific model capabilities that became the foundation of Now Assist.

The unifying pattern across all of these is the same. ServiceNow is buying the capabilities required to build the agentic harness, not buying revenue or scale. McDermott has been publicly explicit that this is the discipline; he said on a recent earnings call that ServiceNow walked away from acquisitions when prices got irrational and that the company’s priority is product completeness, not topline growth through deals.

The math also looks reasonable. ServiceNow has spent roughly 10 billion on acquisitions over the past two years, against a balance sheet with 5 billion in cash and growing free cash flow generation. The pace is meaningful but not reckless, and the company has not had to issue debt or stock to fund any of it.

There are two genuine risks in the M&A story worth flagging. First, the integration burden is real. Each acquisition takes 12 to 24 months to fully integrate into the platform, and during that period the acquired teams need attention, the products need replatforming onto the Now Platform, and customer overlap creates account management complexity. With four meaningful acquisitions in two years, the integration backlog is heavier than it has been at any prior point in ServiceNow’s history. Second, the larger ServiceNow gets, the more tempting it becomes to use M&A to paper over slowing organic growth. Other large enterprise software companies have walked into this trap (the historical comparisons here are not flattering; SAP and Oracle both went through phases where M&A was a substitute for organic innovation rather than a complement to it). ServiceNow has not shown this pattern yet, but the risk increases as the company scales.

For now the discipline looks intact. The acquisitions plug specific capability gaps, the prices have been reasonable, the strategic rationale is consistent, and the integration is being managed openly with clear margin guidance to investors. This is the right pattern from a long-horizon shareholder perspective.

Dividends

ServiceNow does not pay a dividend and has not signaled any intent to start. Capital return runs entirely through buybacks. For a business still growing in the low 20s with significant reinvestment opportunities and an active acquisition pipeline, this is the correct choice. Dividend yield investors should look elsewhere; this is a compounding capital appreciation story, not an income story.

Gross margins and the trajectory

GAAP gross margin has held in a tight range of roughly 77 to 79 percent across the past five years. Non GAAP gross margin sits at roughly 82 to 83 percent. Subscription gross margin specifically runs at 81 to 83 percent on a GAAP basis and 85 to 86 percent on a non GAAP basis. These are best in class enterprise software gross margins.

The recent trend has been a slight compression on GAAP gross margin, primarily driven by acquisition related amortization (Armis being the most recent contributor) and to a lesser extent by AI infrastructure costs as Now Assist scales. Management has guided to 81,5 percent subscription gross margin for the full year 2026, with the Armis acquisition creating roughly 25 basis points of headwind. None of this materially changes the underlying picture. ServiceNow is an extraordinarily high margin business and will remain one. The gross margin profile is not a concern.

Operating leverage and R&D

This is one of the more underappreciated parts of the financial profile. GAAP operating margin has expanded from 4,4 percent in 2020 to 13,7 percent in 2025, more than a tripling over five years. Non GAAP operating margin has moved from roughly 24 percent in 2020 to roughly 30 percent in 2024 and 31,5 percent guided for 2026. The business is producing genuine operating leverage even while R&D investment has been climbing in absolute terms.

R&D spending was 2,96 billion in 2025, up 16 percent year over year. As a percentage of revenue, R&D has been remarkably stable in a 22 to 24 percent range across the past six years, which is appropriate for a platform business that is actively building out an AI layer. ServiceNow is not coasting; it is reinvesting heavily while still expanding margins, which is the textbook profile of a quality compounding software business.

The biggest operating leverage has come from sales and marketing. S&M spending fell from 41 percent of revenue in 2020 to 33 percent of revenue in 2025. That is the classic SaaS maturity curve playing out exactly as it should; as the install base grows and renewals carry more of the revenue load, the cost of acquiring each incremental dollar of revenue declines. G&A has shown similar leverage, falling from 10 percent of revenue in 2020 to 8,5 percent in 2025. These two lines together explain most of the GAAP operating margin expansion over the past five years and they have substantial room to keep compressing.

The 2030 target and what it implies

In May 2026, at the company’s Financial Analyst Day, ServiceNow laid out a target of 30 billion in subscription revenue by 2030. McDermott called this the bear case during the presentation, with a 32 billion upside scenario presented as well. The company is currently doing approximately 16 billion in subscription revenue this year and has 27,7 billion in remaining performance obligations, approximately double its annual revenue.

