Haypp Group Revenue Prediction Q2 2026

Is Haypp's strategy changing? Web traffic doing weird things

Welcome to my Q2 Haypp Group revenue prediction based on web traffic. In this series I nowcast Haypp Group’s revenue and share intel before earnings in order to front run potential moves.

In this quarter’s edition we have some mind boggling data to deal with. Saying that Haypp Group web traffic was strong in Q2 would be an understatement; their traffic seems to have disconnected from its past growth trajectory. I will begin by showing you the data. After that I will dissect the big elephant in the room, and finally I will share my take on how Q2 earnings will go down.

NFA. Nothing here is investment advice.

Backdrop

Before diving into the numbers it is worth setting the scene, since Q2 was an unusually busy quarter on the regulatory front. Most of what matters for Haypp happened around the edges of policy, so I will keep this part focused.

The first item is the French ban. France’s decree banning nicotine pouches took effect on 1 April 2026, right at the start of the quarter. The ban is the most comprehensive in Europe; it covers manufacture, sale, import, possession and use of all non medicinal oral nicotine products. France thus became the first European country to criminalise possession and use, going further than Belgium, the Netherlands or Germany. A partial legal challenge suspended the manufacturing and export provisions, but the import, possession and use ban all took effect as scheduled.

The second and more important item is the FDA enforcement guidance. On 8 May 2026 the FDA issued guidance titled “Enforcement Priorities for Certain New Tobacco Products Marketed Without Premarket Authorization.” In plain terms, the agency clarified that it does not intend to prioritise enforcement against nicotine pouch products whose manufacturers have a pending and accepted PMTA. Crucially, the FDA also said it will create and maintain a public list identifying which products fall under this policy. This is a big deal for the industry. For four years pouch manufacturers, suppliers and retailers had been stuck in a grey zone of uncertainty; Haypp’s own VP of regulatory affairs described the guidance as remarkably clear, essentially file a compliant PMTA, wait 180 days, get acceptance and then launch. Companies can now push new products with far less fear of being wiped off shelves. It is worth noting the products remain technically unauthorised until the FDA actually grants marketing authorisation, and some state attorneys general have pushed back; but the direction of travel is a more orderly, regulated market, which benefits a compliant retailer like Haypp.

The third item is the most recent, landing just a few days ago. On 30 June 2026 the FDA issued modified risk tobacco product orders for 20 Zyn products, allowing PMI/Swedish Match to market them with the claim that using Zyn instead of cigarettes lowers the risk of mouth cancer, heart disease, lung cancer, stroke, emphysema and chronic bronchitis. These are the first MRTP orders ever granted for nicotine pouches. The implication for Haypp is bullish; the entire category now has an official regulatory stamp saying pouches are less harmful than smoking. That is exactly the kind of legitimacy that pulls smokers into the category, expands the total addressable market, and makes online retailers of authorised products more valuable. It also strengthens the harm reduction narrative that Haypp leans on when arguing against bans like France’s.

The fourth item is on the hiring side. Q2 looks to have been a very active recruitment season for Haypp; their careers page has had a notable number of open positions through the quarter. This lines up with management’s stated plan to invest in growth, and it strongly suggests headcount is growing, which matters for the margin discussion later.

The final item is on the EU side. The bloc’s long awaited revision of the Tobacco Products Directive (TPD3), which would for the first time bring nicotine pouches formally into EU wide scope, has once again slipped. The Commission published its evaluation of the current directive on 2 April 2026, concluding that novel nicotine products including pouches are insufficiently covered, which is the trigger for a revision. But the actual legislative proposal, expected at various points to arrive in mid 2026, has effectively stalled in the evaluation and impact assessment phase due to sharp disagreements between member states. The proposal is now not expected to land in draft form until late 2026 at the earliest, with rules unlikely to take effect before roughly 2028. The implication is neutral to mildly positive for Haypp in the near term; the regulatory overhang that could eventually impose flavour restrictions or tighter standards across the EU keeps getting pushed further out, buying the category more time to grow under the current fragmented national patchwork.

