Innventure and the Data Center Cooling Bottleneck

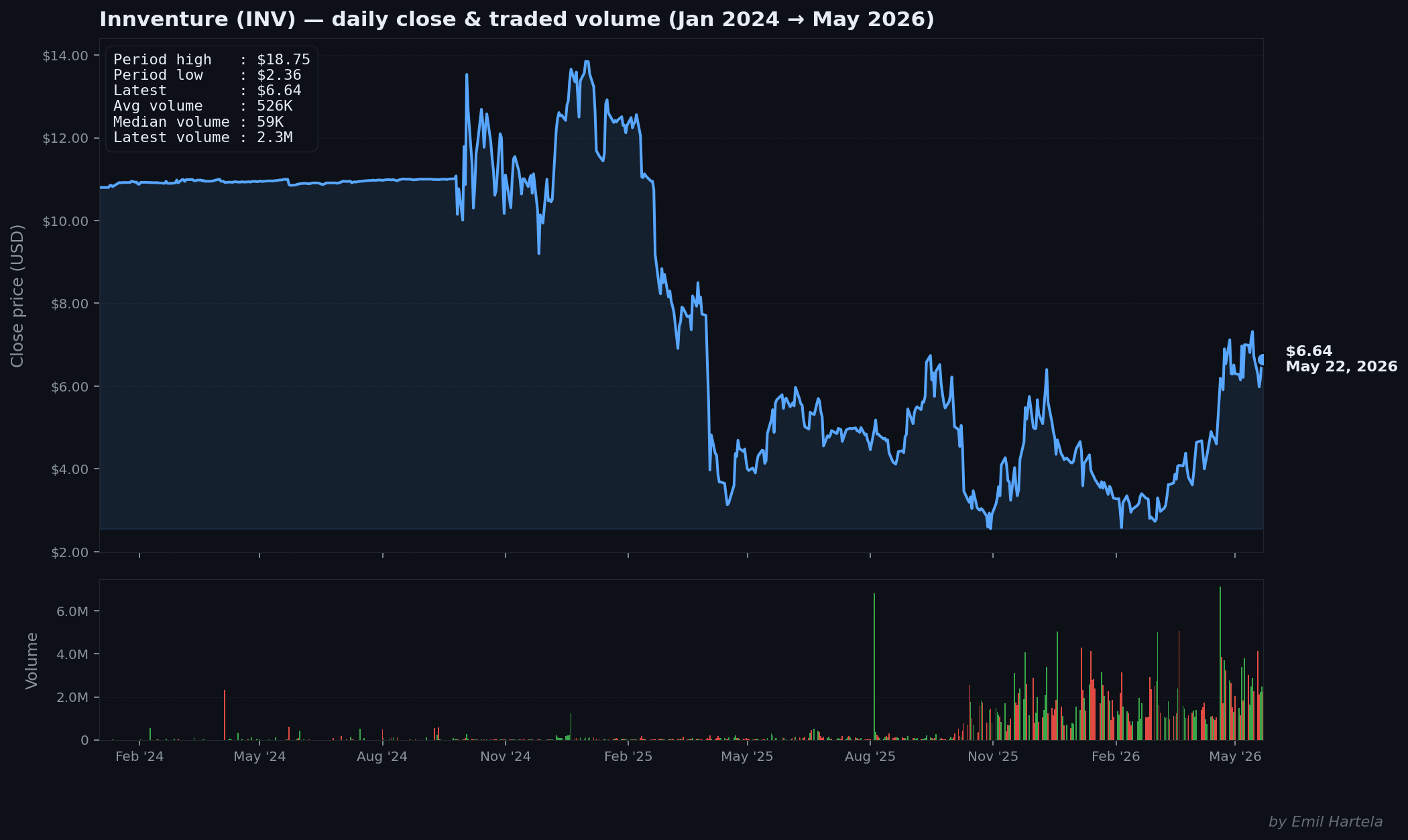

All my research into $INV so far, in one place

The market is currently full of AI bottleneck theses, especially around photonics. Data center stocks have already been bid up aggressively, and an insane amount of capex is pouring into the field. If you believe AI in all its forms is real, especially the agentic AI inference demand that is now ramping, then the bottleneck in this writeup should genuinely interest you.

I found the name in a slightly unusual way. I asked Grok for several interesting bottleneck theses outside of photonics, ones that have not yet been hyped to the same degree. The original thesis traces back to AAIG, and there is a fairly active X community forming around the name that has helped me orient myself as I dug in. I also subscribed to MVC Investing after someone in the comments mentioned they were looking into the name as well. So this is not a lone-genius writeup; it is me building on a thread others started and trying to take it deeper. Go check out both Asset Alliance - AAIG and M. V. Cunha Investing's work.

Let us jump straight into it, starting with the technology and the sector as a whole, because that is what explains why this opportunity exists in the first place.

Why This Opportunity Exists: The Cooling Bottleneck

Billions upon billions are being poured into data centers right now, and the pace is only accelerating. The reason is straightforward once you accept the premise that AI demand is real and durable. It is not just chatbots. Inference at scale, agentic AI that runs long chains of reasoning and calls tools in the background, and the emerging wave of physical AI in robotics and autonomous systems all share one trait: they are enormously compute-hungry, and that hunger compounds. Training a model is a one-time burst, but inference and agentic workloads run continuously, around the clock, across millions of users and tasks. If you believe that future is arriving, then you believe the demand for compute, and therefore for the physical infrastructure that compute runs on, is going to keep climbing for years. That belief is what is driving the capex wave, and it is the foundation everything else in this writeup rests on.

