SEO Was One Surface. GEO Is Six.

The shift to AI-driven discovery doesn't kill SimilarWeb. It multiplies their market.

I have been using alternative data for investing for several years. Tried a lot of providers across a lot of data types. One provider has consistently managed to work its way into my actual workflow: SimilarWeb. I have used both SimilarWeb directly and several services that buy and repackage their data. When it comes to predicting revenue trends and nowcasting companies from web traffic and app signals; it is genuinely one of the better tools I have come across.

A few months back I realised SimilarWeb is a listed company. Further; it has come down significantly from its peak; the kind of chart that makes a stock look distressed at first glance. But distressed and broken are two different things. I think there might be a real opportunity here; so I decided to write a proper deep dive on the trade idea.

Disclaimer

Nothing in this piece constitutes financial advice. This is my personal research and opinion for informational purposes only. Always do your own due diligence before making any investment decision.

What Does SimilarWeb Do?

SimilarWeb is a digital intelligence platform. At its core it measures what is happening across the internet; who is visiting which websites; where they come from; how long they stay; and what they do next. It does this across hundreds of millions of digital properties globally and packages that data into a platform that different types of customers use for different purposes.

The customer base is broad but falls into a few natural clusters.

Enterprise marketing and strategy teams use SimilarWeb to benchmark their own digital performance against competitors; understand which channels are driving growth in their category; and identify market share shifts before they show up in reported financials. A consumer goods company wanting to know whether a competitor is gaining ground in organic search or paid acquisition before the next earnings call is a typical use case.

Investors and financial analysts use it as alternative data for nowcasting revenue; predicting earnings surprises; and tracking consumer demand trends in real time. Web traffic and app engagement data has a meaningful lead time advantage over reported financials; which is why it has become a standard tool in quantitative and fundamental research workflows.Sales intelligence teams use it to identify prospects; score leads by digital footprint; and prioritise outreach based on signals like traffic growth; tech stack changes; and hiring patterns.

Retail and e-commerce teams use it for category management; tracking Amazon market share; and understanding where online shoppers are going across the purchase funnel.

What every customer is fundamentally buying is the same thing: visibility into the digital behaviour of markets; competitors; and consumers that they cannot observe directly. SimilarWeb is the measurement layer sitting underneath all of that; and the data asset that makes it possible is a proprietary blend of ISP-level data partnerships; browser panel data; direct measurement relationships; and first-party analytics integrations that has taken over a decade and hundreds of millions of dollars to assemble.

