Haypp's M&I might be the entire story

The hiring tells you what the financials don't

I’ve recently been digging into Haypp’s M&I business based on their LinkedIn hiring, and I think I might have been slightly undervaluing the company. Let me explain.

Most investors look at Haypp and see a low-margin online nicotine retailer trading at 0,7x sales, growing top-line at ~25% CAGR, with a thin EBIT margin. The bull case is that it’s cheap on a sales basis and the US market is opening up. That framing is fine, but it’s incomplete in a way I hadn’t fully appreciated until I went through their open job postings and cross-referenced them against what management has been saying.

The short version: Haypp isn’t building a better ecommerce business. They’re building a retail media network. The hiring pattern, the technology choices, and the language in the job descriptions all point to a deliberate, multi-year transformation of M&I from a high-margin data subscription bolt-on into something structurally closer to Amazon Ads at small scale. If they pull it off, the unit economics of the entire group change, and the right way to value Haypp shifts from “ecommerce multiple on consolidated revenue” to a sum-of-parts where the M&I piece carries a software/ad-tech multiple.

This isn’t a thesis I can prove from current financials. M&I is still reported as roughly 10% of revenue inside the consolidated number, and management hasn’t broken out its margin profile separately. But the operational evidence is unusually clear, and the trajectory is the kind of thing that gets ignored until segment-level disclosure forces the market to acknowledge it.

Below, I’ll lay out what I found, what M&I actually is today, what they appear to be building, and why I think the right way to think about Haypp is no longer just as a nicotine retailer.

NFA. This is my own analysis for entertainment purposes; do your own research before making any investment decisions.