Doubling subscription revenue from 16 billion to 30 billion over four years requires a roughly 17 percent compound annual growth rate. Given that the company has been growing subscription revenue in the low 20s recently, the 30 billion target is genuinely conservative on current trajectory. The CFO noted that in 2021, the company set a five year target of 15 billion and is on track to beat it by half a billion dollars, organically. Management has a track record of setting ambitious targets and then beating them. The 30 billion number is more likely a floor than a ceiling.

The other important number from Financial Analyst Day was that AI products are expected to represent more than 30 percent of annual contract value by 2030, up from low single digits today. If that materializes, it answers the SaaSpocalypse question directly. ServiceNow would have demonstrated that AI is additive ARPU on top of existing seat based revenue, not a replacement for it.

Running some simple multiples

This is where the relative value gets interesting. If you assume ServiceNow hits 30 billion in subscription revenue by 2030 (their bear case), and add a reasonable 1,5 to 2 billion of professional services revenue on top, total revenue lands around 32 billion. Apply the historical FCF margin of roughly 32 percent and you get free cash flow of roughly 10 billion in 2030.

At today’s 94 billion market cap, that implies a forward 2030 FCF multiple of roughly 9,4. For a business that will still be growing over 15 percent annually at that point with the kind of customer stickiness ServiceNow has, 9,4 times FCF four years out is not just cheap; it is genuinely undemanding. A reasonable terminal multiple for a business of that quality and growth profile is somewhere between 25 and 35 times free cash flow. At 30 times FCF on 10 billion of FCF, the implied 2030 market cap is 300 billion. From today’s 94 billion, that is a triple over four years before considering buybacks.

Now consider the upside scenarios. If the harness thesis is correct and the market eventually starts pricing ServiceNow not as a workflow company but as the operational substrate of the agentic enterprise, multiples could rerate dramatically. Investors today are paying 70 plus times revenue for Palantir, which has a less defensible business at much smaller scale. There is no fundamental reason ServiceNow could not see a multiple rerate toward 12 to 15 times revenue if and when the agentic transition is recognized as a tailwind rather than a threat. At 15 times revenue on 32 billion of 2030 revenue, the implied market cap is closer to 480 billion. That would be a roughly five times return over four years on today’s price.

The honest framing of the bull math is this. The downside case is that ServiceNow continues to compound revenue and FCF at 15 to 20 percent for the next four years and the multiple stays where it is, which still produces a roughly 70 to 100 percent return through earnings growth alone. The base case is that the multiple modestly rerates as the SaaSpocalypse narrative breaks and the company delivers on the 30 billion target, producing a 2 to 3x return. The bull case is that the harness thesis becomes consensus, multiples rerate aggressively, and the stock compounds at 25 to 30 percent annually for the next four to five years.

This is the kind of asymmetric setup that does not come along often in large cap enterprise software. The market is pricing the bear case. The business is delivering the base case. And the long term setup is the bull case. That is the entire valuation argument in three sentences.

Next we will turn to the risks and the deeper due diligence questions that could break this thesis.

Risks and Deeper Due Diligence

No thesis is complete without honestly enumerating what could break it. The harness framing is compelling, the financials are strong, and the leadership is among the best in enterprise software, but a long horizon investment thesis still needs to survive scrutiny on what could go wrong. This section walks through the risks I take most seriously, ordered roughly by how much they actually keep me up at night.

Stock based compensation as a structural drag

The first risk is the one already covered in the financials section but worth flagging again as a risk rather than just a feature of the financial profile. SBC at 14 to 15 percent of revenue is the single largest gap between the GAAP and non GAAP picture, and it is the reason traditional value oriented investors have stayed away from the name. If the trend of declining SBC reverses, or if the buyback program slows for any reason, dilution becomes a meaningful drag on per share returns. Management has signaled commitment to the buyback ramp, but capital allocation decisions are reversible. This is not a thesis breaker but it is a permanent bear talking point that will keep some investors out of the stock.

Key person risk and the McDermott question

Bill McDermott was 58 when he took the CEO role in late 2019, which makes him roughly 64 or 65 today. That is not old by CEO standards (Buffett is in his 90s, Larry Ellison is in his 80s, Dimon is 69) but it is worth flagging because McDermott is genuinely critical to the next phase of ServiceNow’s story in a way that is rare. He was hired specifically to take the company through the agentic transition and to scale toward 30 billion in revenue by 2030. If something happens to him or if he decides to step back before that journey is complete, the stock would react sharply.

There is a specific health note worth being honest about. McDermott lost his left eye in a household accident in 2015, when he slipped on stairs while carrying a glass of water and a shard of glass injured his eye. He underwent a long surgical recovery and returned to running SAP shortly afterward. There is no public indication of any current health concern. But anyone evaluating key person risk on a CEO of his age and centrality to the thesis should be aware of his medical history.