But compute does not exist in a vacuum, and this is where it gets interesting, because the build-out is starting to run into hard physical constraints. The first is power. Electricity demand from data centers is rising fast enough that it is straining grids, pushing up local power prices, and turning into a genuine political issue in the regions where these facilities cluster. The second is water, and this one is sharper than most investors appreciate. There is a growing movement against data centers at the local level, precisely because of how much electricity and water they draw from the communities around them. We have already seen public hearings and local opposition over facilities consuming the water supply that towns rely on, and a meaningful number of new data center projects are effectively stalled because of exactly these power and water concerns. So the constraint is not abstract. It is showing up as stalled permits, community pushback, and rising input costs.

This is the backdrop for what has become a kind of frenzy on X and across the investing world: the hunt for the bottleneck. If compute demand is going to explode but the build-out keeps hitting physical walls, then the companies that sell the picks and shovels, the ones that relieve those bottlenecks, become extraordinarily valuable. The most popular version of this hunt has been photonics, where the names have already been bid up aggressively. It feels like half of the platform has gone into bottleneck-finding mode, with accounts like Serenity leading the charge on the silicon and photonics side. The logic is sound: find the chokepoint, find the company that widens it, and you have found a structurally advantaged business.

This thesis is not about photonics, though. It is about cooling, and specifically about the bottleneck inside the bottleneck. Goldman Sachs has named liquid cooling one of the primary constraints in the data center market, and once you understand the physics of why, it becomes hard to unsee.

Start with how a data center actually works at the physical level. You have rows of racks, each rack filled with chips, and those chips run on electricity. Electricity in means heat out; it is a law of physics, not a design choice. Every watt of power a chip consumes becomes a watt of heat that has to be removed, or the chip throttles, fails, or melts. For most of the history of computing, this heat has been handled the way you would cool a room: with air, supported by water-based systems. You chill the air, blow it across the chips, capture the heat, and reject that heat to the outside, very often by evaporating water in cooling towers. That evaporation is the crux of the water problem. It is not that the chips drink water, it is that the traditional method of getting rid of their heat consumes enormous quantities of it by evaporating it into the atmosphere.

So here is the first reason this trade is interesting. Water is a finite resource, the political and regulatory pressure against data centers consuming it is mounting, and the traditional cooling approach is directly in the crosshairs. Something has to change in how these facilities reject heat, and that pressure is creating a forced migration toward new approaches.

The first step in that migration is liquid cooling, and the version most widely deployed today is what is called single-phase direct-to-chip. Instead of cooling the air in the room, you bring liquid directly to the chip. You run cold plates over the hot components, circulate a coolant through them in a closed loop, the coolant absorbs the heat directly at the source, carries it to a cooling unit called a CDU, dumps the heat, and cycles back. The key word is closed loop. Because the coolant recirculates rather than evaporating away, single-phase liquid cooling dramatically reduces a facility’s reliance on outside water. That solves the environmental and siting problem to a large degree. And it solves a second problem at the same time: liquid carries heat away far more effectively than air, so you can pack chips much more densely and run hotter, higher-power processors than air could ever keep up with. For the current generation of AI hardware, single-phase direct-to-chip is the workhorse, and it is genuinely good at its job.

But there is a deeper layer, and this is where the real opportunity lives. Single-phase cooling has a ceiling, and the chip roadmap is heading straight for it. The problem is in the physics of how single-phase works. It removes heat by warming up the liquid, which is called sensible heat, and a given volume of liquid can only absorb so much energy before it gets too hot to keep cooling effectively. To remove more heat, you have only one real lever: move more liquid, faster. And that lever breaks down in three compounding ways as chips get hotter.

First, the penalties of pumping faster do not scale linearly. The pressure you need rises with roughly the square of the flow speed, and the pumping power rises with roughly the cube. So doubling the flow to cool a hotter chip can cost you around four times the pressure and closer to eight times the power. Each generation of hotter chip makes the next increment of cooling disproportionately more expensive. Second, that faster flow creates real mechanical wear: erosion of the channels, stress on pumps, tubing, and connectors, and higher maintenance and failure risk. Third, and most fundamentally, there is a hard wall. Past a certain heat density at the chip surface, no amount of faster flow helps, because the limiting factor stops being how fast you move the liquid and becomes how fast heat can cross from the chip surface into the fluid at all. Beyond that point single-phase simply cannot keep a chip safe, regardless of how much water you throw at it. The consensus figure is that single-phase direct-to-chip becomes unviable somewhere around 2,500 watts per chip, and the chip roadmap is moving toward and past that line.

This is where two-phase cooling enters, and the distinction is the whole thesis. Two-phase works much like single-phase, with one transformative difference: instead of merely warming the coolant, it boils it. You circulate a dielectric fluid, a liquid engineered to be electrically safe so it can touch sensitive components, over the chip, and at the hot surface that fluid boils and turns to vapor. The vapor travels to a condenser, releases its heat, condenses back to liquid, and returns to do it again, all in a sealed closed loop. The reason this matters is a piece of physics worth internalizing: boiling a liquid absorbs vastly more energy than simply heating it. The energy a fluid soaks up when it changes phase from liquid to vapor, called latent heat, is on the order of several times greater per unit of fluid than what it absorbs by warming up alone. So two-phase can pull far more heat off a chip with far less fluid flow, which sidesteps the exact wall that single-phase runs into. It is not a marginal improvement. It is a different regime of heat removal, and it is the reason essentially every other high-heat industry, from power generation to refrigeration, relies on phase change rather than simple convection.

Put simply: as chips keep getting hotter, the industry runs out of room with single-phase, and two-phase is the architecture that picks up where it leaves off. That transition, from air, to single-phase liquid, to two-phase, is the bottleneck this writeup is about, and the company at the center of it is where we turn next.