The backstory

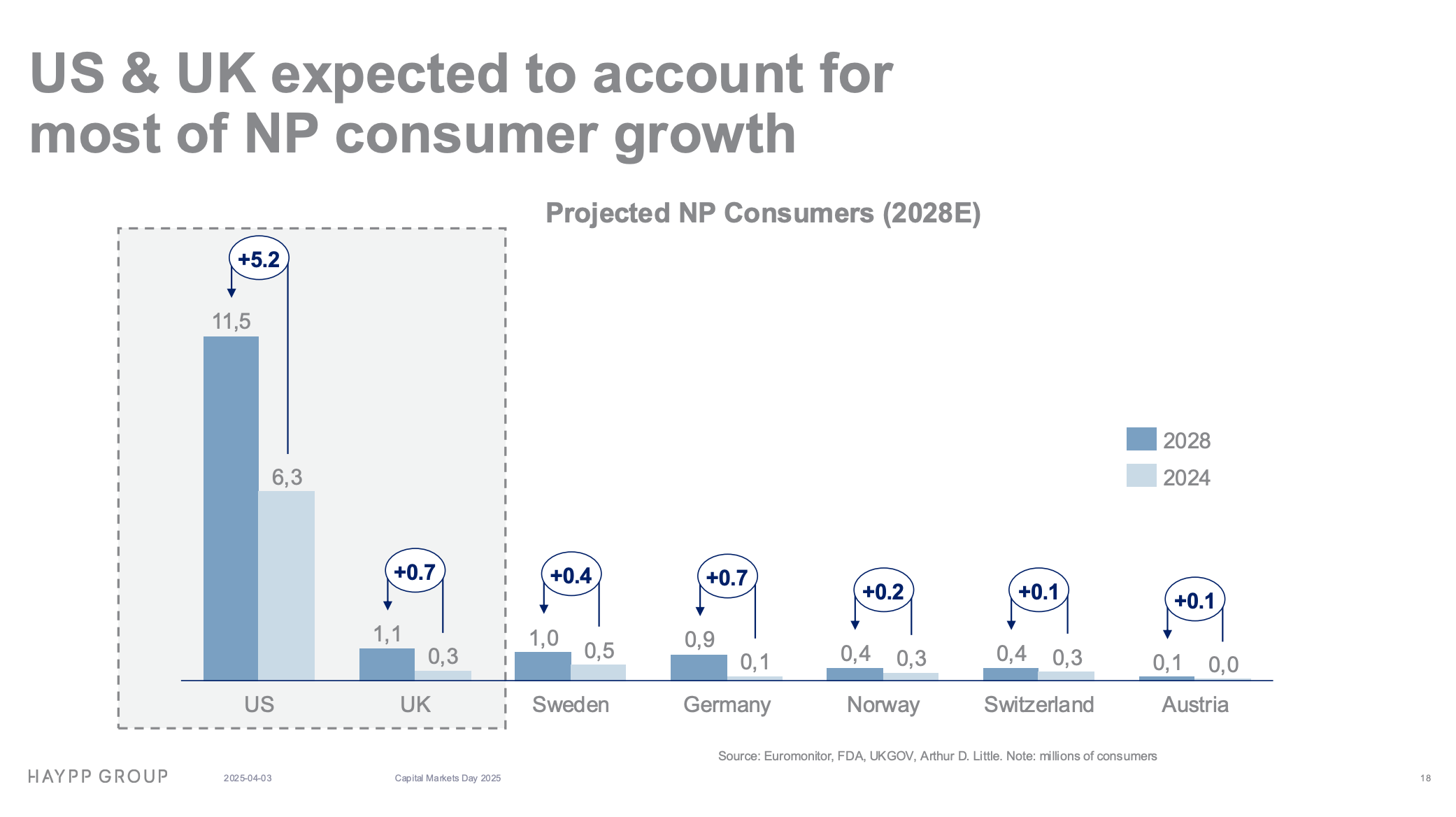

Haypp Group runs 16 e-commerce sites across 7 countries, selling nicotine pouches and snus. Total revenue is around SEK 4 billion, growing at an 18-25% CAGR target through 2028, with about 1,1 million active consumers.

But Haypp doesn’t just sell pouches. They also run a business unit called Media & Insights (M&I), which currently accounts for around 10% of revenue and grows at roughly 2x the rate of the rest of the group. M&I is the part of Haypp that has driven most of the gross margin expansion over the past two years; the consolidated gross margin has gone from 14,3% in Q2 2024 to 19,2% in Q2 2025, and management has explicitly attributed a meaningful share of that uplift to M&I.

So what is M&I actually doing today? It splits into two pieces.

The Insights piece. Haypp sits on a dataset that effectively does not exist anywhere else: every transaction by ~1,1 million age-verified online nicotine consumers across 16 sites in 7 countries. They know exactly which products switch to which, how price elasticity varies by market, which flavors are gaining share in real time, what percentage of ZYN buyers also try VELO, repeat rates by SKU, basket composition, and conversion rates by brand. There is no Nielsen for online nicotine. The offline scanner data captured by IRI/Circana, the kind shown in the WhiteWillowResearch tweet I recently saw, only covers physical retail. Haypp packages this data into reports and dashboards and sells it on contract to the six big brand owners (PMI, BAT, Altria, JTI, Imperial, and Swedish Match before PMI absorbed it), to regulators, and to researchers. This is essentially a syndicated data product, structurally similar to what NielsenIQ sells to FMCG companies. The revenue model is recurring contracts; the cost structure is mostly the analytics team that produces the data plus a small commercial team. Once the pipeline is built, each new contract is almost pure margin.

The Media piece. Brand owners pay Haypp for premium placement on Haypp’s owned properties: featured product slots on category pages, sponsored placements on the homepage, dedicated landing pages for new flavor launches, email campaigns to existing customer cohorts, and supplier-funded promotional pricing on key SKUs. This is closer to traditional retailer co-op marketing or trade marketing dollars. It’s high-margin because Haypp owns the inventory and doesn’t pay anyone to acquire the audience (97% of traffic is organic, marketing costs run below 1% of revenue). But the deals are manually negotiated, not programmatic. They aren’t measured with ad-tech-grade attribution. They aren’t bought through a self-service interface. Each campaign is essentially a custom project.