The mitigant is the deep bench. ServiceNow’s track record of CEO succession (Slootman to Donahoe to McDermott) suggests the board and leadership pipeline can handle a transition. Gina Mastantuono as CFO and President is a credible internal succession candidate. Fred Luddy is still Chairman. The company has handled three CEO transitions cleanly, and the cultural anchor Luddy provides is itself succession insurance. Still, in the near term, McDermott is the face of the company and the architect of the current strategy. His departure for any reason would be a meaningful negative event.

Reflexivity in the equity funding model

This one is more subtle and worth taking seriously. ServiceNow’s compensation model depends meaningfully on equity to attract and retain talent, like every other large enterprise software company. When the stock is rising, equity grants are a powerful retention and recruiting tool because employees see their unvested stock appreciating. When the stock is falling, the same equity grants become less effective because employees worry about declining value, and the company has to issue more shares at lower prices to deliver the same dollar amount of compensation.

This creates a reflexive loop. If the stock continues to fall, SBC as a percentage of revenue could rise rather than continue its downward trend, because the company would need to issue more shares to cover the same compensation expense. That would in turn push GAAP earnings further down, deepen the SaaSpocalypse narrative around the name, and push the stock lower. The current dynamic of accelerating buybacks against declining SBC could reverse if equity sentiment around the name does not improve.

The reverse is also true. If the stock starts to recover, the equity compensation model becomes self reinforcing in the opposite direction. Fewer shares issued for the same dollar expense, lower SBC as a percentage of revenue, less buyback offset needed, and the GAAP picture improves. This is part of why management has been so aggressive about defending the stock publicly and buying back shares; they are trying to break the negative reflexive loop before it embeds.

For a long horizon investor, this risk is real but not unique to ServiceNow. Every high growth software company faces the same dynamic. The question is whether ServiceNow’s underlying business is strong enough to break out of the negative loop on its own, which I believe it is, but it is not guaranteed.

AI platform hostility and squeezed input costs

This is one of the more interesting forward looking risks and one that is not yet being priced. ServiceNow’s Now Assist and Otto products are increasingly built on top of frontier AI models from external providers. The Knowledge 2026 conference made clear that ServiceNow is integrating Claude from Anthropic and OpenAI’s models alongside its own NowLLM. This works beautifully today because the AI providers want enterprise distribution and ServiceNow gives it to them.

The risk is that this dynamic shifts. If OpenAI, Anthropic, or Microsoft decide that the enterprise workflow layer is strategically valuable enough to compete in directly, they could squeeze ServiceNow’s input costs by raising API prices, restricting access to leading models, or going after ServiceNow’s customers directly with their own competing offerings. Microsoft is the most obvious risk because they own both a frontier model partnership with OpenAI and a competing workflow stack in Power Platform. OpenAI has been increasingly direct about wanting to own the enterprise relationship, not just be a model provider. Anthropic has a deep partnership with ServiceNow today, but partnerships shift.

The mitigant is that the harness layer, the actual workflow execution and governance infrastructure, is much harder to replicate than the AI model layer. ServiceNow can swap one frontier model for another with limited customer impact. The customer cares about workflow orchestration and audit, not which underlying model summarizes a ticket. ServiceNow’s MCP server architecture announced at Knowledge 2026 is essentially a hedge against this exact risk; it makes ServiceNow model agnostic so that no single AI provider can hold it hostage. Still, this is a real watch item over the next three to five years.

Broader AI narrative cooldown

Worth taking seriously and probably the risk I think about most actively. The AI infrastructure trade has been one of the strongest equity narratives of the past three years. NVIDIA has carried the broader market. TSMC, Broadcom, and the semiconductor ecosystem have been priced for continued exponential growth. Recent signals suggest that growth is slowing. TSMC has been moderating its near term capex outlook. Some semiconductor valuations are at levels that historically have only been sustainable in extreme bubble conditions.

If the AI narrative cools off broadly, the market historically does not discriminate well in the early phases of the rotation. In 2001, after the dotcom peak, the market sold everything internet related regardless of the underlying business quality. Cisco, Sun, and Oracle all dropped 70 to 90 percent despite being real businesses. ServiceNow could absolutely take collateral damage in that kind of environment, even though the harness thesis is more durable than most AI tagged businesses. A 12 to 18 month period of multiple compression across the entire AI complex would push ServiceNow lower regardless of fundamentals.

The way to think about this is not whether to own ServiceNow, but how much to own. If the AI narrative breaks broadly, you want enough conviction in the underlying business to add to the position rather than cut it. ServiceNow is one of the few names in this space where I am confident the operating performance will eventually pull the stock up regardless of what the broader narrative does, but the path could be uncomfortable.