The Downfall of SimilarWeb

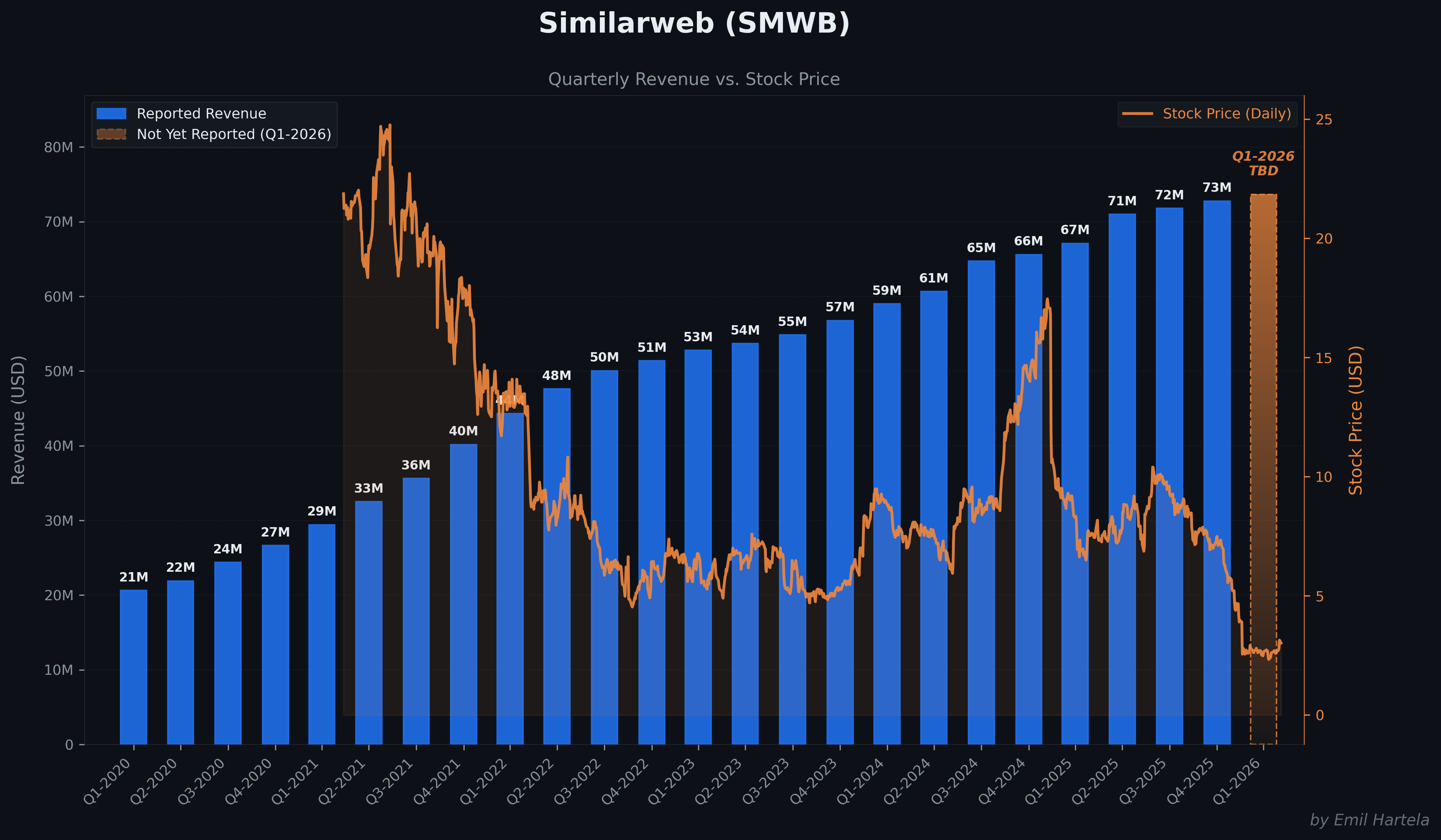

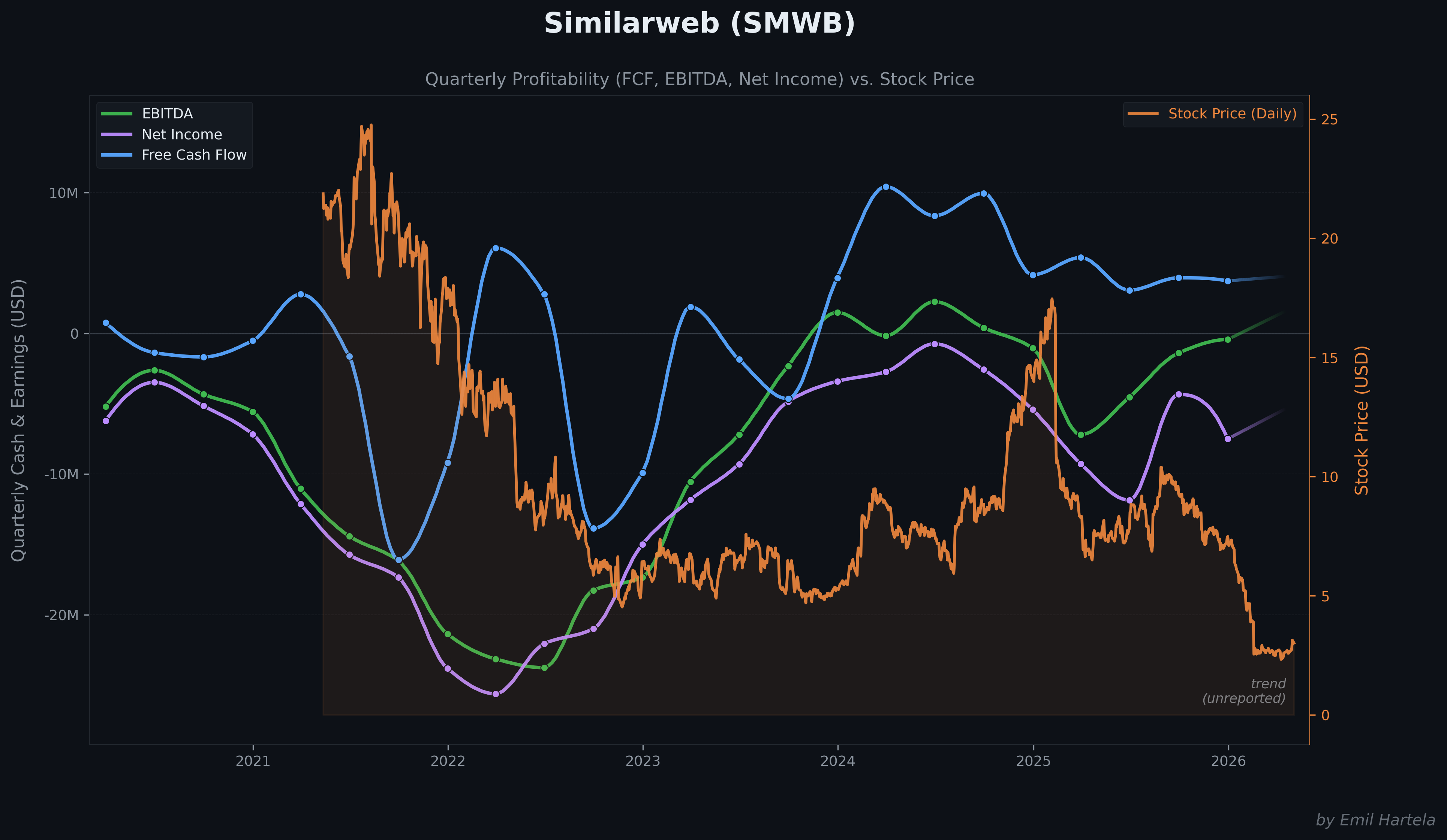

SimilarWeb listed on the NYSE in May 2021 at $22 per share; valuing the company at roughly $1.65 billion at IPO. At its peak shortly after listing the stock touched nearly $25. Today it trades around $2.50; a decline of approximately 90% from its highs.

The collapse in valuation is a combination of several compounding factors.

The first is simply post-IPO multiple compression. SimilarWeb listed at the peak of the SaaS valuation cycle; when growth software companies routinely traded at 15 to 20x revenue. As interest rates rose through 2022 and 2023 that multiple framework collapsed across the entire sector. SimilarWeb went from being priced as a high-growth data platform to being repriced as a mid-growth SaaS business; and the valuation followed.

The second is the retention problem. SimilarWeb’s net revenue retention has lingered around 98%; below the 100% threshold that signals a healthy expanding customer base. For a SaaS business this is a meaningful red flag; it means existing customers are not growing their spend fast enough to offset those who downgrade or leave. New customer acquisition is carrying the entire growth burden; which is an expensive and fragile way to grow.

The third is competitive pressure. SemRush has grown aggressively into adjacent territory; building a broader platform that competes directly for marketing intelligence budgets. With better brand recognition among practitioners and stronger NRR; SemRush has attracted a higher valuation multiple and more investor confidence; making the comparison unflattering for SimilarWeb.

Finally there is the AI threat narrative. The market has begun questioning whether AI-driven search disruption could erode the web traffic signals that SimilarWeb’s platform is built on; and whether newer AI-native tools could commoditise the intelligence layer SimilarWeb currently owns. That uncertainty has added a structural discount on top of the operational headwinds.