So today’s M&I is a data subscription business plus a manually-sold on-site media business. Both pieces are attractive on their own, both are growing, and together they explain why the consolidated gross margin keeps expanding. Nothing about this is hidden; management talks about M&I on every earnings call, and the Capital Markets Day 2025 deck makes the 10% revenue / 2x growth disclosure explicit. This is the visible part.

The interesting part is what they appear to be building next, and that’s where the LinkedIn search comes in.

What the LinkedIn search revealed

Haypp’s public job board (which mirrors what they post on LinkedIn) currently shows around 11 open roles. What stood out is that several of them describe a retail media platform under active construction, using technical vocabulary that doesn’t show up in earnings reports. Three roles in particular tell the story.

Retail Media Lead (Stockholm). This is the central role. The JD asks for someone with 8+ years of experience in “Retail Media, AdTech, or E-commerce strategy” with a “strong understanding of ad servers, SSP/DSPs, and first-party data activation”. The mission, in their words, is to “scale our current offering into a world-class advertising network” across all 16 platforms. Responsibilities include partnering with Tech and Product teams to “implement new ad formats (on-site, off-site, and social) and improve self-service capabilities”, and working with the Data team to “refine audience segmentation and attribution modelling”. This is not a marketing role. It is a product and platform role that uses the technical vocabulary of programmatic advertising.

Global Paid Co-Marketing Lead (Stockholm). The mission here is to design “the global paid co-marketing roadmap” that balances Haypp’s brand identity with “supplier-specific visibility across paid marketing channels”. Translated: take supplier media budget and deploy it through paid channels off Haypp’s own properties, with Haypp orchestrating the spend. This is the operational equivalent of an off-site DSP function, the same capability Amazon DSP provides for brands advertising off Amazon.

Retail Media Ad Ops Specialist (Stockholm). This role is explicitly being hired to “build and own our ad operations function from the ground up”. An ad ops function is the operational backbone of an ad platform; the people who manage campaign trafficking, creative QA, performance reporting, and the day-to-day running of advertiser accounts. The phrase “from the ground up” is the most important one in the entire job board: it tells you the operational layer of the platform doesn’t fully exist yet.

Underneath these three, there’s a supporting cluster of data and engineering hires (Internal Analytics Manager, Senior Data Analyst, Data Engineer, Head of Engineering) that build the data infrastructure any ad platform depends on. Individually unremarkable; collectively they’re the technical foundation the retail media stack sits on top of.

A few things make this set of roles particularly revealing.

First, the technical vocabulary. SSP/DSP, ad server, first-party data activation, attribution modelling, audience segmentation, self-service capabilities; this is the language of Amazon Ads, Walmart Connect, and Criteo. It is not the language of a retailer’s marketing department. Combined with the fact that Haypp has already deployed Kevel (the leading white-label ad server for retailers building their own ad networks), this is the technology stack of a retail media platform under active construction.

Second, the org shape. Hiring a global lead, an off-site orchestration role, and an ops specialist simultaneously is exactly the shape of an ad platform org chart in its first year of build-out. Hiring just one of these would suggest scaling existing capability. Hiring all three at once suggests building something new and treating it as a strategic priority.

Put together, the LinkedIn evidence describes a company in the late-foundation, early-productization stage of building a retail media network. The data infrastructure is in place. The ad server is deployed. The org around it is being hired. The self-service interface and the off-site DSP capability appear to be the next 12-24 months of work. None of this is mentioned explicitly in earnings reports beyond the high-level “Media & Insights is growing 2x” disclosure, but the operational footprint is unambiguous.

That gap between the operational footprint and what the financial reporting currently shows is the interesting investment angle, and it’s where I’ll go next.

The opportunity

To understand why this matters, you have to understand the unusual position the big nicotine brand owners are in. PMI generates around $37 billion in revenue annually, BAT around £27 billion, Altria around $20 billion. Companies of that size would normally spend somewhere between 6% and 10% of revenue on marketing. PMI alone is therefore working with a global marketing budget likely in the range of $2-4 billion. The combined nicotine industry’s marketing budget across these six brand owners runs into the tens of billions of dollars annually.