Web Traffic Breakdown · June 2026

Web traffic is the cleanest leading indicator we have for Haypp Group; a pure-online B2C retailer where every paying customer has to land on one of these domains, and where revenue is single-transaction, so visit volume maps almost mechanically to orders × AOV. In an in-house audit of the last 9 reported quarters, panel visits explained group revenue at Pearson r ≈ 0.94 on a YoY% basis.

Each domain card below leads with the June total, then the month-on-month move vs May, the gap to the Q1 2026 monthly baseline, and YoY.

Core, Mature Nordic

Looking at Haypp's core markets we see strength in the smaller sites, while the biggest core site, snusbolaget.se, is slightly down for the quarter at -6,5%. This was largely expected already at the end of last quarter, as net sales grew more strongly than active customers, a leading indicator for core. The equal weighted average across the Core cohort came in at +8,9% versus the prior quarter baseline, with snushjem.no the standout at +28,2%. See charts below.

snushjem.no — Norway

June 2026: 65K visits — +28.2% growth vs the Q1 2026 monthly average (51K). Month-on-month it’s up 15.0% on May’s 57K. On a YoY basis the site is +112.9%. This is the strongest grower across the segment so far this month.

snuslageret.no — Norway

June 2026: 152K visits — +13.5% growth vs the Q1 2026 monthly average (134K). Month-on-month it’s up 1.7% on May’s 149K. On a YoY basis the site is +32.2%. One of the strongest growers in the segment this month.

snus.com — Norway

June 2026: 45K visits — +6.6% growth vs the Q1 2026 monthly average (43K). Month-on-month it’s down 8.8% on May’s 50K. On a YoY basis the site is +21.0%. Growing in line with the segment composite.

nettotobak.com — Sweden

June 2026: 140K visits — +2.9% growth vs the Q1 2026 monthly average (136K). Month-on-month it’s down 11.4% on May’s 158K. On a YoY basis the site is +42.6%. Growing in line with the segment composite.

snusbolaget.se — Sweden

June 2026: 484K visits — -6.5% decline vs the Q1 2026 monthly average (517K). Month-on-month it’s down 1.6% on May’s 491K. On a YoY basis the site is +32.9%. The weakest performer in the segment, dragging the composite.

Growth — UK · US · DE · CH (Vape + HNB)

For the growth segment we are seeing something completely unprecedented. In the history of Haypp there hasn't been this aggressive a web traffic inflow to their sites; more on that later. The equal weighted average across the Growth cohort came in at +61,0% versus the prior quarter baseline, driven by haypp.com at a staggering +158,0%. Not everything rose though; snusmarkt.ch was the weakest at -13,5%. See chart below.

haypp.com, (multi-market flagship)

June 2026: 832K visits — +158.0% growth vs the Q1 2026 monthly average (322K). Month-on-month it’s up 32.4% on May’s 629K. On a YoY basis the site is +196.9%. This is the strongest grower across the segment so far this month.

northerner.com — United States

June 2026: 998K visits — +130.2% growth vs the Q1 2026 monthly average (434K). Month-on-month it’s up 33.5% on May’s 748K. On a YoY basis the site is +261.6%. One of the strongest growers in the segment this month.

vapeglobe.de — Germany

June 2026: 31K visits — +25.3% growth vs the Q1 2026 monthly average (25K). Month-on-month it’s down 20.6% on May’s 39K. On a YoY basis the site is +225.8%. Growing in line with the segment composite.

nicokick.com — United States

June 2026: 449K visits — +5.3% growth vs the Q1 2026 monthly average (427K). Month-on-month it’s down 3.9% on May’s 467K. On a YoY basis the site is +0.8%. Growing in line with the segment composite.

snusmarkt.ch — Switzerland

June 2026: 15K visits — -13.5% decline vs the Q1 2026 monthly average (17K). Month-on-month it’s up 12.5% on May’s 13K. On a YoY basis the site is +23.2%. The weakest performer in the segment, dragging the composite.

Note

Although the Haypp and Northerner charts look like they are going parabolic, they seem to be coming down sharply in the last week of June.

The Elephant in the Room

If you have read multiple Haypp Group web traffic reports by now you will immediately see that something is up with Northerner and Haypp.com. Never in the history of all of Haypp web traffic has there been such a violent move. Not only are the two sites completely synced; they both started rising at the same time and peaked at the same time. Even further, the size of the moves are very close. This does not feel organic. So the question is: why have two of Haypp’s biggest sites all of a sudden seen 200% surges in traffic in Q2.