The result is a stock that looks genuinely distressed; trading at under 1x trailing revenue with a market cap of roughly $230 million against a business doing $283 million in annual revenue.

Turnaround Pitch

For SimilarWeb to meaningfully recover and reclaim a fraction of its lost market cap; several things have to go right simultaneously.

Retention has to improve. The core SaaS business needs to stop bleeding at the margins; meaning existing customers need to expand their spend rather than flatline or downgrade. Without that the growth engine is entirely dependent on new logo acquisition; which is expensive and increasingly competitive.

They need to nail the AI narrative. Not just in investor presentations; but in actual product and revenue. The market needs to see the AI data licensing business convert from lumpy one-time deals into recurring contracts; and the GEO measurement suite needs to demonstrate real enterprise adoption. The story is compelling. The numbers need to follow.

And they need to be differentiated enough from competitors that they have room to breathe. If SimilarWeb is perceived as a slightly worse version of what Adobe now owns in SemRush; the stock stays where it is. If the market comes to understand that SimilarWeb is measuring something fundamentally different and more comprehensive; the repricing can be significant.

In the sections that follow I will walk through each of these dimensions in detail; what the company is actually doing; what the data shows; and whether this is a knife worth catching.

The Potential Turnaround Drivers

I think SimilarWeb is in the right position to make a meaningful comeback. Let me walk through why.

Artificial Intelligence: Threat or Tailwind?

The market has largely framed AI as a threat to SimilarWeb. I think that framing is wrong; or at least incomplete.