The problem is they have almost nowhere to spend it.

TV is heavily restricted or outright banned in most markets through the US Master Settlement Agreement and equivalent rules in Europe. Print is dying and most major publications won’t accept nicotine advertising even where it’s legal. Out-of-home is being progressively banned in city after city. Meta prohibits all nicotine product advertising, full stop. Google heavily restricts nicotine ads on Search and YouTube. TikTok prohibits it. Influencer marketing is blocked by both platform policies and PMI’s own internal rules, which prohibit using social media influencers in the US or anyone under 35 in marketing materials. The giant platforms where every other consumer goods company spends the bulk of their digital budget are categorically closed to nicotine.

So where does the money actually go today? A fragmented mess of channels: owned media on age-gated brand sites, a small handful of endemic publishers, retail co-op deals with c-store chains for shelf placement, sponsorships of motorsports and adult-oriented events, and a meaningful amount of underspent budget that sits idle because there’s nowhere efficient to put it. None of this offers the targeting, attribution, or scale that PMI’s media team would get on Meta if Meta took their money.

Haypp currently captures only a tiny slice of this budget. M&I is around SEK 400 million in revenue, split across the six brand owners, mostly through manually-negotiated insights contracts and on-site placements. Against a combined nicotine marketing budget that runs into the tens of billions, Haypp is capturing on the order of 1-2% of the industry’s available digital marketing dollars, despite running the only large-scale, age-verified, attributable digital nicotine consumer audience in the world. The constraint isn’t supplier willingness to spend; the constraint is that Haypp’s current model can only handle so many bespoke deals at once.

This is where self-service changes the shape of the business. The reference example most investors will know is Reddit. For years Reddit had a perfectly functional ad business that was bottlenecked by manually-negotiated direct deals with big brands. The economics were fine but the growth was slow because every dollar of revenue required a salesperson. When Reddit invested seriously in self-service infrastructure (specifically the auction-based Ads Manager that lets any advertiser set up a campaign without ever speaking to a Reddit employee), advertiser counts went from a few thousand managed accounts to hundreds of thousands of self-serve accounts, and ad revenue scaled in a way that wasn’t possible under the old model. The same dynamic played out at Meta in the early 2010s, at Pinterest after their 2018 self-serve launch, and at every retail media network that has matured. Self-service doesn’t just make existing advertisers more efficient; it brings in advertisers and campaign types that the manual sales motion couldn’t economically support. The long tail of smaller suppliers, regional variants, and challenger brands like Lucy, Rogue, On!, and Black Buffalo can buy their way in once the minimum spend drops from “negotiate a six-figure quarterly deal” to “log in and run a 5,000 SEK test campaign next week.”

The honest caveat is that it’s not entirely clear from the outside how much self-service Haypp has already built. The Retail Media Lead JD talks about “improving self-service capabilities”, which suggests some baseline exists, but the Ad Ops Specialist being hired “from the ground up” suggests the operational layer underneath is incomplete. The Kevel deployment provides the ad-serving infrastructure but Kevel is a toolkit, not a turnkey product; building a true self-service buyer interface on top of Kevel is itself a multi-quarter engineering project. My best read is that Haypp is somewhere in the middle of this transition, with parts of the stack functioning and parts still being built. The exact state isn’t visible from public disclosure.

What you can say with confidence is that the direction is unambiguous. They are building the architecture that converts a manually-sold, sales-capacity-constrained media business into an auction-based, software-scaled platform that big brand owners can deploy meaningful budget into without Haypp adding headcount proportionally. In a category where those brand owners have tens of billions of marketing dollars and almost nowhere compliant to spend them, the difference between capturing 1-2% of that budget and capturing 5-10% of it is the difference between Haypp being a small Nordic ecommerce retailer and Haypp being something materially different.

The valuation case

Here’s where the thinking gets interesting.