Federal government exposure and DOGE

ServiceNow has a meaningful federal business that has been a quiet contributor to growth for several years. That exposure has become a near term risk. The Department of Government Efficiency has been aggressively pruning federal software contracts in 2026, and federal agencies have been scrutinizing legacy SaaS spend in favor of cheaper, often AI native, alternatives. ServiceNow’s federal business growth has slowed measurably as a result, and analyst commentary in early 2026 has flagged this as one of the primary near term overhangs on the stock. Stifel cut its price target from 180 to 135 in April 2026 specifically citing weaker federal spending.

The mitigant is that ServiceNow’s federal business is still growing in absolute terms (net new ACV in federal grew over 30 percent year over year in Q3 2025) and the federal use cases ServiceNow serves are deeply embedded in agency operations. DOGE can slow procurement cycles and force renegotiation but is unlikely to actually rip out installed deployments. The bigger question is whether the federal contraction is a one to two year timing issue or a structural shift in how federal IT spending allocates. I lean toward the former, but it is worth watching closely.

Middle East deal slippage and geopolitical drag

Q1 2026 results flagged 75 basis points of subscription revenue growth headwind from delayed closings of large on premise deals in the Middle East due to the regional conflict. Management has guided cautiously for the rest of 2026 to reflect continued geopolitical uncertainty. This is a pure timing issue, not a structural one; the deals are not lost, just delayed. But timing matters for quarterly prints, and the market has been punishing any near term miss against the SaaSpocalypse backdrop. A second or third quarter of similar slippage would extend the drawdown even though the long term thesis would be unaffected.

US fragmentation from global powers

A risk that gets less attention than it should is the broader trend of geopolitical fragmentation between the United States and other major economies. ServiceNow is an American enterprise software company that runs critical workflow infrastructure for global customers. If trade tensions, data sovereignty requirements, or outright sanctions force European, Asian, or Middle Eastern customers to move toward domestic alternatives, ServiceNow’s international revenue base is exposed.

This is not a near term risk. But it is the kind of slow moving structural pressure that could compress international growth over a five to ten year horizon. The mitigant is that ServiceNow’s competitors at the harness layer are all also American (Microsoft, Salesforce, Workday), so a fragmentation scenario is more about reduced TAM than market share loss. There is no meaningful European or Chinese competitor at the harness layer today, which is both a strength (no immediate displacement risk) and a weakness (a fragmenting world cannot easily be served by any of the current incumbents).

M&A and buyout risk

This one is technically not a downside risk for shareholders, but worth flagging. At a 94 billion market cap, ServiceNow is large enough that very few acquirers could absorb it. Microsoft, Oracle, Alphabet, Amazon, Meta, and possibly SAP are essentially the only realistic candidates. Regulatory approval for any of these acquirers buying ServiceNow would be extremely difficult given antitrust scrutiny on big tech. The probability of a takeover at this size is very low.

If it did happen, it would likely be at a meaningful premium to current prices, which would reward shareholders but would cap the long term upside that the harness thesis implies. From a long horizon perspective, the better outcome is that ServiceNow remains independent and compounds value over the next decade. A buyout would be a near term win and a long term opportunity loss.

Other risks worth flagging

A few smaller items worth knowing about. The CJ Desai departure as President in 2024 raised some concerns about product strategy continuity, though the bench has handled it well. The Armis and Moveworks acquisitions are creating near term margin headwinds (roughly 75 basis points of operating margin and 200 basis points of FCF margin in 2026) that will normalize by 2027 but are creating optical noise in the meantime. Customer concentration is not a meaningful risk; the largest customer is well below 5 percent of revenue. Currency exposure is real because international is roughly 35 percent of revenue, and the dollar has been volatile, but management hedges actively and discloses constant currency growth rates that are typically within 100 to 200 basis points of reported.

What I deliberately did not include in this risk section is anything around accounting or governance concerns, because despite the elevated multiple and high SBC, there are no credible short reports against the company, no material accounting questions raised by major activist short sellers, and no governance red flags in the 10-K. ServiceNow has been a public company for over thirteen years and has consistently passed audit and disclosure scrutiny. That is not nothing.

What would actually make me sell

This is the question every honest thesis section should answer. I would reduce or exit my ServiceNow position if any of the following happened.

First, if the renewal rate disclosed in the 10-K dropped meaningfully below 98 percent for two consecutive years, the harness thesis is broken because the encoded workflow stickiness is not as strong as I believe.