Meet the Company: Innventure and Accelsius

The asset that matters here is Accelsius. Innventure is the listed shell that lets you get exposure to it. That framing is worth holding onto from the start, because almost everything interesting about this opportunity lives inside the operating company, while the thing you actually buy on the market is the parent. We will get into what that structure means later. For now, the point is simple: when people talk about the $INV thesis, what they are really talking about is Accelsius.

So what is Accelsius? It is an Austin-based company commercializing two-phase, direct-to-chip liquid cooling for data centers, the exact architecture described in the previous section. It was founded in 2022 by Innventure, which operates as a create-and-operate platform that takes promising technology, builds a company around it, and scales it. Accelsius is the cooling business that emerged from that model, and it has become the centerpiece of the entire Innventure story.

The technology has serious provenance, and this is one of the more important and underappreciated facts about the company. Accelsius’s core two-phase cooling technology originated from research done at Nokia’s Bell Labs, one of the most credentialed industrial research institutions in the world. Crucially, Accelsius did not merely license this technology. It bought the underlying patents outright from Nokia, through a patent purchase agreement, while other software and know-how is licensed alongside it. Owning the foundational patents rather than renting them is a materially stronger intellectual property position, and the Bell Labs lineage gives the technology a pedigree that is rare for a company this young. The science had been developed at Bell Labs over several years but never productized, and Accelsius was built to take it to market.

The product line is branded NeuCool, and it is worth understanding what they actually sell, because it spans several layers of the cooling stack. At the chip level, the system uses what are effectively boiling cold plates, mounted directly onto the hot components, where the dielectric refrigerant nucleates into vapor before traveling to a coolant distribution unit to condense and cycle back. On the capability front, Accelsius has demonstrated some of the most impressive thermal numbers in the industry: in testing, its cold plate handled 4,500 watts on a GPU-socket test vehicle, reportedly the highest documented load for direct-to-chip liquid cooling, and notably the cold plate did not reach its own limit, the test equipment simply ran out of power. That figure matters because it shows headroom well beyond where single-phase gives out and well beyond current chip generations.

On the product side, the line includes the IR150, an integrated rack that combines the cooling and the IT space into a single plug-and-play enclosure rated to 150 kilowatts, designed for straightforward deployment without redesigning a facility’s plumbing, and the MR250, a row-based coolant distribution unit rated to 250 kilowatts and beyond, which Accelsius has described as the first in a planned series of increasingly powerful multi-rack systems with higher-capacity units on the roadmap. The system runs on a low-global-warming-potential, minimal-PFAS dielectric refrigerant, which matters given the environmental and regulatory backdrop. In short, Accelsius is one of a very small number of companies delivering true two-phase direct-to-chip cooling at rack scale today, with a credible product family already in the market and bigger systems in development.

Now the ownership and capital picture, because this is where the story gets its strategic weight. The most important recent event was Accelsius’s funding round, which closed with Johnson Controls leading and Legrand participating. The round valued Accelsius at roughly 665 million dollars post-money, and Innventure’s economic stake in Accelsius sits in the region of 43 percent, which is the figure to anchor on when you think about how much of Accelsius’s value flows through to the listed parent. Innventure consolidates Accelsius in its financials, so when you look at Innventure’s reported revenue, you are largely looking at Accelsius’s revenue.

The identity of those backers is the part worth dwelling on, because strategic investors are a different signal from financial ones. Johnson Controls is a roughly fifty-billion-dollar building systems and HVAC giant with deep relationships in the facilities and mechanical infrastructure of large buildings, exactly the layer where data center cooling lives. Legrand owns rack power distribution brands like Raritan and Server Technology and has strong penetration in data center rack infrastructure, particularly in Europe. So the two investors are not passive check-writers hoping for a markup. They are operators who bring distribution, manufacturing credibility, and customer access, and Legrand in particular has framed the relationship as a pillar of its data center strategy, with the two companies collaborating on integrating two-phase cooling into rack infrastructure. When giants like these put capital and their own reputations behind a small company’s technology, it is a stronger validation than a venture fund writing a check, because they are staking their customer relationships on the technology working.

Innventure itself is the publicly traded entity, and Accelsius is its flagship, though not its only, operating company. The parent also holds other ventures, including AeroFlexx in packaging and Refinity in advanced materials, but the overwhelming share of investor attention, and of the thesis, is on Accelsius and the cooling opportunity. That concentration is deliberate on the part of most people following the name, because cooling is where the large, near-term, AI-driven opportunity sits.

So to summarize the asset before we get into how to think about valuing it: Accelsius is a two-phase direct-to-chip cooling company with technology bought outright from Nokia Bell Labs, a product family already shipping across rack and row formats, industry-leading demonstrated thermal performance, a roughly 665 million dollar post-money valuation from its latest round, two major strategic backers in Johnson Controls and Legrand, and Innventure as the roughly 43 percent owner and the listed vehicle through which public investors get exposure. That is the thing at the center of all of this. The next question is how you actually put a value on something like it, and that is where most people, in my view, reach for the wrong tool.

How to Value Something Like This: The Make-or-Buy Lens

The first thing I did when I started modeling Accelsius was the obvious thing: I tried to map out their revenue. Management is guiding for a 100 million dollar run rate by the end of the year, which means roughly 8 to 9 million dollars of revenue in December, exiting at that pace. Full-year 2026 revenue is likely to land somewhere around 30 to 40 million. On top of that, management has said they see a pipeline supporting something like eight times their 2026 revenue plan, which points to a pipeline north of 200 million dollars. The trouble is that it is genuinely hard to pin down how much of that pipeline actually converts to sales, and over what timeframe. So the revenue model gives you a rough shape, but not a foundation you would want to build a valuation on.