SimilarWeb has spent over a decade scraping and measuring the web at scale. The data asset they have built is genuinely hard to replicate; and the proof of that is in the margins. An 80% gross margin business is not something you build without a defensible underlying asset. That data is now becoming more valuable; not less; as foundational model companies need high-quality; proprietary; continuously updated web behavioural data to train and evaluate their models. SimilarWeb is already selling into this market. The financial scale is still modest but the strategic significance is not.

The more interesting AI angle however is what is happening on the demand side among SimilarWeb’s existing customers. Every marketing team; every brand; every e-commerce operator that previously asked “how do we rank on Google” is now asking a set of entirely new questions. Are LLMs recommending our products to users? Why does Grok recommend us while Claude does not? Are our competitors ahead of us in AI-driven discovery? Where is our share of voice across ChatGPT; Gemini; Perplexity; and DeepSeek? These are not hypothetical future questions. They are being asked in boardrooms right now; and budgets are beginning to follow.

It is also worth understanding the relationship between SEO and GEO. SEO largely feeds GEO. The content; authority; and structured data signals that determine Google rankings are the same signals that AI engines use to decide which brands to cite in generated responses. For the foreseeable future SEO and GEO are not competing priorities; they are layered ones. This means SimilarWeb’s existing SEO intelligence product does not become obsolete; it becomes the foundation layer of a broader measurement stack.

But the truly compelling implication is the emergence of an entirely new market: GEO intelligence. Attribution is increasingly happening inside LLM responses rather than through tracked clicks and search rankings. Brands will need to understand and influence those channels the same way they learned to understand and influence Google. And here is where the complexity argument becomes very powerful as an investment thesis.

Measuring SEO meant scraping Google and Bing. Two surfaces. Relatively contained. Measuring GEO means tracking ChatGPT; Claude; Gemini; Grok; Perplexity; DeepSeek; and whatever surfaces emerge next. Each one has different citation behaviour; different content preferences; different update frequencies; and different referral patterns. The network complexity does not double or triple relative to SEO measurement. It multiplies by an order of magnitude. There are vastly more interactions to measure; more integrations to build; and more interpretation required to make the data actionable.

That complexity is not a problem for SimilarWeb. It is an opportunity. Complexity creates value. The harder the measurement problem; the higher the willingness to pay for someone who can solve it. If SimilarWeb successfully builds out its GEO intelligence segment; it will not be building something comparable in size to what the SEO intelligence market was. It will be building something significantly larger; because the problem is significantly harder and the number of surfaces to monitor keeps expanding. The GEO market at maturity could dwarf the SEO software market that SemRush and SimilarWeb have been competing in for the past decade.

SimilarWeb already has dedicated traffic trackers for ChatGPT; Claude; Gemini; Grok; Perplexity; and DeepSeek as distinct product lines. They have an AI Share of Voice Monitor; AI Citation Analysis; AI Prompt Analysis; and AI Sentiment Analysis already in market. This is not a roadmap item. It is a live product suite that is already ahead of what any competitor has assembled. The market has not priced this in.

It is also worth noting that the financial industry’s appetite for alternative data is growing rapidly and SimilarWeb is positioning itself directly in that flow. The company recently deepened its partnership with Bloomberg; embedding its web traffic and digital intelligence data directly into the Bloomberg Terminal. This means that every institutional investor; analyst; and portfolio manager using the Terminal now has access to SimilarWeb’s data as part of their standard research workflow.

The strategic significance of this goes beyond the direct revenue it generates. Bloomberg Terminal users are among the highest-paying data consumers in the world. Getting embedded into that workflow is not just a distribution win; it is a credibility signal. It puts SimilarWeb’s data in front of the exact audience that will pay a premium for reliable alternative data signals; and it creates a natural expansion path as more investors come to rely on web traffic and app data as a standard input into their equity research process. As alt data becomes table stakes in institutional investing rather than a niche advantage; SimilarWeb’s Terminal presence means they are already inside the workflow before the demand fully arrives.

Confirmation of the Value

The most important external data point for this thesis landed recently. Adobe announced the acquisition of SemRush; SimilarWeb’s closest competitor; for $1.9 billion in cash.

SemRush and SimilarWeb have slightly different product profiles today but they are competing for increasingly overlapping budgets and are on a collision course for the same enterprise marketing intelligence market. The fact that Adobe; one of the largest marketing software companies in the world; decided to pay a significant premium to own a web intelligence asset tells you something important about how the category is being valued by strategic buyers.