Second, if McDermott departed for non-routine reasons and the succession was not handled cleanly within six months, I would reassess whether the company can still execute the agentic transition on the timeline the bull case requires.

Third, if Microsoft or a competitor managed to displace a Tier 1 financial services or government customer from ServiceNow in a public reference deal, the moat assumption is wrong.

Fourth, if SBC as a percentage of revenue reversed and started rising sustainably, indicating the company cannot retain talent without paying ever higher equity costs.

Fifth, if a major short report from a credible activist surfaces with substantive accounting or governance concerns that survive initial scrutiny.

None of these are happening today. All of them are worth watching.

Net risk assessment

The honest summary is that the risks to the ServiceNow thesis are mostly timing and sentiment risks rather than fundamental business risks. The harness thesis could be wrong but the evidence is strong. The competition is real but no one is actually building a competing harness. The financials could disappoint in any given quarter but the multi year trajectory is one of the most consistent in software. The biggest actual danger is that the market continues to misread the agentic transition as a threat and the stock stays rangebound for longer than a typical investor’s patience.

For the kind of investor who can hold through multi quarter narrative dislocations, the risk reward setup is unusually attractive. For investors who need quarterly performance to validate every position, this is a difficult name to own right now and probably will remain so until either the SaaSpocalypse narrative breaks definitively or the agentic transition shows up clearly in financial results.

Next we will close with a summary of the thesis and a conclusion on positioning.

Summary

The harness thesis is the cleanest articulation of why ServiceNow should be one of the most important companies in the world over the next decade. Every large enterprise will need a substrate that holds together the operational logic of the business as humans, integrations, and AI agents all execute work in parallel. Twenty two years of encoded customer workflows, deeply governed integrations, and the strongest cross functional module footprint in enterprise software make ServiceNow the structurally favored candidate to own that layer. The recent Knowledge 2026 announcements around AI Control Tower, Action Fabric, and the model context protocol server are not pivot moves; they are the natural extension of what ServiceNow has been building since 2003.

The leadership story is among the best in software. Fred Luddy built the right thing for the right reasons and handed it off cleanly. Bill McDermott is one of the few operators on earth qualified to take the company through the agentic transition, and his recent open market stock purchases and the cancellation of executive sale plans signal he believes the stock is mispriced relative to where the business is heading. The competitive landscape is real but no one else is actually building a harness; Microsoft, Salesforce, and Workday are each building something else with workflow as a feature.

Worth highlighting one independent endorsement that lands with weight. At Knowledge 2026 in early May, Jensen Huang appeared on stage alongside McDermott and made the explicit case that the agentic transition is one of the largest software opportunities in history and that it runs through ServiceNow. Huang is not just a partner endorsing a partner; Nvidia itself runs its employee workflows on ServiceNow, and Huang publicly described a future where physical robots, factory automation, and the entire industrial economy are governed through ServiceNow. There are very few people on earth whose track record on identifying technology shifts is as strong as Huang’s. When he tells you publicly that an enterprise software company is going to be central to the next phase of AI, that is a signal worth weighting heavily. It is not a substitute for doing your own work, but it is one of the strongest endorsements an outside operator could give.

A few honest caveats worth holding in mind. The stock is not dirt cheap if you look at it on traditional multiples alone. A trailing GAAP P/E of 54 and a price to sales ratio of nearly 7 are still premium multiples by most measures. The SaaSpocalypse narrative could continue to drag the stock lower in the near term. The federal headwinds and Middle East deal slippage are real and could extend beyond a quarter or two. The broader AI complex could see a sharp narrative reset that pulls everything related down with it. ServiceNow could fall further from here, and any honest investor in the name needs to be prepared for that possibility.

But step back from the noise and consider what is actually being offered. There is essentially not a single large company on earth that would not benefit from what ServiceNow is building. Every Fortune 500 needs better workflow infrastructure. Every enterprise deploying AI agents needs a governance layer. Every aging organization facing knowledge transfer challenges needs a way to encode operational logic. Every company facing margin pressure needs a substrate that can let humans and agents execute work side by side. The total addressable market is essentially the operating model of the global enterprise economy, and the company best positioned to capture it is trading at a free cash flow yield approaching 5 percent with a balance sheet in net cash and a CEO actively buying his own stock.

If the harness thesis is right, ServiceNow is one of the most underpriced large cap software businesses in the market today. If the harness thesis is wrong, you still own a 30 percent FCF growth business at a reasonable multiple with best in class retention and a strong balance sheet. The asymmetry is what makes this an unusually attractive setup for a long horizon investor.

That is the full thesis as I see it today.