Once you get past the next year or so, management has not told us much, so you are forced to reach for industry TAM figures and sector growth rates. The number that gets quoted repeatedly is a roughly 40 billion dollar cooling TAM by 2033. But here is the thing: estimating how Accelsius fits into that TAM picture does not actually help very much, in my opinion. Saying they land at, say, 20 percent market share is just guessing. This is a startup. Picking a share number a decade out and multiplying it by a TAM is the kind of math that feels rigorous and is really just optimism with a calculator. So I do not think the conventional revenue-and-share model is where the real signal is.

Instead, there are only two things I think you can actually rely on when looking at Accelsius, and both come from outside the company’s own projections.

The first is industry validation from the players who set the standards, namely the chipmakers, NVIDIA and AMD. Two-phase is still in its early innings, and it is genuinely unclear exactly when the threshold gets crossed where single-phase no longer cuts it. It could be 2028, it could be later, it could be earlier. What matters is that we get confirmation from the reference designs that NVIDIA and AMD publish, because their roadmaps dictate what the entire ecosystem builds around. If Jensen comes out and says two-phase cooling is inevitable for the 2028 generation, we have a dramatically clearer picture than we have today. Until the chipmakers bless it, two-phase adoption is a question of when, and the chipmakers are the ones who answer that question.

The second thing to watch is what the incumbents are doing, and this is the heart of how I think you should value this asset. I will get into the competitive picture in detail later, but for now the exercise is to put yourself in an incumbent’s seat. The big cooling players are mostly doing air and single-phase today. But they know perfectly well that as chips get hotter, they will have to move to better cooling solutions. So they face a simple question: make or buy. Should they build two-phase technology in house, or acquire a company that already has it?

Building it in house takes real time and effort. These are large companies with plenty of capital, so money is not the constraint. Time is. Two-phase is a different engineering discipline, and developing it from scratch, designing, testing, and iterating through the reliability qualification that mission-critical cooling demands, takes several years. My guess is that they do not have those years to spare, and here is why. Once chips cross the threshold where single-phase can no longer cool them efficiently or economically, there will be a scramble, a window of a few years where everyone needs two-phase at once. We are already seeing the beginning of this. As I mentioned, two of Accelsius’s own investors are already strategic players who have chosen to buy in rather than build. And when you look at Accelsius’s main competitor, ZutaCore, you see the identical pattern: the incumbents circling that company also chose to buy exposure rather than develop their own. So far, essentially every major player that has looked seriously at this field has decided to bet on either Accelsius or ZutaCore, rather than join the game as a builder.

When you combine the make-or-buy logic with the future TAM of the sector, you start to get a much better picture of what an asset like Accelsius could be worth. The right question is not “what revenue will Accelsius book in 2030.” It is “how much would an incumbent be willing to pay to be in the two-phase cooling game at all.” And bear in mind the structural setup: there are several incumbents who will need two-phase, and not many companies actually making it yet. More buyers than assets is exactly the condition that drives prices up.

If you look at other sectors that have seen rapid valuation increases over the past few years, a common pattern emerges: incumbents go on acquisition sprees in the early innings of commercial sales, right at the proof inflection where the technology is de-risked but adoption has not yet ramped. Accelsius is not quite at that point yet, but we are starting to get closer to peak incumbent demand for the technology. The incumbents will look at a 40 billion dollar market and think, we need to be part of this, what are we willing to pay to participate. They obviously need upside on the purchase, but a 40 billion dollar market that is still growing can plausibly support well more than 40 billion in total value creation across its players. So it is not hard to see how an incumbent could be willing to pay several billion dollars for an asset that lets them play in that market, or even into the tens of billions if you want to be really optimistic about the scramble.

This is why the hype around Innventure is growing. Innventure owns roughly 43 percent of a potentially multi-billion-dollar company, and that ownership is being acquired through a listed vehicle that currently trades at a fraction of what that stake could be worth if the make-or-buy scenario plays out. It is genuinely easy to construct a scenario where Innventure is worth several hundred percent more than it is valued at today. The make-or-buy logic gives the story a floor that no revenue forecast could, because it does not require Accelsius to win the open market on its own merits, only to remain one of the few buyable ways into a market everyone will need to be in.

That is the bull case at its strongest. But there are some important things to keep in mind that complicate it, and those are what I want to focus on next.

The Good, the Bad, and the Ugly

So far we have concluded that there is a large opportunity ahead of Accelsius, potentially valuing the company at multiple billions in the future. Innventure’s stake in that is roughly 43 percent. So it is not too big a stretch to see Innventure valued at double or triple where it trades today, somewhere in the 10 to 20 dollar range, if the scenario plays out. That is the part that gets people excited, and I think it is genuinely plausible.

But there are multiple risks and several things that make the story considerably less sexy than the headline. It is worth going through them honestly, because the difference between a good outcome and a bad one here runs straight through these issues. I will take them as the good, the bad, and the ugly.

The good, or at least the manageable. The first thing to internalize is that you only own 43 percent of Accelsius, and the rest of Innventure is other companies, namely AeroFlexx in packaging and Refinity in advanced materials. These other positions in the Innventure portfolio are interesting ventures, but they are ventures, which means they carry the same trait every venture does: the potential to require more capital and bring more dilution to the whole. When I value Innventure, I would not assign a large amount of value to the businesses beyond Accelsius. Yes, they might be worth 100 million or so collectively, but they also carry the potential to dilute a similar amount as they get funded. So I treat them as roughly a wash, neither a hidden treasure nor a disaster, just not the reason to own this. The reason to own this is Accelsius, and everything else is secondary.