First I will present some of the evidence so that you can get a look into some of the logic behind my prediction and what I tinker around.

The first piece of the evidence can be found in SimilarWeb. Looking at SimilarWeb data and where that traffic is coming from, you notice that Germany is dominating that traffic. Essentially in one quarter the amount of Germans visiting Haypp’s websites has increased over 400%.

The second piece of evidence can also be found in SimilarWeb. A big chunk of the new traffic seems to be coming from display ads, many of them targeted at adult sites.

Another piece of evidence, or perhaps more of a potential lead, is the fact that France’s ban of nicotine pouches went into effect at the start of the quarter.

Even further, many German gas stations and convenience stores have voluntarily stopped selling nicotine pouches.

Now piecing all this together, it seems like Haypp Group has decided to do a sort of blitz marketing campaign that particularly targets Germans. Essentially we likely have a mix of factors giving Haypp extraordinary growth here. First, the French ban likely has some small part of Frenchman ordering NP to Germany and then using it illegally in France. At the same time Germans also struggle to get NP as a lot of the logical places to buy it don’t sell it, pushing online penetration way up.

Haypp Group must have realized that now is their time to strike, and thus they started a strong ad campaign, likely the largest one they have ever done.

My data roughly shows that Haypp has gotten around 5 million extra visits to their site in Q2. Most of this can likely be attributed to them running ads. Now the cost of running these ads should be very low; we are talking CPC under 10 cents. So essentially the extra cost of their marketing push would likely be under 5 MSEK.

Now the bigger implication here is of course what do these new consumers order, if they order at all. It is almost always the case when there is a huge influx of customers that order value goes down per visit. The difficult part is knowing to what extent. We don’t have any data to estimate the elasticity of current events, but I will try to do my best to predict how well this spike translates into revenue in the next chapter.

Now before I end this section I want to say a word of warning. My interpretation of what is going on can be faulty. Web traffic can be manipulated and there are countless factors that could mislead in this type of situation. Germans all of a sudden ordering a bunch more nicotine pouches seems highly suspicious. It is possible that SimilarWeb’s panel data simply over counts Germany.

