Hims & Hers Earnings Recap: Q1 FY2026; Soft Print, Raised Guide

Q1 FY2026 saw a narrow revenue miss and sharp EPS drag from restructuring charges, but my pre-earnings model beat consensus with a 1.12% MAPE.

The GLP-1 Pivot’s Immediate Sting

International revenue surged 969% YoY to $78.2M, offsetting an 8% YoY decline in U.S. revenue, but $33M in restructuring charges tied to the GLP-1 pivot still dragged the headline print into a narrow miss. This recap breaks down the Q1 FY2026 numbers, checks my pre-earnings model’s accuracy, and reflects on what the results mean going forward. Remember, none of this is investment advice; I’m sharing my independent read as always.

Headline Numbers from the Print

Hims & Hers reported Q1 FY2026 revenue of $608.1M. That marked +3.8% YoY growth but a -1.6% QoQ dip. GAAP EPS came in at -$0.40, hit by $33M in one-time restructuring charges.

Gross margin compressed to 65.0%, down from 73% in the prior-year quarter. Subscribers grew to 2.584M, up 9.0% YoY. Monthly ARPU slipped to $80, a 6.0% YoY decline.

Free cash flow stayed positive at $53.0M. The revenue print narrowly missed the pre-print EODHD consensus of $616.9M; EPS also fell short, largely from those charges.

How My Pre-Earnings Call Stacked Up

My pre-earnings model had Q1 FY2026 revenue at $614.9M. The company reported $608.1M, a gap of $6.8M or 1.12% MAPE; I overshot slightly.

Consensus from EODHD sat at $616.9M pre-print; their error was $8.8M or 1.44% MAPE. My estimate edged out the Street this time, but single-quarter accuracy is noisy; the real test is consistency over multiple prints.

Web traffic grew 15.5% QoQ to 23.7M visits. That signal captured the demand strength well.

FDA restrictions on compounded semaglutide were a key risk; those drove the $33M charges and the 8% YoY U.S. revenue decline. The Hers brand traffic surge provided the expected offset; this drove the 969% YoY international growth.

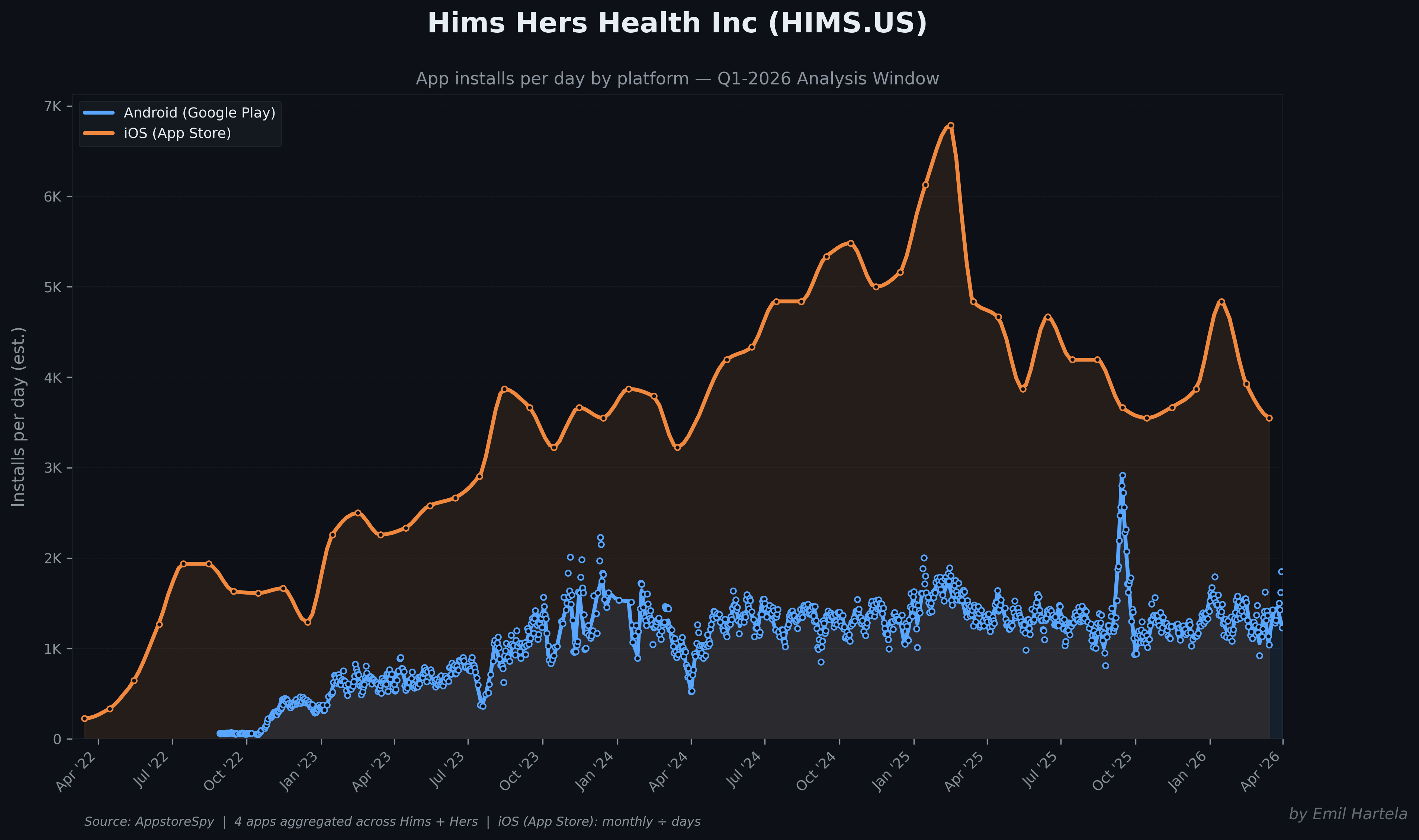

App installs softened in February-March, hinting at the 6% YoY ARPU drop to $80, but my model didn’t fully bake in the mix shift’s depth. The international offset proved stronger than I anticipated, contributing to my slight overshoot.