The bad. The first real problem with Innventure is, obviously, dilution. We have already seen a great deal of it over the past year, and it is hard to see how, over the long term, there would not be more. This happens at two levels: at the holding company level, as Innventure raises capital to fund operations, and inside the holdings themselves, as Accelsius and the others raise their own rounds. Cumulatively, this can have a large impact on returns for anyone who wants to own this for a few years or more. A thesis can be completely correct on the technology and the eventual buyout and still deliver disappointing per-share returns if the share count keeps climbing in the meantime. This is the single most important thing for a long-term holder to keep front of mind, and it is the reason the capital structure matters as much as the technology.

The ugly. In 2021 there was a Hindenburg short report that painted a very negative picture of Innventure, focused largely on PureCycle, one of its ventures. This report came out around the time PureCycle went public, and before Innventure itself was listed. Like most short reports, it was aggressively negative, and short sellers are not neutral parties. But setting the tone aside, it identified some patterns that have, to some extent, repeated, and those patterns are worth understanding rather than dismissing.

The first pattern to be aware of is management’s tendency to make bold revenue claims and strong projections. With PureCycle, Innventure repeatedly signaled that the company was close to an inflection point and that revenues would soon be far higher. The useful thing about a five-year-old claim is that you can now fact-check it. Looking at PureCycle today, roughly five years later, it generates barely any revenue. Back in 2021, many investors listening to the inflection talk were modeling PureCycle making billions in revenue around now. In reality it is doing a couple of million, orders of magnitude below the guidance-era expectations. The lesson is straightforward: the management commentary should not be taken at face value. If Innventure’s management says they are at an inflection point, it is far better to wait for the proof than to take their word for it.

The second focus of the report was the team’s poor track record of taking portfolio companies to market. Most of their past ventures have gone bankrupt, and the report argued that they have consistently taken companies public too early. The pattern is related to the first point: the management comes across as highly opportunistic and quite promotional, spending a lot of time and effort making each venture look like the next big thing.

Now I want to address these claims directly, because the honest answer is more nuanced than either “ignore it” or “avoid the stock.”

First, on governance, something important has recently changed. An activist investor, Ascent Capital Partners, took a stake of around 7 percent and sent a pointed public letter to the board. The letter was sharply critical, essentially saying its patience had run out, and it made specific demands: materially cut corporate overhead, stop funding ventures beyond Accelsius until things stabilize, redirect capital into Accelsius, and reconstitute the board with more independent, experienced operators. Over the following weeks, the company responded substantively. It added new directors, published a formal capital allocation framework, and made meaningful cost cuts, with general and administrative expenses coming down significantly. The activist subsequently followed up with a public letter of support. This matters, and it is a genuine positive, because the activist pressure pushed the company toward exactly the disciplines that address the biggest concern here, namely overhead and dilution, and it tightened the focus onto Accelsius as the priority. Engaged shareholders forcing better capital discipline is precisely what you want to see in a holdco that has historically been criticized for the opposite. One honest caveat: an activist who has done well on the position has every incentive to declare victory, so the support letter is encouraging rather than a clean bill of health. But the direction of travel on governance is clearly better than it was.

On the Hindenburg report itself, my honest view is that it is largely correct in arguing that Innventure’s management should not be trusted completely. Where I think the report overreaches is in using failed ventures as evidence of poor performance, because on average ventures tend to fail; that is the nature of the model, and a string of failures is not by itself an indictment. You underwrite a venture platform on whether the winners are big enough to cover the losers, not on the body count. But, and this is the part I cannot wave away, it does worry me when a team consistently jumps on hype cycles and markets its story so aggressively that it repeatedly misses its own targets. I would much rather back a team that gives projections you can trust and then beats them quietly. So the management question is a real mark against the name, and I am not going to pretend otherwise.

But here is the most important thing, and it is the reason none of the above is disqualifying. Accelsius has its own management. Innventure has a parent-level management team whose record is, let us say, mixed. But Accelsius, the operating company that actually matters, is run by a separate team, and that team looks considerably stronger. So the promotional-parent concern and the quality of the operating business are two different questions, and conflating them is a mistake in either direction. The next section is where I want to dig into the Accelsius team and the company’s recent activity, because that is what gives the clearest picture of whether the operating business is the real thing the bull case needs it to be.

The Accelsius Team and the Evidence on the Ground

If the parent-level management is the part of this story that gives reason for caution, the Accelsius operating team is the part that gives reason for confidence, and the contrast is sharp enough that it deserves its own section. This is a separate group of people, with a different profile, and they are the ones actually building and selling the product.

Start with the CEO, Josh Claman. He is not a promoter cut from the create-and-operate mold; he is a career data center and enterprise technology operator with around thirty years in the industry. His background includes senior leadership at Dell, where he ran large multi-billion-dollar units including serving as general manager of Dell UK and heading enterprise business for the Americas, along with time at companies like NCR and AT&T. That is precisely the kind of profile you want selling infrastructure into the same enterprise and hyperscale buyers Accelsius is targeting; he has sat on the other side of those tables for decades.