What the street thinks

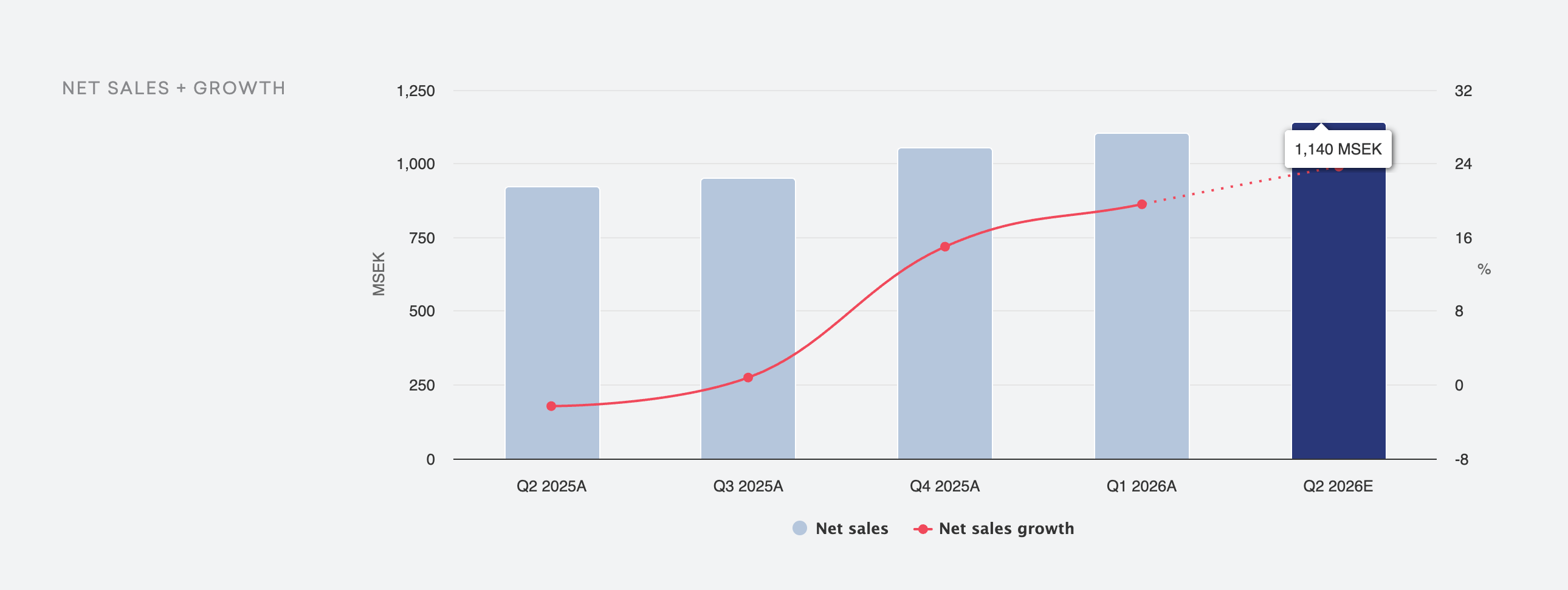

Before showing my own estimates, let’s take a look at what analysts and Twitter think. First the analyst consensus from Barclays, Deutsche Bank and Pareto Securities; they land at 1140 MSEK. Chart below. Here it is worth noting that the 1140 MSEK likely represents a time series estimate, that is roughly where revenue should land if they grow at the pace of management’s guidance.

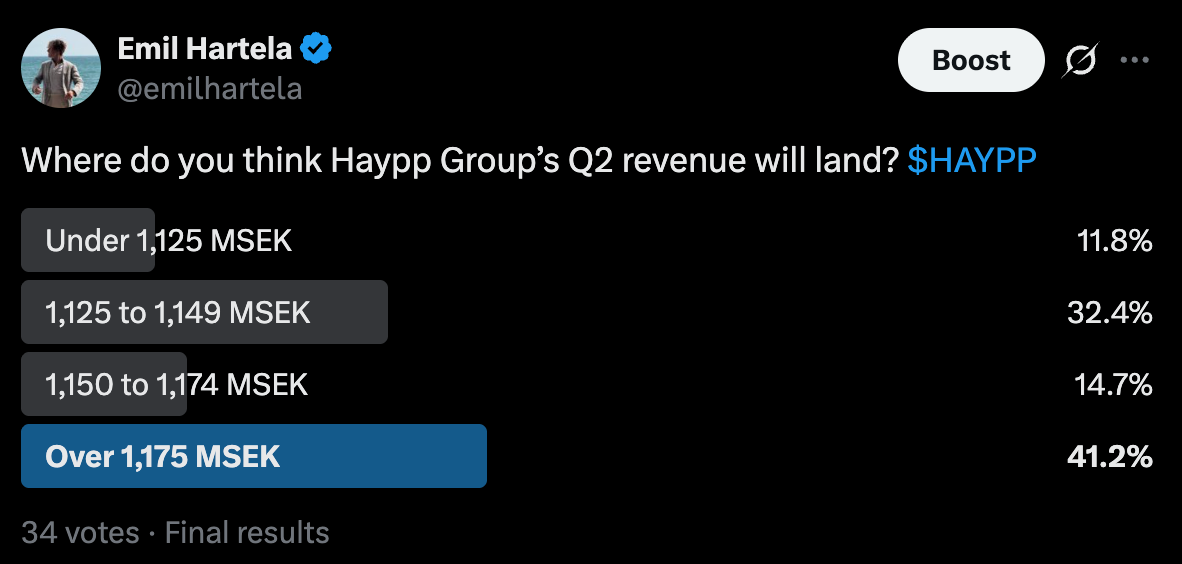

And here is the result of Twitter, from my one week poll that got 34 votes. The result can be seen below and averaged shows 1158 MSEK. On average the X crowd has been really good at estimating revenues, with the exception of last year's Q2. Thus 1158 MSEK provides another valuable data point, as last year's Q2 miss was likely caused by a bias to the upside, since very few expected Haypp shrinking.

In total, both X and analysts seem to think that revenue will have grown roughly 25% from last year; a very reasonable estimate. Next, let's dive into my estimate.