The numbers make the mispricing obvious. SemRush has revenues of roughly $450 million and was acquired at approximately 4.3x revenue. SimilarWeb has revenues of $283 million and trades at roughly 0.8x revenue. Adobe did not pay 4.3x revenue for SemRush’s current earnings. They paid it for the GEO opportunity; the data moat; and the strategic positioning in a world where digital discovery is fragmenting across AI surfaces. The exact same logic applies to SimilarWeb. The market just has not done that math yet.

This is however a two-sided sword. On one side the Adobe deal confirms that SimilarWeb is likely meaningfully undervalued based on the strategic value of its data asset and its GEO infrastructure. On the other side the deal signals that the GEO race is intensifying significantly. Adobe bringing its distribution; balance sheet; and enterprise relationships behind SemRush creates a well-resourced competitor. In a winner-takes-most measurement market; the losers get left behind entirely. The stakes just got higher.

The question then is whether SimilarWeb can compete. I went through their hiring activity and product architecture in detail and the picture is more promising than the stock price implies. The technical language in their job descriptions points to deep integration with foundational model companies; not surface-level partnerships. They already have live product lines tracking six major AI surfaces simultaneously. Their agreement with Manus AI; subsequently acquired by Meta; serves as an early blueprint for embedding SimilarWeb data into autonomous agent workflows. These are early signals; but they point in the right direction.