The technical bench is the part that should reassure you most, because it directly answers the question of whether the technology is real. The CTO, Dr. Richard Bonner, is a genuine two-phase thermal specialist: 18 years in thermal product development, over fifty published papers, five US patents, a former AIChE Transport and Energy Processes Division Director, and a PhD in chemical engineering from Lehigh. This matters enormously in context, because one of the sharpest criticisms in the Hindenburg report about a different Innventure venture was that the team lacked deep domain expertise in the relevant science. Here, the opposite is true: the person leading the technology is an actual boiling and two-phase heat transfer expert. The supply chain side carries serious hardware-scaling pedigree as well; the supply chain lead spent 12 years at Dell running server supply chain planning, with prior engineering experience on NASA’s Orion program at Lockheed Martin, which is exactly the discipline a company needs when its bottleneck is manufacturing scale rather than invention. The broader finance and operations leadership brings backgrounds from companies like Dell and National Instruments that are known for scaling hardware revenue from millions into billions.

So the picture of the operating team is a credible, operator-and-engineer group with real data center, two-phase, and hardware-scaling expertise. That is a meaningful rebuttal to any lazy dismissal of Accelsius as just another over-marketed Innventure venture. The parent carries the promotional history; the operating company is run by people who look like they know exactly what they are doing.

Now to the evidence on the ground, because credentials matter less than what a company is actually doing, and over the past year Accelsius has put out a steady stream of milestones and signals that, taken together, are more substantive than I expected when I started digging. Let me walk through them.

On products and performance, the company brought its NeuCool line to general availability, including the IR150 integrated rack launched at Data Center World and the MR250 row-based CDU launched at the OCP Global Summit, where management explicitly described it as the first in a planned series of increasingly powerful systems with higher-capacity units on the 2026 roadmap. On raw capability, the demonstrated 4,500 watts per socket result, where the cold plate did not reach its own limit and the test rig ran out of power first, remains one of the most impressive thermal numbers publicly shown in direct-to-chip cooling.

On third-party validation, this is where the signals get genuinely interesting, and a lot of it comes from sources most investors never bother to read. Independent engineering analysis, attributed to Jacobs, has put numbers on the efficiency case: in a modeled 10 megawatt data center, two-phase direct-to-chip showed roughly 35 percent lower annual operating expense and around 12 percent lower five-year total cost of ownership versus single-phase, with no change in capital expenditure. That matters because it is an outside firm rather than the company validating the economics.

On deployments and channel, Accelsius has a named deployment at a large data center campus through DarkNX, a 300 megawatt project that stands as the single biggest named deployment in the space. It has placed equipment at Equinix’s co-innovation facility in Ashburn, the data center capital of the world, which means the technology is being shown to essentially every major operator that passes through. And the partnership with Legrand is visibly operational rather than just a press release: at Dell Technologies World, Accelsius exhibited its IR150 inside Legrand’s booth, showing the two-phase rack alongside Legrand’s power and networking gear, which is the strategic investment actually manifesting on a trade-show floor.

Perhaps the most striking single signal came from a separate event entirely. Accelsius was featured as a technology partner at the ribbon-cutting for a major server vendor’s customer solutions center, a facility of exactly the kind where that vendor walks its own enterprise customers through validated technology. The company’s own marketing lead posted about it, and the imagery showed the cooling technology on display in the vendor’s innovation lab. I want to be careful here, because this is validation and exposure rather than a disclosed supply contract, and it should not be inflated into one. But being placed in front of that vendor’s customer base, in that vendor’s own facility, is a meaningful step for a company this size, and it is not the kind of thing that happens to a business that is all marketing and no substance.

Then there is the hiring data, which is the kind of primary research that almost nobody does and that I find genuinely revealing. You can learn a lot about where a company thinks it is going by who it is paying to hire. Accelsius has been staffing like a company preparing for a production ramp, not like a lab still searching for product-market fit. It brought on a global commodity manager, a role whose entire purpose is to lock down annual component supply contracts, which you create when you have forward order visibility, not when you are running pilots. It has a manufacturing operations function at the VP level, unusual at this revenue stage, along with production and shift roles and systems engineers with hardware and aerospace backgrounds. None of that is an organization you build on speculation. You build it against demand you can see coming.

And there is a constant drumbeat of independent commentary reinforcing the direction. Data center industry voices have been writing about “building for a two-phase future” as the prospect of one-megawatt racks comes into view, and the IR150 launch drew a wave of posts from infrastructure professionals calling it a significant step for AI-ready cooling. Even Accelsius’s own deployment partner, DarkNX, has publicly framed two-phase as core to building AI environments that can handle both current high-density chips and future Rubin-class infrastructure without major redesigns later. When a customer is talking publicly about future chip generations, that is the kind of forward signal you want to see.

None of this is a contract, and none of it is revenue at scale. It is validation, channel activity, credentialed leadership, and hiring that all point the same direction. But that is exactly the point: in a pre-inflection business, the progression is the signal, and the progression here is consistent and improving. The operating company is doing the things a real company on the cusp of an inflection does. Whether that converts into the outcome the bull case needs is the open question, and it is what the final section is about.

The Competition and the Industry Picture

I have referred to the competitive landscape a few times, so let me lay it out properly, because understanding who Accelsius is actually up against, and where the whole industry sits on the adoption curve, is essential to judging the thesis.

At the leading edge of two-phase direct-to-chip, this is effectively a two-horse race between Accelsius and ZutaCore. ZutaCore is the other credible pure-play two-phase company, and like Accelsius it is backed by serious strategic investors, in its case Carrier, alongside a hyperscaler server ODM and others, which gives it a strong direct line into hyperscaler design-in. Both companies have credible technology and early deployments, and crucially neither has yet landed the named, high-volume hyperscaler contract that would settle the race. So the outcome is genuinely open, and the two are not even competing on quite the same axis, which is the most useful thing to understand about the matchup.