Management’s Take on the Drivers

Management pinned the quarter’s drag on the pivot from compounded GLP-1 drugs to branded options like Novo Nordisk’s Wegovy. That shift triggered $33M in one-time restructuring charges, including $28M in write-downs on obsolete ingredients.

Subscribers climbed 9% YoY to 2.584M, showing healthy demand. ARPU fell 6% YoY to $80 as the mix moved away from high-margin compounded GLP-1 toward lower-priced branded and other offerings.

Geographic shifts stood out: international revenue exploded 969% YoY, while U.S. revenue dropped 8% YoY where the GLP-1 pause hit hardest. Free cash flow held at $53M despite the costs; adjusted EBITDA halved to $44.3M from $91.1M a year ago.

The lab testing rollout continues, with scaling planned through 2026 and 2027.

Breaking Down the Segments

United States

U.S. revenue landed at $529.9M, down 8.0% YoY. This segment, 87.1% of total, bore the brunt of the compounded GLP-1 pause. Traffic data showed flat Hims brand visits; the decline tied to regulatory restrictions on semaglutide.

The strategic shift to branded GLP-1 hit ARPU here hardest. App installs softened late in the quarter, signaling the product transition’s drag.

Rest of World

Rest of World revenue hit $78.2M, up 969.0% YoY. At 12.9% of total, this surge offset U.S. weakness as international scaling ramps.

Hers brand traffic jumped from 8.8M to 11.6M visits; this drives the growth story. The mix shift shows expansion potential beyond domestic headwinds.

Forward Guidance and Implications

Management guided Q2 revenue to $680M–$700M, above pre-print consensus. For full-year FY2026, they raised the range to $2.80B–$3.00B from the prior $2.70B–$2.90B; second-half acceleration is coming.

They expect a return to profitability in 2027 as GLP-1 transition costs fade. The lab testing platform rolls out with commercial scaling targeted through 2026 and 2027.

International scaling is working; the raised guide shows confidence in monetization ramps. U.S. stabilization will be key to watch amid the pivot.

Stock Move and Market Chatter

Shares dropped roughly 13.0% in after-hours trading from the $29.14 regular-session close on 2026-05-11, with prices ranging from $25.08 to $25.55.

Chatter on X split evenly. Bulls pointed to the raised full-year guidance to $2.8-3.0B, 969% YoY international revenue growth, and subscriber additions to 2.584M as thesis positives. They highlighted the Novo Nordisk partnership; not a pilot; and $53M free cash flow as signs of long-term health.

Bears focused on the revenue miss, -$0.40 EPS, 8% YoY U.S. revenue decline, and gross margin drop from 73% to 65%. They flagged adjusted EBITDA halving to $44.3M and ARPU sliding 6% as structural risks from the GLP-1 pivot.

The debate centers on execution in shifting to branded GLP-1, sustaining international momentum, and reversing U.S. trends into Q2.

Reflections on This Print

This print surprised me with the international offset’s strength; 969% YoY growth masked more U.S. pain than I modeled. Flagging FDA risks paid off, capturing the $33M charges, but I underestimated their ARPU impact.

My model edged consensus with 1.12% MAPE versus 1.44%, thanks to traffic signals nailing subscriber growth. The miss came from not weighting international data heavier amid the pivot.

Going forward, I’ll recalibrate ARPU for mix shifts and bake in one-time charges explicitly for regulatory transitions. The key watch item is U.S. revenue stabilization above $529.9M in Q2 as branded GLP-1 ramps.

Prediction vs Actual Breakdown

My pre-earnings estimate was $614.9M; the company reported $608.1M, a gap of $6.8M or 1.12% MAPE. Consensus was off by $8.8M or 1.44% MAPE. This quarter my model edged out the Street, but one print is just a data point—plenty to tune going forward.

Key Metric into Q2

Watching U.S. revenue for signs of stabilization above $529.9M in Q2, as the GLP-1 branded pivot ramps and aims to reverse the 8% YoY decline from Q1.

A speculative note from the author

So here is what I think of the company as an investment.

I think bears don’t understand that there is genuinely a lot of growth ahead of the firm. My web traffic data for Q2 so far already points to a print at the high end of guidance, and I think it’s possible they even exceed it; potentially around 720 mil in Q2. Long term, I think the company will boast a meaningfully bigger revenue base than today.

But here is what I think the bulls get wrong.

The business model doesn’t support massive margins. You have substantial sales and marketing costs, ongoing SBC, and persistent R&D spend. That realistically means you have to accept an owner yield somewhere around 10% at steady state. Modeling anything higher is reckless. The output of this is that Hims is still slightly expensive even post the Q1 earnings dip.

So here is how I am looking at the stock. Wait and see if it goes even lower, say into the 10 to 20 USD range, and then potentially prepare to buy options ahead of a strong future print like Q2 is likely to be. But at today’s prices the stock doesn’t really make much sense compared to other names in the opportunity set.

Disclaimer: This research is informational and not personalized investment advice. Outputs blend alternative data with a disciplined internal workflow; figures are directional and may change as new information arrives. Past accuracy does not guarantee future results.

If you want more of these before they hit earnings, subscribe