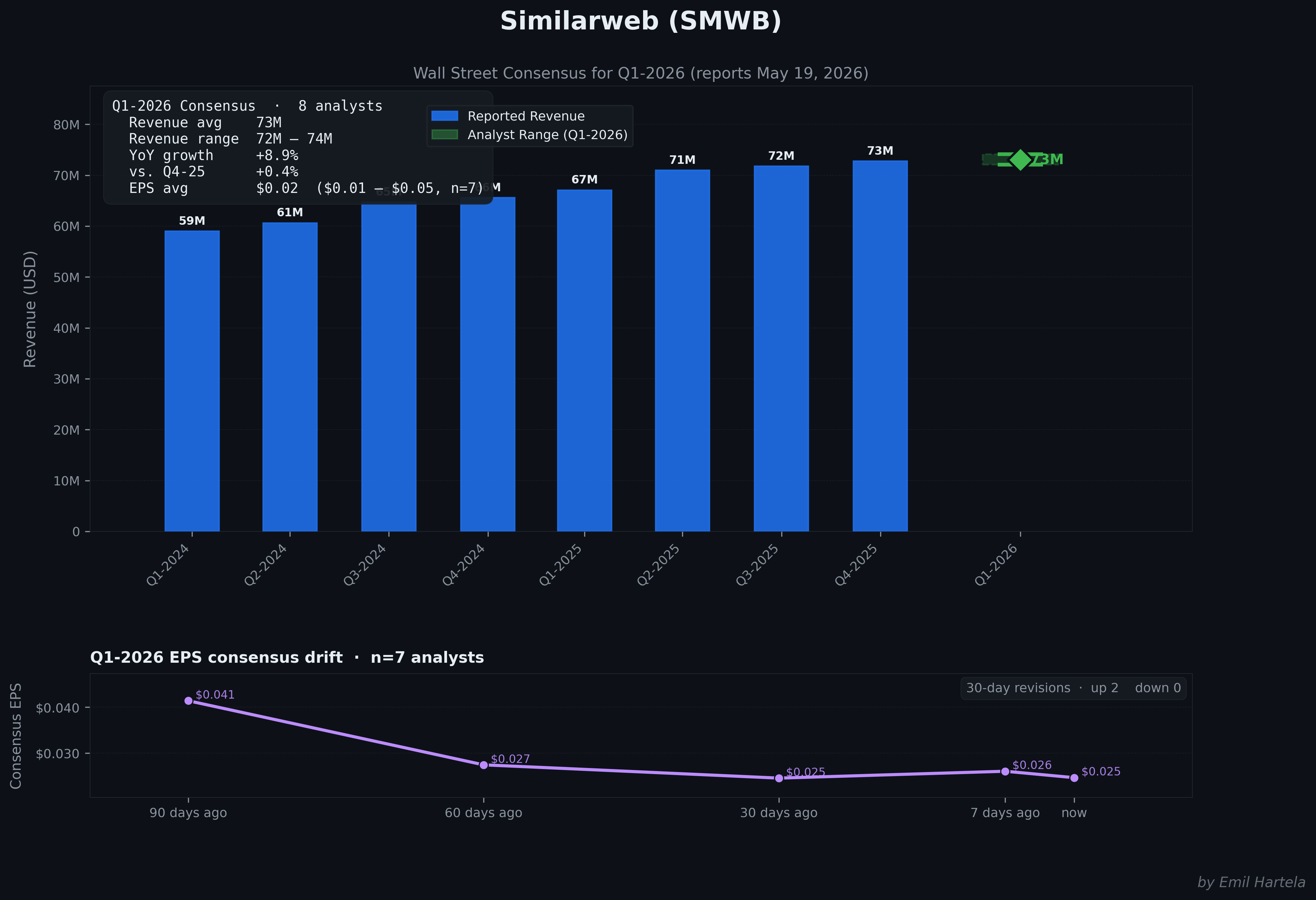

The market is currently in wait-and-see mode on the AI contracts specifically. Several large deals were delayed last quarter and it remains unclear how recurring these contracts will ultimately be. That uncertainty is legitimate and is part of why the stock sits where it does.

One further point worth making about the AI tailwind that goes beyond GEO. AI-assisted development has produced a staggering volume of new apps; SaaS products; and digital businesses. The App Store is expanding at a pace that would have been unimaginable a few years ago. As it happens SimilarWeb has app analytics. More apps and more SaaS competition means more operators who need an edge on their competitors. More brands entering crowded digital markets means more demand for the kind of competitive intelligence SimilarWeb provides. The vibe coding era does not just create more things for SimilarWeb to measure. It creates more customers who need the measurement. Both sides of that equation benefit SimilarWeb.

Summarizing the Turnaround Thesis

The core of the thesis is straightforward. SimilarWeb sits at the intersection of two compounding tailwinds; the explosion of GEO as a new measurement category and the growing demand for proprietary web behavioural data from AI companies. If executed well; either of these alone could meaningfully re-rate the stock. Together they represent a genuinely transformative opportunity for a company that already owns the underlying data infrastructure required to win in both.

The entry point makes the asymmetry compelling. At roughly 0.8x trailing revenue with $72 million in cash and no debt; the market is pricing in very little optionality. You are essentially paying for a semi-functional SaaS business and getting the GEO infrastructure; the AI data licensing pipeline; the Bloomberg Terminal integration; and a decade of proprietary data accumulation for close to free. The Adobe-SemRush deal has established what a strategic buyer is willing to pay for a comparable asset; and the gap between that implied valuation and where SimilarWeb trades today is significant.

The Risks

The first risk is one I already touched on: winner-takes-all dynamics could end up destroying SimilarWeb entirely. But this is a risk you have to accept if you want the big return. The way I see it the stock can either go to zero or become something ten times bigger. There is not much middle ground in a market where the dominant measurement layer captures most of the value and the losers become irrelevant.

The second risk I think deserves to be taken seriously is the company’s culture and commercial practices. Looking at Glassdoor the sales organisation is clearly not a happy place. This likely explains a meaningful portion of the poor NRR numbers. Management has also acknowledged that their current product packaging is outdated and does not allow existing customers to scale their usage aggressively enough. If they cannot fix the sales and account management function they will lose the GEO race regardless of how good the underlying data is. Winning new contracts and expanding existing ones requires commercial execution; and right now that is the weakest part of the business.

A further concern is funding. SimilarWeb currently has a decent cash position but winning the GEO intelligence race could turn out to be expensive. If the stock continues to drift lower; raising capital becomes increasingly dilutive and difficult. Reflexivity works against you here; a lower stock price makes it harder to fund the future; which makes the stock go lower.

And finally privacy regulation is a real and underappreciated risk. The EU is already moving aggressively to restrict how behavioural data can be collected and used. The US could follow with its own framework. Stricter privacy laws mean higher compliance costs; constrained data sourcing; and a potentially narrower moat. The data asset that makes SimilarWeb valuable today is partly dependent on data collection practices that regulators are actively scrutinising.

A Final Note

I think this opportunity is worth keeping a very close watch on. I am genuinely close to pulling the trigger and initiating a position. The upcoming earnings call and how the rest of this year develops will be decisive; particularly whether the delayed AI contracts close; whether NRR shows any signs of improvement; and whether the GEO product suite starts generating meaningful traction in enterprise accounts.

I will continue to monitor the situation closely and publish my findings on the name as the story develops.

If you found this piece useful feel free to share it; and consider checking out some of my other work. Thank you for reading.