There are two different ways to measure cooling performance, and Accelsius and ZutaCore have each pulled ahead on a different one. The first is per socket, meaning how much heat you can pull off a single chip. Here Accelsius leads: it has demonstrated 4,500 watts on a socket-level test vehicle, the highest documented figure for direct-to-chip, and the cold plate did not reach its own limit. ZutaCore’s HyperCool has been certified to cool up to roughly 2,800 watts per processor, which is formidable but lower. This is the chip-level headroom that matters most as the next chip generations push socket power up, because it is the axis on which single-phase physically gives out. The second measure is per unit, meaning how many racks one cooling unit can serve. Here ZutaCore currently leads: in late 2025 it announced end-of-row coolant distribution units rated at 1.2 and 2 megawatts, which serve many racks from a single centralized box. Accelsius’s row-based unit, the MR250, is rated at 250 kilowatts, with higher-capacity systems promised for 2026 but not yet shipped.

So the honest current state is that Accelsius leads on chip-level thermal performance while ZutaCore leads on system-level capacity per unit, and they are partly optimizing for different buyers. Accelsius’s integrated, plug-and-play products are well suited to enterprise, colocation, and neocloud players who want to adopt incrementally without redesigning a facility. ZutaCore’s high-capacity end-of-row units are aimed more squarely at hyperscale-density greenfield deployments. Which approach wins the early volume depends on whether the near-term buying comes from hyperscalers building from scratch or from a broader set of operators retrofitting and adopting rack by rack. It is worth being clear-eyed here: on the specific metric of capacity per cooling unit, which several knowledgeable observers argue is what ultimately decides the winner at the hyperscale frontier, Accelsius is currently behind, and the higher-capacity unit it has promised for 2026 is one of the more important things to watch.

It is also worth saying that this will not be a two-company market forever. The physics is known, and as the field matures more players will be able to enter, whether established thermal names or new entrants. There are already adjacent and emerging players in two-phase and advanced direct-to-chip beyond these two. But at the leading edge today, with shipping general-availability products, named deployments, and strategic backing, Accelsius and ZutaCore are clearly the front pair, and notably almost every incumbent that has looked seriously at the space has chosen to back one of them rather than build, which is the make-or-buy dynamic in action.

Now the bigger competitive reality, which is that the real near-term competition is not the other two-phase company at all; it is single-phase. The single-phase incumbents are the ones with the installed base, the relationships, and the mature products today, and they are formidable. The market leaders here, names like CoolIT, Vertiv, and Schneider, already ship single-phase coolant distribution units at very high capacity. CoolIT’s largest row CDU is rated at 2 megawatts and has been deployed at scale, enough to cool many of the densest current-generation AI racks. So when you compare Accelsius’s 250-kilowatt row unit to a 2-megawatt single-phase unit, the gap looks enormous, but a good chunk of that is a product-class difference, an integrated rack and an early row CDU versus a mature high-capacity row product, rather than a pure capability gap. Still, the takeaway is real: single-phase is not a weak incumbent waiting to be displaced. It is a capable, entrenched technology that is being actively stretched to handle more, and it is the thing two-phase has to displace, not merely outperform on paper.

This is what makes the S-curve and the timing question the crux of the entire thesis. Two-phase is sitting at the transition from early commercial deployments into qualification: products just generally available, first named deployments landing, hyperscaler engagement at the proof-of-concept stage, and the current flagship chips still specified for single-phase. The reason single-phase is still the default is that it can be stretched further by brute force, pumping more fluid faster, even though the penalties of doing so rise steeply. So the key question is when the crossover arrives, the point where single-phase genuinely cannot keep up economically and two-phase becomes necessary rather than optional. The honest answer is that nobody knows precisely. It could be 2027, 2028, or later, and estimates keep moving. The chip roadmaps are the accelerant, and the single most important confirmation would come from the chipmakers themselves: if NVIDIA or AMD bless two-phase in their reference designs, the architectures the whole ecosystem builds around, that is the signal that the crossover is locked in. A reference-design win, or a public statement from the chipmakers that two-phase is the path for a given generation, would change the picture far more than any company press release. Watching the reference designs is, in my view, the clearest leading indicator there is.

The photonics comparison is instructive here, and it cuts in two directions. Photonics is the other great AI-bottleneck story, and its valuations have already popped hard, with names reaching multi-billion marks well before the revenue arrived. That tells you frontier-hardware valuations can run years ahead of adoption. But it also tells you that two-phase cooling has not yet had its photonics moment. The story has not gone fully hot, which means, if you believe the direction of travel, this sits earlier in its narrative cycle than photonics did, with arguably a clearer physical forcing function behind it. The flip side, and the genuine risk, is timing: if single-phase keeps getting stretched and the crossover slips out to 2029 or beyond, you are holding a cash-burning, diluting company while you wait for an inflection that keeps receding. That is the central risk of being early, and it is why the dilution discussed earlier matters so much. Being right on the technology and wrong on the timing can still cost you.

One last thread worth pulling, because it points to other ways to play this theme that may be safer than Innventure. Regardless of which cooling company wins, all two-phase systems need an engineered dielectric fluid to boil, and that fluid is a high-value, recurring consumable. The market for these fluorinated coolants is essentially a duopoly between Solstice Advanced Materials, ticker SOLS, the business spun out of Honeywell’s advanced materials arm, and Chemours, ticker CC. These are the coolant suppliers, the picks-and-shovels one layer below the cooling vendors, and they benefit whichever two-phase company wins, and indeed benefit from the broader liquid cooling shift generally. The catch is that both are large, diversified chemical companies where data center cooling fluid is only a slice of the business, so they are not pure plays, and the upside per dollar invested is more muted. But that is precisely the trade-off: they are slower, safer, more diversified bets that capture the theme without the binary technology risk and the holdco baggage that come with Innventure. For an investor who believes in the cooling bottleneck but does not want to underwrite a single early-stage company wrapped in a holding structure, the coolant names are a genuinely more conservative way to express the same view. I find them less exciting and lower-variance, which is exactly why they are worth mentioning: not every way to play a theme has to be the highest-beta one.

With the competitive and industry picture laid out, the final question is what actually moves this from here, which catalysts to watch and how I am thinking about positioning. That is where I will close.

What I Am Watching and How I Think About Positioning

So where does all of this leave me. I want to close with the catalysts I am actually watching and how I think about expressing the trade, because the thesis is only useful if it connects to decisions.

Let me start with the question I have spent the most time on, which is how to express this at all, and specifically whether options make sense. The honest answer right now is that they mostly do not. The options chain for Innventure is poor. The contracts are expensive, the implied volatility is high, and the name does not have proper long-dated LEAPS. What that means in practice is that if you buy the options currently available, you are effectively betting that the stock rises by something like 100 percent within a few months, because anything less and the cost and time decay eat you alive. That is a brutal bar. You can be completely right on the direction and the eventual outcome and still lose on the option simply because the move did not happen fast enough.

To use the options, in other words, you essentially have to bet on market discovery and rerating rather than on a specific news catalyst landing in your window, and that is a genuinely hard thing to time. I will say that the signs of that kind of rerating are not absent. There has been a lot of activity around the name on X, and my own writing on it has drawn a good amount of engagement, which suggests the story can spread and the stock could rerate on hype and attention before any single hard catalyst arrives. But even granting that, the options being this expensive means they are not the ideal way to express the view. You are overpaying for the privilege of being right on a tight clock.

That mostly leaves pure stock, and when it comes to sizing I think you have to remember what this actually is: a venture. The sensible way to invest in a venture is to start small and add as the picture clarifies and the winner reveals itself, rather than going in large on conviction before the evidence is in. So my current thinking, if one wants to play the name at all, is a smaller position first, and then reassess around October, which is when I expect the next meaningful product catalyst, and decide from there whether the picture has improved enough to add. I would also note that, as covered earlier, SOLS and CC are genuinely attractive alternatives for expressing the broader cooling theme with far less single-company and holding-company risk, and for some investors those are the better vehicle entirely.

Now the catalysts themselves, in rough order of how much they would move the story.

The first is the product roadmap, and specifically the higher-capacity unit. I expect Accelsius to announce something around October, possibly earlier, that addresses the hyperscaler segment better than the current line does, following the launch cadence of the past year. If that lands, it closes the per-unit gap to ZutaCore and the single-phase incumbents and materially strengthens the competitive position. If October passes without it, that is a mild negative signal that the roadmap is slipping.

The second, and potentially the most powerful, is a chipmaker reference design. I think there are decent odds that within the next six months we see something like an AMD reference-design announcement, or comparable industry commentary, that validates two-phase for a specific high-power deployment. A reference-design win from NVIDIA or AMD is the single clearest confirmation that the crossover is locked in, because it is the chipmakers, not the cooling vendors, who dictate what the ecosystem builds around. This is the catalyst I would weight most heavily as a leading indicator.

The third is future funding rounds, which could act as a very strong rerating moment in their own right. If Accelsius announces it has completed new financing at, say, a 1.5 billion dollar valuation, the listed parent should see its implied value rise more or less instantly, because that is a fresh, market-set mark on the asset that Innventure owns a large slice of. A priced-up round is the cleanest way the private value gets crystallized into something the public market can point to.

The fourth is straightforward commercial progress: more named contracts on the scale of the 300 megawatt deployment, and crucially, whether booking growth breaks out of its current level rather than staying flat. Bookings accelerating is the proof that the pipeline is converting, and a named, high-volume hyperscaler contract would be the milestone that genuinely settles the bull case.

And the fifth, which is more of a slow-burn macro catalyst, is the environmental and water backlash. If states or regulators begin to say, in effect, that you cannot build new air-cooled or water-hungry data centers, the demand for liquid cooling would rise rapidly, and more investors would catch wind of the story. We are already seeing stalled projects and local opposition over power and water; if that hardens into actual policy, it becomes a forcing function that pulls the whole adoption curve forward, and a two-phase, water-free solution sits right in the path of that shift.

So that is the watch list: the October product cadence, a chipmaker reference design, a priced-up funding round, named contracts and booking acceleration, and the regulatory water backlash. Any one of them moving in the right direction strengthens the case; the reference design and the funding round are the two I think would rerate it hardest.

As for how I think about it overall, the thing complicating this for me is not the technology, which I find genuinely compelling, but the structure. Buying Accelsius directly as a pure play would be far easier to stomach. The added Innventure holding-company layer, with its dilution history and the promotional track record covered earlier, is what gives me pause, and it is the reason I would treat any position here as venture-style: small to start, sized to survive the dilution, and added to only as the catalysts confirm the picture. The honest conclusion is that this is a genuinely interesting, genuinely risky situation where the technology and the make-or-buy logic are the draw and the capital structure and timing are the risk. Whether those balance out in your favor depends a great deal on the catalysts above, which is exactly why I am watching them rather than reaching for the spreadsheet.

Disclaimer: Nothing in this post is financial advice. I am not a financial advisor, and this is not a recommendation to buy or sell any security. It is my own research and opinion, shared for informational and entertainment purposes only. I may hold positions in the names mentioned, and those positions can change at any time without notice. Everything here could be wrong, including the facts, the assumptions, and the conclusions. Do your own research, consider your own circumstances, and consult a licensed professional before making any investment decision. Small, early-stage, and thinly traded names like the ones discussed here carry a real risk of permanent and total loss.